Tax Depreciation in Japan: Asset Categories & Methods

Key Takeaways

- Japan prescribes mandatory depreciation methods and useful life periods for every asset category — companies cannot set their own estimates. The National Tax Agency's ordinance tables specify exact useful lives ranging from 3 years for market-sale software to 50 years for reinforced concrete buildings.

- Buildings must use straight-line depreciation (since 1998), and building facilities and structures since 2016 — the declining-balance method remains available only for machinery, vehicles, computers, and furniture. Corporations default to declining-balance unless they file a notification choosing straight-line.

- Declining-balance front-loads deductions at double the straight-line rate — a 5-year asset generates a 40% first-year deduction under declining-balance versus 20% under straight-line. Both methods produce the same total depreciation, but timing differs significantly for tax planning.

- SMEs with capital of ¥100 million or less can immediately expense assets under ¥300,000 — subject to Blue Form filing status and an annual cap of ¥3 million. All companies can expense items under ¥100,000 or elect 3-year lump-sum depreciation for items between ¥100,000 and ¥200,000.

- Book-tax depreciation differences must be reconciled on corporate tax returns — Japan requires parallel tracking of accounting and tax depreciation schedules. Depreciable asset tax of approximately 1.4% applies municipally on top of income tax depreciation impacts.

Understanding Depreciation Under Japanese Tax Law

Tax depreciation in Japan is the systematic allocation of an asset's acquisition cost across its government-prescribed useful life, governed by detailed National Tax Agency ordinances that specify exactly how companies must depreciate different asset types.

Unlike jurisdictions where businesses enjoy flexibility in setting their own useful life estimates, Japan mandates standardized periods based on asset categories. The fundamental principle is straightforward: companies can only deduct depreciation up to a calculated limit for each fiscal period. This limit derives from multiplying the asset's net book value by the applicable depreciation rate published by the NTA. If a company books higher depreciation for accounting purposes, the excess creates a book-tax difference that must be added back to taxable income.

One distinctive aspect of the Japanese system is its separation between accounting depreciation and tax depreciation. While Japanese GAAP and international standards like IFRS traditionally employ different approaches for financial reporting, tax law permits companies to choose between different methods depending on the asset category. According to PwC's Japan tax summary, this divergence means finance teams must track two separate depreciation schedules and reconcile differences when preparing corporate tax returns.

Asset Categories and Permitted Depreciation Methods

Japanese tax law divides depreciable assets into three primary categories — tangible, intangible, and leasehold improvements — each governed by distinct rules for methods and useful life periods.

Tangible assets represent physical property that companies use in business operations. This category encompasses buildings, attached facilities like elevators and air conditioning systems, structures such as bridges and fences, machinery and equipment, vehicles, tools and instruments, and furniture and fixtures. The tangible nature of these assets means they experience physical deterioration over time, which the depreciation process reflects through systematic cost allocation.

Intangible assets consist of non-physical property rights that provide economic benefits to the business. Patents and trademarks, software and technology licenses, goodwill acquired through business combinations, and mining rights all fall within this category. Japanese tax law generally requires intangible assets to follow straight-line amortization — for instance, internally used software carries a statutory useful life of 5 years, while software developed for market sale depreciates over just 3 years, reflecting rapid technological obsolescence.

Leasehold improvements occupy a special position within the depreciation framework. When companies rent office or retail space and invest in customizing that space, these improvements technically belong to the property owner. However, Japanese tax law recognizes that tenants receive economic benefit from these improvements during the lease period. Consequently, leasehold improvements follow unique depreciation rules that consider both the improvement type and the remaining lease term.

Japanese tax law provides two primary depreciation methods for tangible assets: the straight-line method and the declining-balance method. The choice between these methods significantly impacts the timing of tax deductions, making method selection an important tax planning consideration. However, this choice comes with important restrictions based on when assets were acquired and what type they represent.

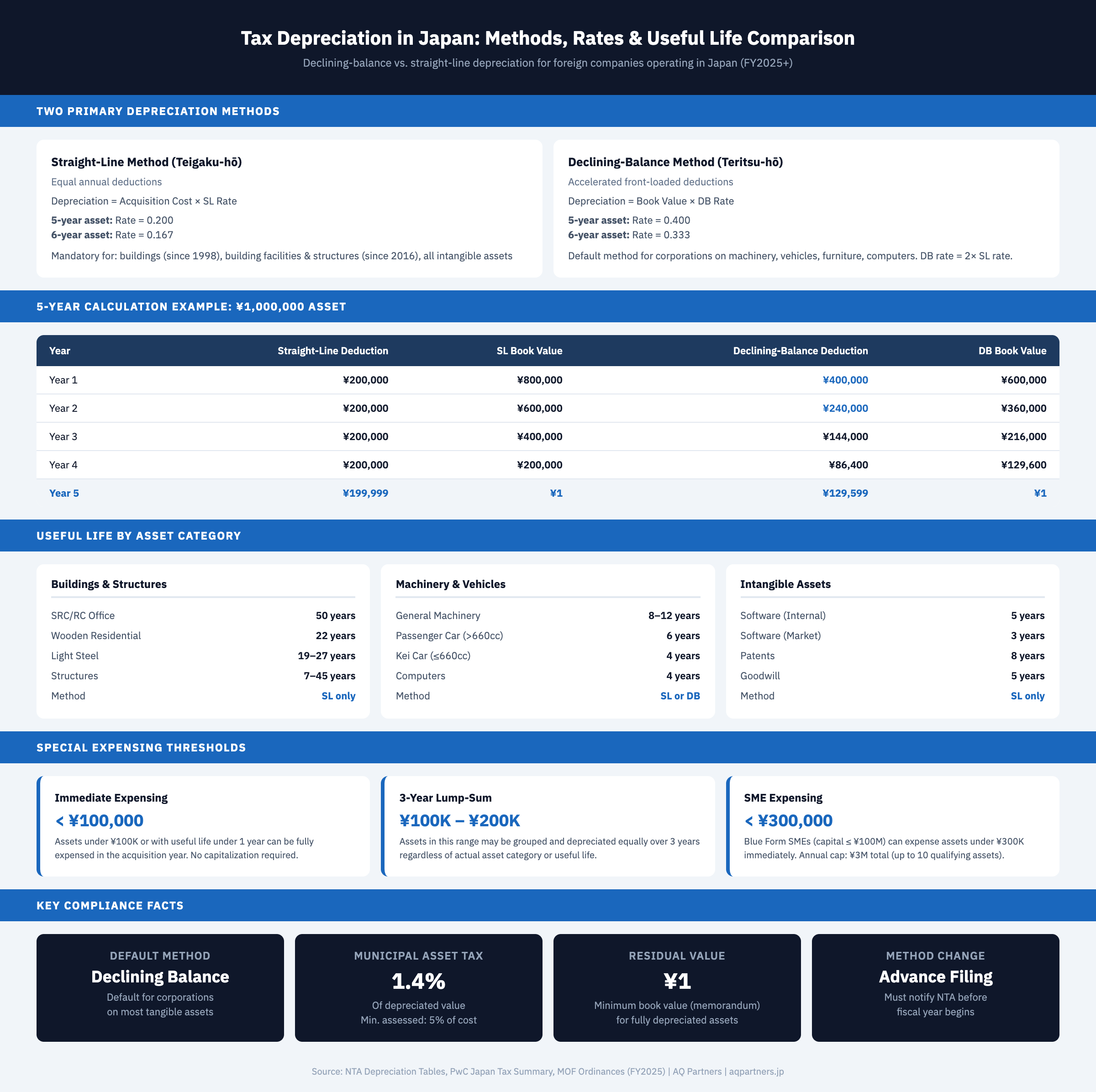

The straight-line method distributes depreciation evenly across an asset's useful life. Companies calculate annual depreciation by multiplying the asset's acquisition cost by its depreciation rate, which corresponds to the mandated useful life period. For instance, an asset with a 6-year useful life carries a straight-line depreciation rate of 0.167, representing one-sixth of its cost per year.

The declining-balance method accelerates depreciation by applying a rate to the asset's remaining book value each year rather than its original cost. This approach front-loads depreciation deductions, recognizing higher expenses in early years. For the same 6-year asset, the declining-balance rate would be 0.333 — exactly double the straight-line rate. Each subsequent year, this rate applies to the diminishing book value, creating naturally decreasing depreciation amounts.

Japanese tax law underwent significant changes in depreciation policy over the past two decades. For assets acquired after April 1, 2007, the system uses "new" straight-line and declining-balance methods with specific rate tables. More restrictively, buildings acquired after April 1, 1998 cannot use declining-balance depreciation — only straight-line is permitted. Similarly, facilities attached to buildings and structures acquired after April 1, 2016 must follow straight-line depreciation exclusively, per revisions published by the Ministry of Finance.

Companies must notify tax authorities of their chosen depreciation method for each asset category. Without such notification, the statutory default method applies automatically. For corporations, the declining-balance method serves as the default for most tangible assets except those explicitly restricted to straight-line.

Statutory Useful Life Periods and Rate Tables

The Ministry of Finance prescribes detailed useful life periods for virtually every conceivable business asset — companies must follow the prescribed periods corresponding to their asset categories, not their own estimates.

Buildings represent the longest-lived asset category, with useful lives varying dramatically based on construction materials and purpose. Wooden residential structures carry a 22-year useful life, while steel-framed reinforced concrete (SRC) office buildings depreciate over 50 years. Lightweight steel buildings fall somewhere in between, with useful lives ranging from 19 to 27 years depending on the thickness of the steel frame.

Machinery and equipment useful lives depend on the specific industry and application. General-purpose machinery typically depreciates over 8 to 12 years. Computers and peripheral equipment carry 4-year useful lives, reflecting rapid technological change. Servers used exclusively for business operations depreciate over 5 years.

Vehicles follow standardized useful lives based on their classification. Ordinary passenger vehicles with engine displacement exceeding 660cc depreciate over 6 years. Kei vehicles (mini cars with engines under 660cc) have a 4-year useful life. Office furniture and fixtures generally depreciate over 8 to 15 years depending on their specific nature.

| Asset Category | Permitted Depreciation Methods | Typical Useful Life (Years) | Key Notes |

|---|---|---|---|

| Buildings (SRC/RC) | Straight-Line only | 38–50 | Declining-balance prohibited since April 1998 |

| Buildings (Wooden) | Straight-Line only | 22–24 | Varies by purpose (residential vs. commercial) |

| Building Attached Facilities | Straight-Line only | 6–18 | Elevators, HVAC, plumbing; SL-only since April 2016 |

| Structures | Straight-Line only | 7–45 | Bridges, fences, retaining walls; SL-only since April 2016 |

| Machinery & Equipment | Straight-Line or Declining-Balance | 4–12 | Varies widely by industry and machine type |

| Vehicles (Passenger, >660cc) | Straight-Line or Declining-Balance | 6 | Default method is declining-balance for corporations |

| Vehicles (Mini, ≤660cc) | Straight-Line or Declining-Balance | 4 | Kei-cars commonly used in Japan |

| Computers & Peripherals | Straight-Line or Declining-Balance | 4 | Servers depreciate over 5 years |

| Furniture & Fixtures | Straight-Line or Declining-Balance | 8–15 | Desks, chairs, shelving, safes, etc. |

| Software (Internally Used) | Straight-Line only | 5 | Intangible asset; amortized on SL basis |

| Software (Market Sales) | Straight-Line only | 3 | Shorter life reflects rapid market obsolescence |

| Patents | Straight-Line only | 8 | Intangible asset; amortized over remaining legal life |

| Goodwill | Straight-Line only | 5 | Tax amortization of acquired goodwill |

Calculating Depreciation: Practical Examples

Understanding the calculation mechanics clarifies how different methods impact actual tax deductions — the choice between straight-line and declining-balance can shift hundreds of thousands of yen in deductions between early and later years of an asset's life.

Consider a company purchasing new manufacturing equipment for ¥1,000,000 with a 5-year useful life. The straight-line depreciation rate for 5 years equals 0.200, while the declining-balance rate equals 0.400.

Under the straight-line method, the annual depreciation remains constant at ¥200,000 throughout the equipment's life (¥1,000,000 × 0.200). Year one produces a ¥200,000 deduction, as does year two, year three, and so forth. After five years, the equipment's book value reaches a minimal residual value of ¥1. This consistency makes budgeting straightforward.

The declining-balance method tells a different story. In year one, depreciation equals ¥400,000 (¥1,000,000 × 0.400). Year two applies the same rate to the reduced value: ¥240,000 (¥600,000 × 0.400). Year three generates ¥144,000, year four ¥86,400, and year five ¥129,599 (adjusted to reach the ¥1 residual). The total depreciation matches the straight-line method, but the timing dramatically differs — 64% of total deductions occur in the first two years under declining-balance versus 40% under straight-line.

This timing difference creates important tax planning implications. Companies expecting higher profitability in their early years might prefer declining-balance to maximize deductions when tax rates hit profits hardest. Conversely, businesses anticipating future growth might choose straight-line to preserve larger deductions for later periods when taxable income rises.

Partial-year depreciation adds another calculation layer. When companies acquire assets partway through their fiscal year, they must prorate the first year's depreciation based on the number of months the asset remained in service. An asset placed in service on October 1 would generate only six months' depreciation for that fiscal year (6/12 of the annual amount).

Special Rules, SME Benefits, and Exceptions

Japanese tax law provides several exceptions to standard depreciation rules — primarily designed to reduce administrative burden for smaller purchases and incentivize certain business investments by SMEs and companies in designated sectors.

The low-value asset rule allows immediate expensing of items costing less than ¥100,000 or having useful lives under one year. Instead of capitalizing and depreciating these purchases, companies can deduct the full amount as a necessary expense in the acquisition year.

The minor depreciable asset rule addresses purchases between ¥100,000 and ¥200,000. Rather than following standard useful life schedules, companies can elect to depreciate these assets equally over three years regardless of their technical classification.

Small and medium-sized enterprises enjoy an additional benefit through the special SME expensing rule. Companies with stated capital of ¥100 million or less can immediately expense assets costing less than ¥300,000, provided they maintain Blue Form tax filing status. This provision carries an annual cap of ¥3 million — meaning an SME could expense up to ten ¥300,000-yen assets in a single year but no more. According to PwC's Japan corporate tax summary, this benefit applies to each consolidated fiscal year individually.

Special depreciation provisions encourage specific types of capital investments deemed beneficial to Japan's industrial policy goals. Companies investing in environmentally friendly equipment, advanced robotics, or designated regional development zones may qualify for accelerated depreciation rates exceeding standard methods. The JETRO business setup guide notes that these incentives are periodically revised as part of Japan's annual tax reform process, making it important to verify current eligibility criteria.

Book-Tax Differences and Depreciable Asset Tax

The divergence between Japanese GAAP accounting and tax depreciation rules creates timing differences that companies must carefully track — plus, a separate municipal tax applies directly to depreciable asset values.

When a company adopts declining-balance depreciation for tax purposes while using straight-line for financial statements, early years generate deferred tax liabilities. Tax depreciation exceeds book depreciation, reducing current taxable income below accounting income. The company pays less tax now than its financial statements suggest, creating a liability that reverses in later years. Companies navigating both Japanese and international accounting frameworks must pay special attention to these reconciliation requirements.

The magnitude of these timing differences can be substantial, particularly for capital-intensive businesses. A manufacturing company making heavy equipment investments might show millions of yen in deferred tax liabilities from depreciation differences alone. These amounts affect reported profitability and balance sheet leverage ratios, making them important considerations for companies seeking financing. Proper setup of the chart of accounts is essential for tracking these parallel schedules.

Tax return preparation requires meticulous tracking of all depreciation-related adjustments. Companies must maintain detailed fixed asset registers showing both book and tax depreciation schedules for each asset. When preparing corporate income tax returns in Japan, accountants identify every item where tax depreciation differs from book depreciation, calculating the precise adjustment amount.

Beyond corporate income tax, depreciation directly impacts depreciable asset tax (shokyaku shisan zei) — a municipal tax that often surprises foreign companies. Municipalities assess this tax at a standard rate of approximately 1.4% of an asset's taxable value as of January 1 each year. As assets depreciate for tax purposes, their depreciable asset tax burden diminishes correspondingly. However, the minimum assessed value generally cannot fall below 5% of original cost, ensuring some tax remains due even for fully depreciated assets still in use.

Companies must file annual depreciable asset tax returns with each municipality where they operate business facilities by January 31. The threshold for this tax kicks in when total asset values in a single municipality exceed ¥1.5 million. For detailed guidance on meeting these and other obligations, refer to our Japanese tax filing and compliance guide.

Common Pitfalls and Compliance Considerations

Foreign companies frequently encounter depreciation-related compliance issues stemming from unfamiliarity with Japanese tax requirements — proper classification, method election, and documentation are the three areas where errors are most costly.

One persistent mistake involves applying home-country depreciation practices without adapting to local rules. A U.S. parent company might instruct its Japanese subsidiary to depreciate computers over three years, matching American MACRS schedules, when the NTA's corporate tax framework prescribes four years. Similarly, a European parent using IFRS useful life estimates of 3–5 years for office furniture would conflict with Japan's 8–15 year range for the same assets.

Another common error arises from improper asset classification. Companies sometimes categorize leasehold improvements as buildings, applying inappropriate useful lives to tenant improvements. Misclassifying machinery as structures or vice versa can similarly produce incorrect depreciation amounts that trigger penalties upon audit.

Failing to file required depreciation method elections represents a frequent oversight, particularly for newly established subsidiaries. Companies sometimes assume they can choose their preferred method retroactively or switch methods freely. In reality, method selection requires advance notification, and missing these filing deadlines locks companies into statutory default methods. Keeping track of the Japan tax filing schedule and key dates is critical to avoid these missteps.

Documentation requirements extend beyond mere calculations to encompass detailed asset registers, acquisition receipts, and supporting materials proving asset classifications and useful lives. Tax authorities conducting audits expect companies to produce comprehensive records explaining every depreciation-related decision.

The complexity of managing these requirements has led many foreign companies considering entity structuring in Japan to seek professional assistance from the outset. Experienced tax advisors specializing in Japanese compliance can navigate the intricate depreciation rules, ensure proper method selection, maintain compliant documentation, and optimize tax positions within legal boundaries.

Frequently Asked Questions

What depreciation methods are available in Japan?

Japan provides two primary methods: straight-line and declining-balance. Straight-line spreads depreciation evenly across an asset's useful life, while declining-balance front-loads deductions by applying the rate to remaining book value each year. Buildings must use straight-line (since 1998), and building facilities and structures have been restricted to straight-line since 2016. For other tangible assets like machinery, vehicles, and computers, corporations default to declining-balance unless they file a notification choosing straight-line.

How are useful life periods determined in Japan?

The Ministry of Finance prescribes mandatory useful life periods through detailed ordinance tables. Companies cannot choose their own estimates. Useful lives range from 3 years (market-sale software) to 50 years (reinforced concrete office buildings). Common periods include 4 years for computers, 6 years for passenger vehicles, 5 years for internally used software, and 8–15 years for furniture and fixtures. The prescribed useful life determines the depreciation rate applied each year.

Can small businesses expense assets immediately?

Yes, with limits. All companies can immediately expense items costing less than ¥100,000 or with useful lives under one year. Items between ¥100,000 and ¥200,000 can be depreciated over three years regardless of category. SMEs with capital of ¥100 million or less holding Blue Form filing status can additionally expense assets under ¥300,000 immediately, subject to an annual cap of ¥3 million total. These thresholds significantly reduce administrative burden for routine equipment purchases.

What is depreciable asset tax?

Depreciable asset tax is a municipal tax of approximately 1.4% levied on the depreciated value of business-use tangible assets as of January 1 each year. It applies separately from corporate income tax. Companies must file returns with each municipality where they hold assets by January 31, and the tax applies when total asset values in a single municipality exceed ¥1.5 million. The minimum assessed value is 5% of original cost, ensuring some tax remains due on fully depreciated assets still in use.

What happens if we use the wrong depreciation method?

Using an incorrect depreciation method — whether by applying home-country rules, misclassifying asset categories, or failing to file method elections on time — can result in incorrect tax deductions that trigger penalties upon NTA audit. Over-claimed depreciation must be added back to taxable income with potential additional tax, penalties, and interest. Companies must notify tax authorities of their chosen method before the fiscal year begins; missing this deadline defaults to declining-balance for corporations on eligible assets.

For guidance on navigating Japan's depreciation system and broader tax compliance, including corporate tax filing and local tax obligations, contact AQ Partners for a consultation.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.