Japanese Tax Filing & Compliance Guide

Key Takeaways

- Japan's corporate tax system operates on multiple layers — national, prefectural, and municipal — producing a combined effective rate of approximately 30–35% depending on company size and location. Filing obligations span corporate income tax, consumption tax, withholding tax, enterprise tax, and inhabitants tax.

- All major tax returns are due within two months of fiscal year-end — consumption tax permits no extensions, while corporate income tax allows a one-month filing extension (though payment remains due at the original deadline). Missing deadlines triggers penalties of 15–20%, or up to 40% for fraud.

- Blue Form tax return status is essential for foreign companies — it enables 10-year loss carryforward, special depreciation, and enhanced deductions. Application must be filed within three months of incorporation, making it a day-one priority.

- Withholding tax on cross-border payments defaults to 20.42% — covering dividends, royalties, interest, and service fees paid to non-residents. Tax treaty benefits can reduce rates to 5–10%, but require advance documentation filed before payment dates.

- Transfer pricing documentation must be prepared contemporaneously — retroactive documentation receives less credibility from the NTA. Companies with consolidated group revenue exceeding ¥100 billion face enhanced Country-by-Country reporting obligations.

Japan's Corporate Tax Filing System

Japan tax filing for corporations refers to the set of annual, interim, and monthly compliance obligations that companies must satisfy across national, prefectural, and municipal tax authorities. For foreign companies operating in Japan, the system encompasses corporate income tax, consumption tax, withholding tax, enterprise tax, inhabitants tax, and transfer pricing documentation — each with distinct deadlines, calculation methods, and filing destinations.

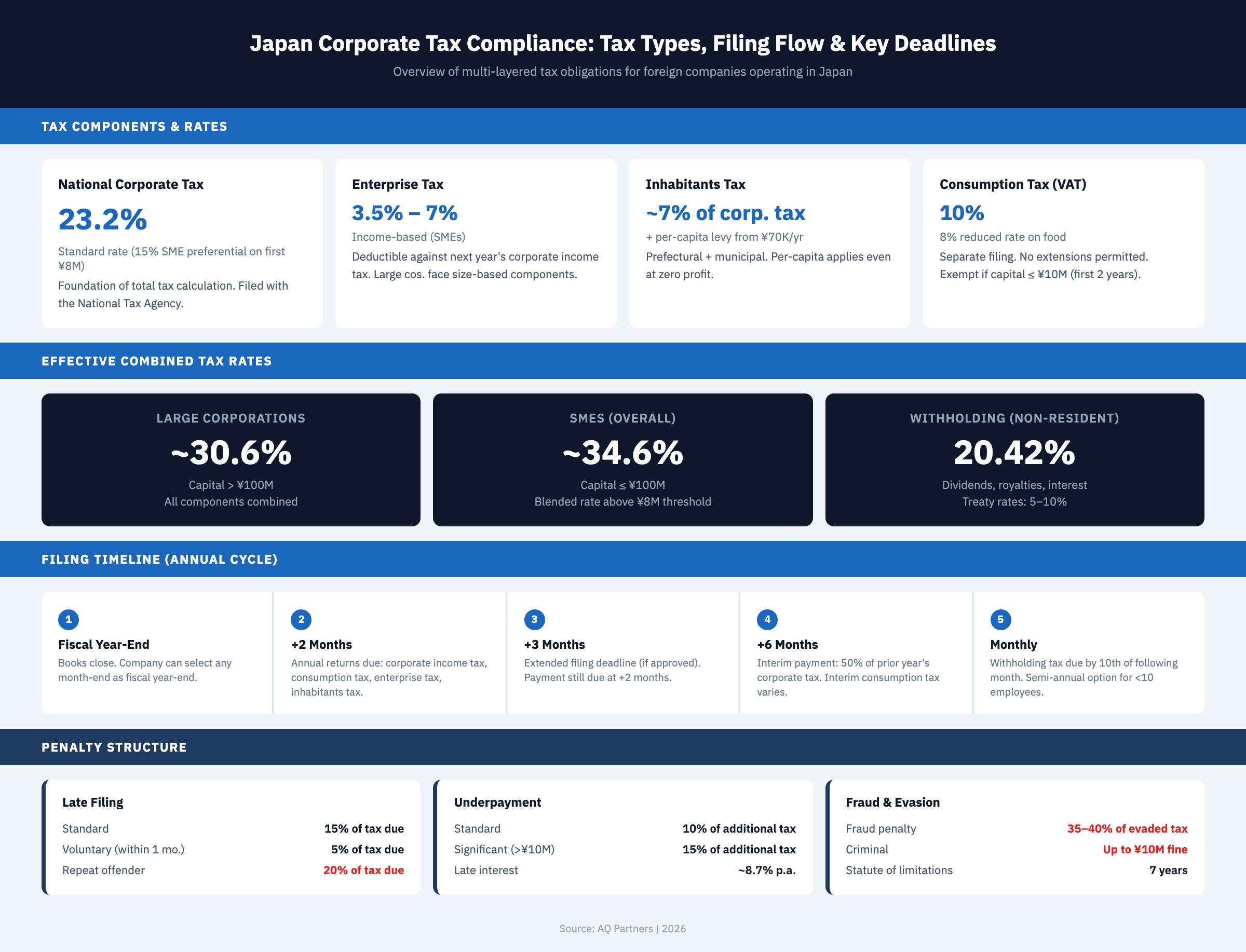

The multi-layered structure differs fundamentally from single-jurisdiction tax systems in many Western countries. According to PwC's Worldwide Tax Summaries, Japan's combined effective corporate tax rate ranges from approximately 31.5% for large corporations to 35.4% for SMEs, placing it in the upper-middle range among OECD economies. The National Tax Agency (NTA) administers national taxes, while prefectural and municipal offices handle local levies independently.

Understanding each component is essential for accurate compliance planning and cash flow management. As covered in our comprehensive Japan Market Entry guide, tax compliance forms a critical pillar of successful back office operations. This guide walks you through the tax structure, filing deadlines, withholding obligations, and compliance best practices for foreign companies in Japan.

Corporate Tax Structure and Rate Components

Japan's corporate tax consists of five primary components that combine into the total tax obligation. Each component applies different rates and calculation bases, requiring companies to file with multiple authorities simultaneously.

| Tax Type | Filing Deadline | Extension Available | Key Notes for Foreign Companies |

|---|---|---|---|

| Corporate Income Tax (national and local) | 2 months after fiscal year-end | Yes (1-month extension for filing only; tax payment still due at original deadline) | Must file with national tax office and each prefectural/municipal office where operations exist |

| Consumption Tax | 2 months after fiscal year-end | No extension permitted | Most rigid deadline; payment must accompany the return with no deferral option |

| Corporate Inhabitant Tax | 2 months after fiscal year-end | Yes (follows corporate income tax extension) | Separate returns required for each prefecture and municipality with offices |

| Enterprise Tax and Special Enterprise Tax | 2 months after fiscal year-end | Yes (follows corporate income tax extension) | Enterprise tax is deductible against the following year's corporate income tax |

| Interim Corporate Tax Payment | 6 months after fiscal year start | No | Required when prior year corporate tax exceeds ¥200,000; typically 50% of prior year liability |

| Interim Consumption Tax Payment | Varies (semi-annual, quarterly, or monthly) | No | Frequency depends on prior year tax amount; monthly payments required when exceeding ¥48 million |

| Employment Withholding Tax | 10th of the following month | No (semi-annual option for companies with fewer than 10 employees) | Register as withholding agent within 1 month of first salary payment |

| Non-Resident Withholding Tax (dividends, royalties, fees) | 10th of the month following payment | No | Standard rate 20.42%; treaty rates may apply with advance documentation |

| Fixed Asset Tax Return | January 31 (calendar year basis) | No | Reports all depreciable assets acquired during the prior calendar year |

| Blue Form Application (new companies) | Within 3 months of incorporation or day before first fiscal year-end | No | Critical for loss carryforward eligibility; must be filed early to avoid losing first-year benefits |

The national corporate income tax rate stands at 23.2% for most companies, with SMEs (paid-in capital of ¥100 million or less) benefiting from a preferential 15% rate on the first ¥8 million of taxable income. Local corporate tax adds 10.3% of the national corporate tax amount. For a detailed breakdown of rate components and calculation methods, see our guide on corporate income tax rates and calculation in Japan.

Corporate inhabitant tax combines a per-capita levy (starting at ¥70,000 annually for small companies) with an income-based component of approximately 7% of national corporate tax. Enterprise tax varies from 3.5% to 7% depending on income levels for SMEs, while large companies face additional value-added and capital-based components. Special corporate enterprise tax adds 37% of standard enterprise tax for most companies. For complete coverage of local tax obligations, see our local enterprise tax and inhabitants tax guide.

Enterprise tax is uniquely deductible against corporate income tax for the following fiscal year — a characteristic that effectively lowers the combined rate. When all layers combine, the effective corporate tax rate ranges from approximately 30.6% for large companies to 34.6% for SMEs, according to JETRO's business setup guide.

Filing Deadlines and Interim Payments

Meeting Japan's corporate tax filing deadlines requires precise calendar management and coordination between accounting teams, tax advisors, and business operations. The primary corporate tax filing deadline falls two months after fiscal year-end — companies with a March 31 year-end face a May 31 deadline, while December 31 year-end companies must file by end of February. This two-month window applies to corporate income tax, local corporate tax, inhabitant tax, enterprise tax, and special corporate enterprise tax simultaneously. The filing deadline covers all national and local tax returns, requiring companies operating in multiple prefectures to submit separate returns for each jurisdiction where they maintain offices.

Japanese tax law permits a one-month filing extension for corporate income tax when companies demonstrate unavoidable circumstances such as delayed shareholder meetings or unfinished statutory audits. The extension application must be filed before the original deadline. However, this extension applies only to filing — companies must still pay estimated taxes by the original deadline to avoid interest charges. Companies should review our detailed Japan tax filing schedule for a complete calendar of deadlines.

Consumption tax follows the same two-month deadline but permits no extensions whatsoever. Companies must file and pay consumption tax exactly two months after fiscal year-end, making it the most rigid deadline in the Japanese tax calendar. Missing this deadline triggers automatic penalties and interest without exception.

Interim Tax Payments

Companies with prior year corporate tax exceeding ¥200,000 face interim payment requirements at the six-month mark, typically equal to 50% of prior year liability. Companies expecting current year profitability to fall below prior year levels may elect to file an interim return based on actual first-half performance, providing cash flow relief.

Interim consumption tax payments apply when prior year consumption tax exceeds ¥480,000. The frequency escalates with the prior year tax amount: one payment for tax between ¥480,000 and ¥4 million, three quarterly payments for ¥4–48 million, and eleven monthly payments for tax exceeding ¥48 million.

Withholding Tax Payment Schedule

Employment income withholding follows the calendar year with monthly payments due by the 10th of the following month. Small companies with fewer than 10 employees can apply for semi-annual payment approval, remitting twice yearly by July 10 and January 10. Withholding on payments to non-residents (dividends, royalties, service fees) requires payment by the 10th of the month following payment, with no semi-annual option available.

Penalties, Interest, and Enforcement

Japan's tax penalty framework escalates based on the severity and nature of non-compliance. Understanding the penalty structure helps companies prioritize compliance efforts and assess the financial risk of filing delays or errors.

| Penalty Type | Rate / Amount | Trigger | Notes |

|---|---|---|---|

| Late filing penalty (standard) | 15% of tax due | Filing after the statutory deadline | Applies to all tax types; reduced to 5% if filed within one month voluntarily |

| Late filing penalty (repeat offenders) | 20% of tax due | Late filing within 5 years of a prior late filing penalty | Enhanced rate applies automatically for pattern of non-compliance |

| Underpayment penalty (standard) | 10% of additional tax | Tax assessment reveals underpayment | Applies when original return underreported income or overclaimed deductions |

| Underpayment penalty (significant) | 15% of additional tax | Underpayment exceeds ¥10 million or 10% of original tax | Higher rate applies to the portion exceeding the threshold |

| Fraud penalty | 35–40% of evaded tax | Deliberate concealment of income or fabrication of deductions | May also trigger criminal prosecution; statute of limitations extends to 7 years |

| Late payment interest (delinquent tax) | ~8.7% per annum (first 2 months: ~2.4%) | Tax payment after due date | Accrues daily; rate adjusted annually based on market interest rates |

| Transfer pricing penalty | 10–15% of additional tax assessed | Failure to maintain contemporaneous documentation | 15% applies when adjustment exceeds ¥10 million or 10% of total expenses |

| Withholding tax failure | 10% of tax that should have been withheld | Failure to withhold or late remittance | Withholding agent bears full liability regardless of recipient cooperation |

| Blue Form revocation | Loss of all Blue Form benefits | Significant accounting irregularities, deliberate evasion, or chronic late filing | Revocation eliminates 10-year loss carryforward and special deductions prospectively |

| Criminal penalties | Up to ¥10 million fine and/or imprisonment up to 10 years | Tax evasion through fraud or concealment | NTA refers approximately 150 cases annually for criminal prosecution |

The NTA uses risk-based selection to identify companies for examination. Common triggers include inconsistent reporting across tax types, significant year-over-year changes, and foreign company structures with cross-border complexity. Large companies face examination approximately every three to five years, while smaller companies experience longer intervals. According to NTA annual reports, the agency conducts over 90,000 corporate tax examinations per year, with approximately 75% resulting in some form of adjustment.

When examinations result in proposed adjustments, companies may pursue informal resolution, formal reconsideration from the regional taxation bureau, or appeal to the National Tax Tribunal. Tribunal proceedings typically require 12–18 months, making proactive compliance substantially more cost-effective than dispute resolution. Preparation significantly impacts examination outcomes — companies should maintain organized documentation, establish clear retention policies, and ensure accounting records reflect actual transactions accurately.

Withholding Tax and Blue Form Benefits

Withholding tax and Blue Form status represent two critical compliance areas where early action and proper systems prevent costly errors for foreign companies operating in Japan.

Withholding Tax Obligations

All companies paying employment income in Japan must withhold national income tax from employee salaries based on NTA-published tax tables. Companies must register as withholding agents within one month of making the first salary payment. Beyond national income tax, companies must withhold special reconstruction income tax at 2.1% of the national income tax amount — a temporary surtax introduced after the 2011 earthquake that extends through 2037. Year-end adjustment in December reconciles annual withholding with actual tax liability, eliminating individual filing requirements for most employees.

Dividend payments to foreign shareholders trigger withholding at a standard rate of 20.42% unless a tax treaty provides reduced rates. Many treaties reduce dividend withholding to 5–10% for qualifying corporate shareholders. Claiming treaty benefits requires advance submission of application forms and residency certificates before the payment date. Royalty, service fee, and interest payments to non-residents face the same 20.42% standard rate, with treaty reductions available through proper documentation. According to PwC's Japan tax summary, withholding obligations extend to technical assistance fees and certain management charges that foreign companies frequently overlook.

Blue Form Tax Return Status

Blue Form status provides significant advantages including 10-year loss carryforward, immediate expensing for depreciable assets under ¥300,000, enhanced bad debt reserves, and access to special depreciation and tax credits. New companies must apply within three months of incorporation or by the day before the first fiscal year-end. The application requires minimal documentation but mandates proper double-entry bookkeeping with seven-year record retention.

Loss carryforward is particularly valuable for startups and foreign companies investing heavily during Japan market entry. Without Blue Form status, loss carryforward is entirely unavailable — making profitable year taxation inevitable regardless of cumulative performance. Companies should implement compliant accounting systems from day one. Our guide on chart of accounts management in Japan provides detailed implementation strategies for Blue Form-compliant bookkeeping.

Consumption Tax and Transfer Pricing

Consumption tax (Japan's 10% VAT) and transfer pricing documentation create distinct compliance obligations that operate alongside corporate income tax but follow separate rules and deadlines.

Consumption Tax

New companies with paid-in capital of ¥10 million or less qualify as consumption tax-exempt businesses for their first two fiscal years. After the exemption period, companies become taxable if base period sales exceed ¥10 million. Japan's standard consumption tax rate is 10% (comprising 7.8% national and 2.2% local), with a reduced 8% rate on food and beverages for home consumption and newspaper subscriptions.

Companies calculate liability using either the general method (output tax minus input tax on actual purchases) or the simplified method (available when base period sales are ¥50 million or less, using industry-specific deemed purchase rates of 50–90%). The simplified method election requires advance notification and commits the company for at least two years. Export-focused businesses benefit from zero-rating, which preserves full input tax deduction rights. For details on asset-related consumption tax treatment, see our guide on tax depreciation and asset categories in Japan.

Transfer Pricing

Transfer pricing rules require that all related-party transactions reflect arm's length pricing — meaning prices, terms, and conditions that independent parties would establish under comparable circumstances. This standard applies to all transaction types: goods sales, service provision, royalty payments, interest charges, and management fees. Japan accepts five primary methods: comparable uncontrolled price, resale price, cost plus, transactional net margin, and profit split. Documentation must be prepared contemporaneously — by the tax return filing deadline — and retained for seven years.

Large companies with consolidated group revenues exceeding ¥100 billion must file Country-by-Country reports within 12 months of fiscal year-end, along with Master Files and Local Files. Companies seeking certainty can pursue Advance Pricing Agreements (APAs), which typically require 12–18 months of negotiation but provide protection from future adjustments. Transfer pricing adjustments can result in penalties of 10–15% of additional tax assessed, plus reputational damage and increased examination frequency.

Compliance Best Practices for Foreign Companies

Building reliable tax compliance requires systematic approaches that address Japan's emphasis on precise documentation, strict deadlines, and detailed record-keeping.

Establish a comprehensive tax calendar tracking all filing deadlines, payment dates, and compliance milestones across every jurisdiction where the company maintains operations. Build buffer time before deadlines and implement automated reminders with escalation procedures. Account for weekends and national holidays — deadlines falling on non-business days shift to the next business day.

Implement accounting systems designed for Japanese tax compliance. Cloud-based solutions with Japanese tax functionality, consumption tax tracking by rate category, and withholding tax calculation reduce manual work and error risk. Integration with payroll and banking systems provides real-time visibility into tax positions.

Maintain documentation standards that exceed minimum requirements. Seven-year retention aligns with statutory requirements. Electronic document management with organized filing structures and consistent naming conventions enables rapid information retrieval during examinations.

Engage qualified advisors with Japanese tax expertise and foreign company experience. Advisors support tax planning, preparation review, examination defense, and dispute resolution. Strong ongoing relationships produce better results than transactional engagement only during examinations.

Coordinate Japanese tax compliance with global tax strategy. Transfer pricing policies, financing structures, and intercompany arrangements require global perspective. Major business decisions should include Japanese tax analysis before implementation to avoid costly restructuring after the fact. For companies comparing frameworks, our guide on Japanese vs. international accounting covers the key differences that affect tax planning.

If you need support navigating Japan's complex tax filing and compliance requirements, AQ Partners specializes in providing comprehensive back office services for foreign companies operating in Japan. Our team handles all aspects of tax compliance — from registration and filing to examination support and strategic planning — allowing you to focus on growing your business. Contact us at hello@aqpartners.jp to learn how we can simplify your Japan tax compliance.

Frequently Asked Questions

What is the corporate tax filing deadline in Japan?

Corporate tax returns are due within two months of fiscal year-end. Companies with a March 31 year-end must file by May 31; those with a December 31 year-end file by end of February. A one-month extension is available for corporate income tax filing (not payment), while consumption tax permits no extension. All returns must be filed with both national and local tax offices where the company maintains operations.

What penalties apply for late tax filing in Japan?

Late filing triggers a standard penalty of 15% of tax due, reduced to 5% if filed voluntarily within one month. Repeat offenders face 20%. Underpayment penalties range from 10–15% of additional tax assessed, while fraud penalties reach 35–40% and may trigger criminal prosecution. Late payment interest accrues daily at approximately 8.7% per annum (reduced to approximately 2.4% for the first two months).

How does Blue Form status benefit foreign companies in Japan?

Blue Form status enables 10-year loss carryforward (unavailable without it), immediate expensing for assets under ¥300,000, enhanced bad debt reserves, and access to special tax credits. New companies must apply within three months of incorporation. The primary requirement is maintaining proper double-entry bookkeeping with seven-year record retention. For startups expecting initial losses before profitability, Blue Form status is essential to preserve tax loss value.

What withholding tax rates apply to payments to non-residents?

The standard withholding rate is 20.42% on dividends, royalties, interest, and certain service fees paid to non-residents. Tax treaties can reduce these rates substantially — often to 5–10% for dividends from substantial shareholders and 0% for qualifying interest payments. Treaty benefits require advance filing of application forms and residency certificates before the payment date. Failure to submit documentation in advance results in withholding at the full standard rate.

What transfer pricing documentation is required in Japan?

All companies with related-party transactions must prepare contemporaneous documentation supporting arm's length pricing by the tax return filing deadline. Large companies (consolidated revenue exceeding ¥100 billion) must additionally file Country-by-Country reports, Master Files, and Local Files. Documentation must be retained for seven years. Failure to maintain proper documentation triggers penalties of 10–15% of any additional tax assessed during examination, and retroactive documentation receives reduced credibility from the NTA.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.