Corporate Tax Obligations for Companies in Japan

Key Takeaways

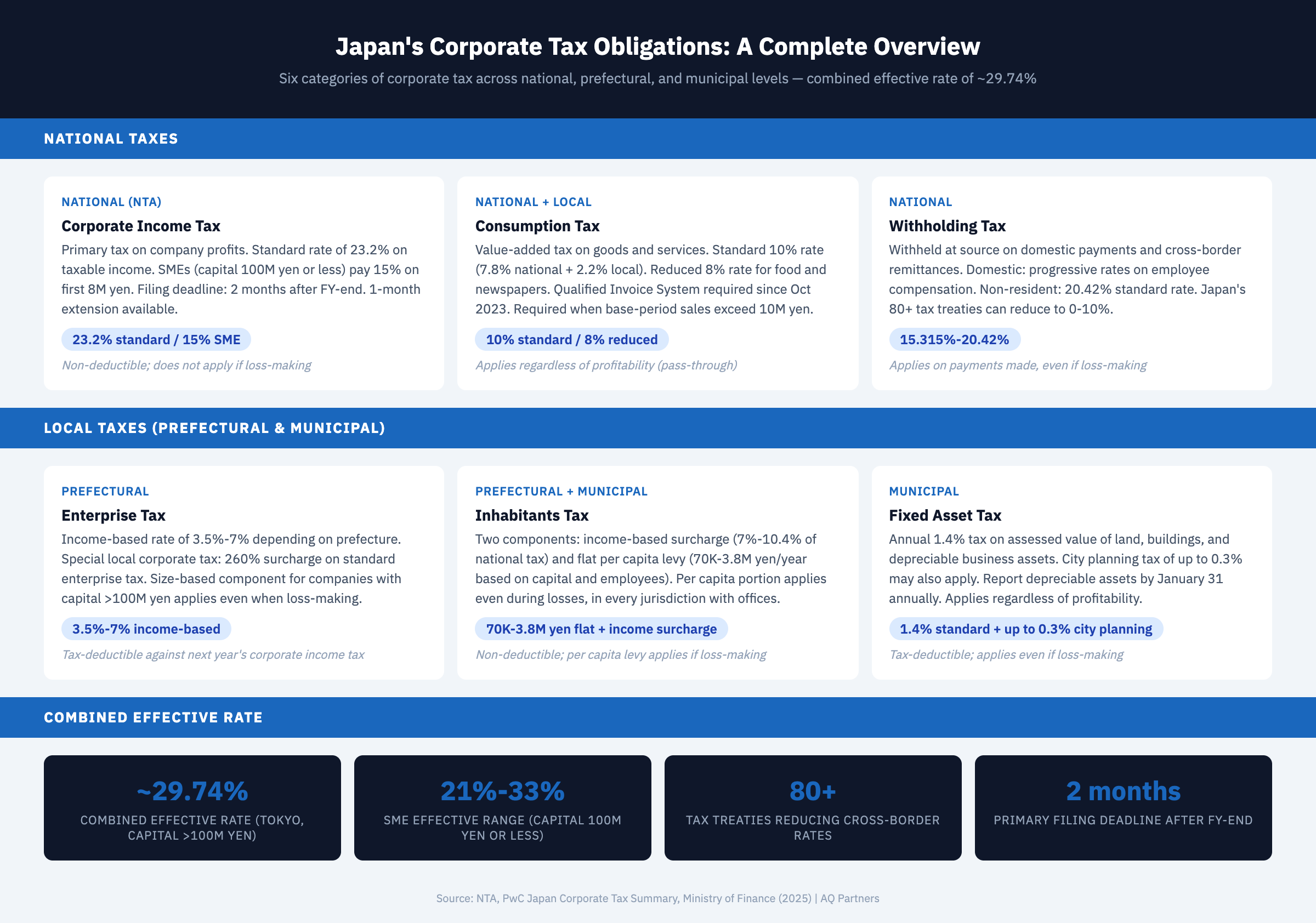

- Japan levies six main categories of corporate tax on business operations — corporate income tax (national), enterprise tax (prefectural), inhabitants tax (prefectural and municipal), consumption tax (national and local), withholding tax (on payments to nonresidents and employees), and fixed asset tax (municipal). Combined, these create an effective corporate tax rate of approximately 29.74% for companies with capital exceeding 100 million yen (PwC, 2025).

- Corporate income tax applies at 23.2% on taxable income above 8 million yen — SMEs with capital of 100 million yen or less benefit from a reduced 15% rate on the first 8 million yen of annual taxable income, per the National Tax Agency's published rate schedule.

- Enterprise tax and inhabitants tax are levied at the prefectural and municipal levels — enterprise tax is deductible from national taxable income in the following year, while inhabitants tax is not. These local taxes add roughly 7-10 percentage points to a company's total tax burden depending on location and capitalization.

- Consumption tax at 10% applies to most domestic transactions — companies with taxable sales exceeding 10 million yen in the base period must register, file, and remit consumption tax. The Qualified Invoice System (introduced October 2023) requires registered invoices for input tax credit claims.

- Foreign companies face additional obligations including withholding tax on cross-border payments — dividends, royalties, and service fees paid to nonresidents are subject to withholding rates of 15.315% to 20.42%, potentially reduced under Japan's network of over 80 tax treaties (Ministry of Finance, 2025).

What Corporate Tax Obligations Exist in Japan?

Corporate tax obligations in Japan encompass a multi-layered system of national, prefectural, and municipal taxes that collectively apply to companies conducting business within the country. Every company registered or operating in Japan — whether a Kabushiki Kaisha (KK), Goudou Kaisha (GK), or branch office of a foreign corporation — must comply with these obligations. Understanding the full scope of Japan's corporate tax framework is essential before establishing operations, because the system differs substantially from those in North America, Europe, and much of Asia.

Japan's corporate tax structure is not a single tax but a combination of distinct levies administered by different levels of government. The National Tax Agency (NTA) administers national corporate income tax and consumption tax, while prefectural and municipal governments assess enterprise tax, inhabitants tax, and fixed asset tax. For a foreign company entering Japan, the practical effect is that tax compliance involves filings with multiple authorities, each with its own forms, deadlines, and calculation methods. This guide provides the orientation-level overview a CFO needs before diving into the specifics of each tax type.

National Corporate Income Tax

National corporate income tax is the primary tax on company profits in Japan, assessed at rates of 15% or 23.2% depending on company size and taxable income level.

Japan's national corporate income tax applies to worldwide income for domestic corporations (those with a head office in Japan) and to Japan-source income for foreign corporations operating through a permanent establishment. The standard rate stands at 23.2% on taxable income. However, SMEs — defined as companies with stated capital of 100 million yen or less — benefit from a reduced rate of 15% on the first 8 million yen of annual taxable income, with the standard 23.2% rate applying to any amount above that threshold.

Taxable income is calculated by starting with accounting profit under Japanese GAAP and then applying tax adjustments prescribed by the Corporation Tax Act. Common adjustments include limits on entertainment expenses, prescribed depreciation methods and useful life periods, and restrictions on the deductibility of certain provisions. Companies that file under Blue Form tax return status gain access to valuable benefits including net operating loss carryforwards for up to 10 years.

The filing deadline for national corporate income tax is two months after the close of the fiscal year. Companies with a March 31 fiscal year end, which is the most common in Japan, must file by May 31. Extensions of one month are available upon application. Corporations must also make interim (provisional) tax payments six months into the fiscal year, based on either the prior year's liability or actual results for the first six months.

Prefectural and Municipal Enterprise Tax

Enterprise tax is a deductible local tax levied by prefectures on corporate income, with rates varying by company size, capital level, and business type.

Enterprise tax is assessed by the prefecture where a company maintains a place of business. Unlike most other taxes, enterprise tax paid is deductible as an expense when calculating national corporate income tax in the following fiscal year, making it effectively less costly than its headline rate suggests. According to PwC's Japan corporate tax summary, the standard enterprise tax rate on income is approximately 3.5% to 7%, depending on the prefecture and income bracket.

For companies with capital exceeding 100 million yen, Japan applies a size-based enterprise tax (gaikei hyojun kazei) in addition to the income-based component. This size-based portion consists of a value-added component and a capital component, calculated on metrics including total employee compensation, net interest payments, net rent payments, and the company's stated capital. The size-based enterprise tax applies regardless of whether the company earns a profit, creating a minimum tax obligation for larger entities.

A special local corporate tax (tokubetsu hojin jigyozei) is assessed as a surcharge on the income-based enterprise tax at a rate of 260% of the standard enterprise tax amount. Despite its name, this tax is collected by the national government and redistributed to local governments. For a detailed breakdown of enterprise tax calculation, see our guide to local enterprise tax and inhabitants tax.

Inhabitants Tax (Prefectural and Municipal)

Inhabitants tax is a non-deductible local tax combining an income-based surcharge and a flat per capita levy, assessed by both the prefecture and the municipality where a company operates.

Corporate inhabitants tax (juminzei) has two components. The income-based component is calculated as a percentage of the company's national corporate income tax liability — effectively a surcharge on the national tax. Prefectural inhabitants tax ranges from 1% to 2% of the national tax, while municipal inhabitants tax ranges from 6% to 8.4%, depending on the municipality. Combined, the income-based inhabitants tax surcharge adds approximately 7% to 10.4% of the national corporate income tax amount.

The per capita component (kintowari) is a flat annual levy that applies regardless of profitability. The amount depends on the company's stated capital and the number of employees in each jurisdiction. A company with capital of 10 million yen or less and 50 or fewer employees pays approximately 70,000 yen per year in combined prefectural and municipal per capita tax. Larger companies with capital exceeding 5 billion yen and more than 50 employees may pay up to 3.8 million yen annually per municipality. This means a loss-making company still owes per capita inhabitants tax in every jurisdiction where it has offices or employees.

| Tax Type | Level of Government | Rate / Range | Tax-Deductible? | Applies Even if Loss-Making? |

|---|---|---|---|---|

| National Corporate Income Tax | National (NTA) | 15% / 23.2% | No | No |

| Enterprise Tax (Income-Based) | Prefectural | 3.5%–7% | Yes | No |

| Enterprise Tax (Size-Based) | Prefectural | Varies by capital / payroll | Yes | Yes (capital > 100M yen) |

| Special Local Corporate Tax | National (redistributed) | 260% of standard enterprise tax | Yes | No |

| Inhabitants Tax (Income-Based) | Prefectural + Municipal | 7%–10.4% of national tax | No | No |

| Inhabitants Tax (Per Capita) | Prefectural + Municipal | 70,000–3,800,000 yen/year | No | Yes |

| Consumption Tax | National + Local | 10% (8% reduced rate) | N/A (indirect tax) | Yes (pass-through) |

| Withholding Tax (Nonresident) | National | 15.315%–20.42% | N/A (withheld at source) | Yes (on payments made) |

| Fixed Asset Tax | Municipal | 1.4% (standard rate) | Yes | Yes |

| City Planning Tax | Municipal | Up to 0.3% | Yes | Yes |

Consumption Tax

Consumption tax is Japan's value-added tax levied at 10% on most goods and services, with an 8% reduced rate for food and beverages — companies exceeding 10 million yen in base-period taxable sales must register and file.

Japan's consumption tax (shouhizei) functions similarly to a VAT system. Businesses charge consumption tax on their sales, collect it from customers, and remit the net amount (output tax minus input tax credits) to the tax authorities. The standard rate is 10%, comprising 7.8% national consumption tax and 2.2% local consumption tax. A reduced rate of 8% (6.24% national, 1.76% local) applies to food and non-alcoholic beverages as well as newspaper subscriptions.

A company becomes a taxable enterprise when its taxable sales in the base period (generally two fiscal years prior) exceed 10 million yen. Newly established companies with stated capital of 10 million yen or more are treated as taxable enterprises from inception, regardless of actual sales. Since October 2023, the Qualified Invoice System (tekikaku seikyusho) requires businesses to issue invoices that include the seller's registered invoice number, applicable tax rate, and tax amount in order for the buyer to claim input tax credits. Companies can learn more in our guide to the Qualified Invoice System and accounting software in Japan.

Filing frequency depends on consumption tax liability. Companies with annual liability exceeding 48 million yen file monthly, those with liability exceeding 4 million yen file quarterly, and all other taxable enterprises file annually. Consumption tax returns are due two months after the fiscal year end for corporations. According to JETRO's business setup guide, newly entering companies frequently underestimate the administrative burden of consumption tax compliance, particularly the record-keeping requirements of the Qualified Invoice System.

Withholding Tax on Cross-Border and Domestic Payments

Japanese companies must withhold tax at source on certain domestic payments and cross-border remittances — rates range from 10.21% on employee compensation to 20.42% on payments to nonresidents without a tax treaty.

Withholding tax (gensen choshuzei) in Japan applies in two primary contexts. For domestic payments, companies must withhold income tax on employee salaries, bonuses, director compensation, and certain professional service fees. Employment income withholding follows graduated tax tables published by the NTA and must be remitted to the tax office by the 10th of the following month.

For cross-border payments, Japan imposes withholding tax on dividends, interest, royalties, and certain service fees paid to nonresidents and foreign corporations. The domestic withholding rate is 20.42% (including the 2.1% reconstruction surtax) on most categories. However, Japan maintains an extensive network of over 80 tax treaties that can significantly reduce these rates. For example, the Japan-U.S. treaty reduces the withholding rate on dividends to 10% (or 0% for qualifying direct investments of 50% or more) and royalties to 0%. Our withholding tax guide provides a comprehensive breakdown of rates by payment type and treaty partner.

Companies making payments subject to withholding must file withholding tax returns and remit amounts withheld. Small companies with 10 or fewer employees can apply for semi-annual remittance (납부) rather than monthly, reducing administrative frequency. Failure to properly withhold and remit carries penalties including a 10% non-deduction penalty and interest on late payments.

Fixed Asset Tax and City Planning Tax

Fixed asset tax is a municipal tax of 1.4% assessed annually on the value of land, buildings, and depreciable business assets — it applies regardless of company profitability.

Fixed asset tax (kotei shisan zei) applies to three categories of property: land, buildings, and depreciable assets. The tax base is the assessed value of the property as of January 1 each year, determined by the municipality. For land and buildings, municipalities conduct periodic reassessments (typically every three years) using standardized valuation methods. For depreciable business assets, companies must file annual returns by January 31 declaring the acquisition cost and accumulated depreciation of assets in each municipality.

The standard rate is 1.4% of assessed value, though municipalities may set rates up to 2.1%. In designated urban planning zones, an additional city planning tax (toshi keikaku zei) of up to 0.3% may apply to land and buildings. According to PwC's summary of Japanese corporate taxes, the depreciable asset tax obligation catches many foreign companies off guard because it creates a tax liability independent of profitability. A company that owns office equipment, computers, and furniture worth more than 1.5 million yen in a single municipality will owe this tax even during periods of operating losses.

For companies leasing office space (which is common among foreign entrants), fixed asset tax on the building and land is borne by the property owner and typically reflected in rent. However, the company remains responsible for filing and paying depreciable asset tax on its own business equipment, furniture, and fixtures located in the leased premises.

Effective Tax Rate: Bringing It All Together

Japan's combined effective corporate tax rate stands at approximately 29.74% for standard companies — understanding how the components interact is essential for accurate financial planning.

| Component | Approximate Rate | Notes |

|---|---|---|

| National Corporate Income Tax | 23.2% | 15% on first 8M yen for SMEs (capital 100M yen or less) |

| Enterprise Tax (Income-Based + Special) | ~3.5%–7% | Deductible from next year's national tax base |

| Inhabitants Tax (Income-Based) | ~2.4% of taxable income | Surcharge on national tax; non-deductible |

| Inhabitants Tax (Per Capita) | 70,000–3,800,000 yen flat | Fixed amount regardless of profit |

| Size-Based Enterprise Tax | Varies | Capital > 100M yen only; payroll + capital components |

| Combined Effective Rate | ~29.74% | Standard rate for Tokyo; varies slightly by prefecture |

The effective tax rate calculation is not simply the sum of headline rates because of interactions between the taxes. Enterprise tax paid in one year reduces the national taxable income base in the following year. Inhabitants tax is calculated as a surcharge on the national tax, not on taxable income directly. These circular dependencies mean the effective rate must be computed iteratively. For a company operating in Tokyo with capital over 100 million yen, the widely cited combined effective rate of approximately 29.74% reflects these interactions (PwC, 2025).

For SMEs with capital of 100 million yen or less, the effective rate is lower due to the reduced national rate on the first 8 million yen and exemption from size-based enterprise tax. Depending on income levels and jurisdiction, SME effective rates can range from approximately 21% to 33%. For a comprehensive treatment of the national income tax component, see our corporate income tax rates and calculation guide.

What Foreign Companies Should Expect

Foreign companies establishing operations in Japan face the same tax obligations as domestic corporations, plus additional considerations around permanent establishment, treaty benefits, and transfer pricing documentation.

The first critical determination is whether a foreign company has created a permanent establishment (PE) in Japan. A branch office, a dependent agent concluding contracts on the company's behalf, or a construction project exceeding a specified duration can all trigger PE status. Once PE status exists, Japan taxes the income attributable to that PE, and all the tax obligations described in this guide apply in full.

Foreign companies should also prepare for several practical realities. Tax returns must be filed in Japanese, using prescribed NTA forms. The filing calendar follows the company's fiscal year, not the Japanese government's April-to-March cycle. Detailed tax calendar information for foreign companies is available in our dedicated guide. Record-keeping must conform to Japanese standards, with documents retained for a minimum of 7 years (10 years for Blue Form filers). And intercompany transactions with foreign related parties require contemporaneous transfer pricing documentation under Japan's transfer pricing rules.

The multi-layered nature of Japan's corporate tax system — spanning national, prefectural, and municipal authorities — means that compliance is an ongoing, year-round process rather than a once-a-year event. For a full roadmap of the compliance landscape, consult our Tax Filing in Japan: Corporate Compliance Guide.

Navigating Japan's corporate tax obligations requires careful planning and expert guidance. AQ Partners provides comprehensive tax coordination and compliance support for foreign companies operating in Japan — from initial setup through ongoing filings. Contact us to discuss your tax compliance needs.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.