Local Enterprise Tax & Inhabitants Tax: Complete Guide

Key Takeaways

- ● Two local taxes apply to every corporation in Japan: prefectural enterprise tax (calculated on income, value-added, or capital) and inhabitants tax (a percentage of national corporate tax plus a fixed per capita levy) — together they add roughly 10-15 percentage points to the headline national rate, bringing effective rates to 30%-35% for most companies.

- ● Size-based enterprise tax kicks in at 100 million yen paid-in capital, requiring large corporations to compute three separate components (income, value-added, and capital). According to MIC local public finance data, local corporate taxes generated approximately 8.5 trillion yen in FY2023 revenue for sub-national governments.

- ● Per capita inhabitants tax applies even when your company posts a loss. The annual levy ranges from 70,000 yen (small companies with fewer than 50 employees) to approximately 3.8 million yen for large corporations with capital exceeding 10 billion yen.

- ● Enterprise tax is deductible for corporate income tax — but with a one-year lag. Tax paid in the current fiscal year reduces taxable income only in the following year, creating important cash-flow timing differences.

- ● 2026 reforms raise the bar: a 4% defense surtax on national corporate tax (effective FY beginning April 2026) compounds through to inhabitants tax, and expanded size-based rules now capture subsidiaries of large groups regardless of nominal capital.

Local enterprise tax (jigyouzei) and corporate inhabitants tax (houjin juminzei) are the two prefectural and municipal levies that every corporation in Japan must pay in addition to national corporate income tax. Enterprise tax is assessed by prefectures primarily on business income — or, for large corporations, on a combination of income, value-added, and capital bases. Inhabitants tax is assessed by both prefectures and municipalities as a percentage of national corporate tax liability plus a fixed per capita levy that applies even in loss-making years. Together, these local taxes typically add 10 to 15 percentage points to a company's effective rate, producing combined rates of approximately 30% to 35% depending on company size and location.

For foreign companies entering Japan, these local taxes often come as an unexpected addition to their financial planning. The terminology itself can be confusing, as both enterprise tax and inhabitants tax apply to corporate entities despite one containing the word "inhabitants" in its English translation. Understanding these obligations early in the incorporation process helps companies budget accurately and avoid compliance issues that could jeopardize their Japan operations. Beyond national corporate income tax, mastering local taxes is essential for realistic financial modeling.

This comprehensive guide examines both local enterprise tax and corporate inhabitants tax, explaining their calculation methods, filing requirements, and strategic considerations for foreign businesses. Whether you're establishing your first Japan entity or managing an existing operation, mastering these local tax obligations is essential for successful business operations in Japan.

Understanding Japan's Local Tax Framework

Japan taxes corporations at three distinct levels — national, prefectural, and municipal — and the two local layers account for roughly one-third of the total corporate tax burden. The national government collects corporate income tax, while prefectures and municipalities each impose their own local taxes on business activities. According to the Ministry of Internal Affairs and Communications (MIC), local tax revenue constituted approximately 40.9% of total tax revenue in Japan in FY2023, underscoring the importance of sub-national taxation in the country's fiscal system.

The two primary local taxes affecting corporations are enterprise tax, levied by prefectures, and inhabitants tax, imposed by both prefectures and municipalities. Enterprise tax compensates prefectures for the infrastructure and public services that enable business operations. Inhabitants tax contributes to local community services in the specific municipalities where a company maintains offices or facilities.

This decentralized tax structure reflects Japan's constitutional framework, which grants significant autonomy to local governments in fiscal matters. Prefectures and municipalities have some flexibility in setting tax rates within nationally defined ranges, though most jurisdictions apply standard rates to maintain competitiveness and avoid creating unintended tax incentives or disincentives for business location decisions.

For businesses operating in multiple prefectures, this creates additional complexity. A company with offices in both Tokyo and Osaka must file separate local tax returns for each jurisdiction, apportioning income and calculating taxes according to each location's specific rules. The allocation formulas consider factors such as the number of employees and office space in each jurisdiction, ensuring that tax revenue flows to the localities where business activities actually occur.

Local Enterprise Tax: Rates, Calculation Methods & Size-Based Components

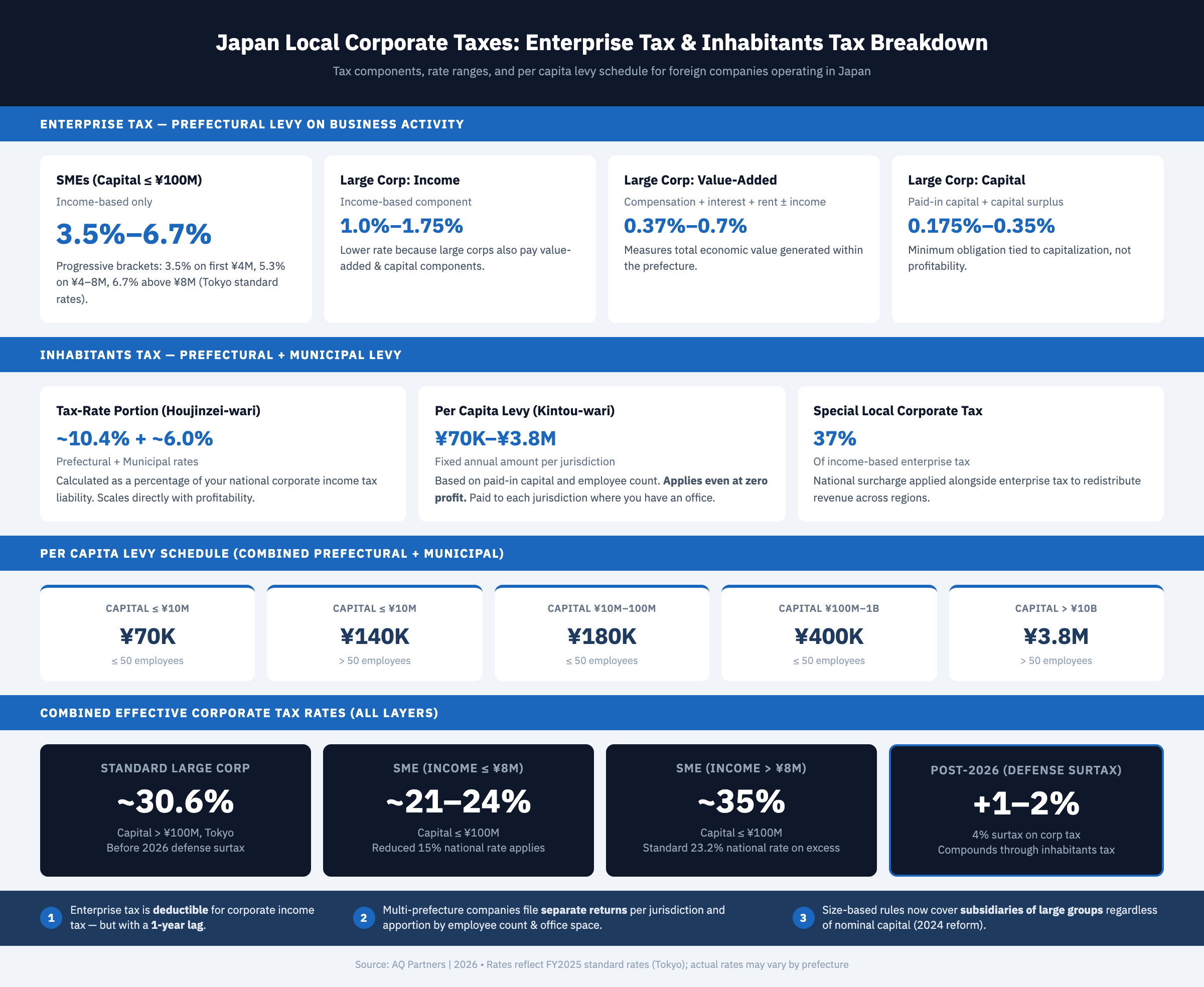

Enterprise tax rates range from 3.5% to 6.7% for SMEs (income-based only) and use a three-component formula — income, value-added, and capital — for corporations with paid-in capital above 100 million yen.

SME Enterprise Tax (Paid-in Capital of 100 Million Yen or Less)

Small and medium-sized enterprises face a relatively straightforward income-based calculation. Their enterprise tax is computed by applying progressive tax rates to their taxable income as determined for national corporate tax purposes, with certain adjustments applied. In Tokyo, for example, SMEs face a 3.5% rate on income up to 4 million yen, a 5.3% rate on income between 4 million and 8 million yen, and a 6.7% rate on income exceeding 8 million yen. These rates may vary slightly in other prefectures, though most jurisdictions apply standard or near-standard rates.

Tokyo applies higher-than-standard enterprise tax rates compared to other prefectures. This reflects the concentration of corporate headquarters and large businesses in the capital, as well as the higher cost of maintaining Tokyo's extensive infrastructure. Companies establishing operations in Tokyo should factor these elevated rates into their financial planning and compare the effective tax burden against operating in other major business centers like Osaka or Nagoya.

Size-Based Enterprise Tax (Paid-in Capital Exceeding 100 Million Yen)

Large corporations face a more complex three-component enterprise tax system introduced to stabilize prefectural tax revenues regardless of annual profitability. The National Tax Agency (NTA) coordinates the national corporate tax base that feeds into these local calculations.

Income-based component: Large corporations pay approximately 1.0% to 1.75% on their enterprise tax income base — lower than SME rates because these companies also pay the value-added and capital components. The income base calculation follows similar principles to those used for smaller companies, starting with corporate taxable income and making specific adjustments.

Value-added component: This component requires calculating "value added" as the sum of employee compensation (salaries, bonuses, retirement allowances), net interest expense (interest paid minus interest received), and net rental payments (rent paid for real property minus rent received), added to taxable income. The value-added base essentially measures the total economic value generated by operations within the prefecture. The tax rate is approximately 0.37% to 0.7% depending on the prefecture. A labor-intensive service company with high payroll costs will face a substantial value-added base even in years with modest profits.

Capital-based component: This applies a rate of approximately 0.175% to 0.35% to the company's paid-in capital plus capital surplus at fiscal year-end. For companies with billions of yen in paid-in capital, this component alone can generate significant annual tax liability. Unlike the income-based component, there is no way to reduce this obligation through operational losses or deductions.

Recent Expansion of Size-Based Rules

The 2024 tax reforms expanded the scope of size-based taxation. Previously, the system applied primarily to companies with paid-in capital exceeding 100 million yen. Recent changes now include wholly-owned subsidiaries of larger corporations and companies with total paid-in capital and capital surplus exceeding certain thresholds, even if their nominal paid-in capital falls below 100 million yen. This prevents avoidance strategies that kept capital artificially low. Transitional tax credits may be available for a limited period for companies newly subject to size-based taxation, but these reliefs are temporary.

Enterprise Tax Deductibility

When calculating enterprise tax, companies must remember that this tax itself becomes deductible in the following fiscal year for corporate income tax purposes. This means that while enterprise tax paid in year one is an expense that reduces taxable income in year two, it does not reduce the current year's tax burden. This deferred deductibility affects cash flow planning and requires companies to account for timing differences between tax payment and tax benefit.

Corporate Inhabitants Tax & Per Capita Levy

Corporate inhabitants tax has two parts: a "tax-rate portion" pegged to your national corporate tax liability, and a fixed per capita levy of 70,000 to 3,800,000 yen per year that applies even at zero profit.

Tax-Rate Portion (Houjinzei-wari)

The corporate tax rate portion is calculated as a percentage of the company's national corporate income tax liability before certain tax credits. In Tokyo, the prefectural inhabitants tax typically applies at a rate of approximately 10.4% of the national corporate tax amount, while municipal inhabitants tax adds additional percentage points. These rates can vary somewhat in other jurisdictions, though most prefectures and municipalities stay within relatively narrow ranges. This creates a straightforward linkage between national and local tax obligations — when national corporate tax increases, inhabitants tax rises proportionally.

Per Capita Levy (Kintou-wari)

The per capita levy component represents a fixed annual amount that every corporation must pay regardless of profitability. This levy varies based on two primary factors: the company's paid-in capital and the number of employees. According to the PwC Japan corporate tax summary, the per capita levy schedule operates as follows:

- Capital of 10 million yen or less, 50 or fewer employees: approximately 70,000 yen per year (combined prefectural and municipal)

- Capital of 10 million to 100 million yen: intermediate amounts that increase with employee count thresholds

- Capital exceeding 1 billion yen with more than 50 employees: levies reaching several million yen annually

- Capital exceeding 10 billion yen with more than 50 employees (Tokyo): maximum per capita levy of approximately 3,800,000 yen

During difficult economic periods when a company reports losses, the per capita levy remains due in full. This distinguishes it fundamentally from income-based taxes, which naturally decrease during low-profit periods. Financial planning for Japan operations must account for these minimum tax obligations that persist independent of profitability. The variation across different prefectures and municipalities is relatively modest, though companies should verify the specific schedule in each jurisdiction where they operate.

Multi-Jurisdiction Inhabitants Tax

Companies operating in multiple prefectures and municipalities must pay separate inhabitants tax to each jurisdiction where they maintain an office or facility. The apportionment of the corporate tax rate portion follows specific formulas based on factors such as employee count and office space in each location. The per capita levy, however, is paid separately to each jurisdiction based on the local presence in that specific area.

Filing, Payments & Deadlines

All local tax returns are filed together with the national corporate income tax return, due two months after fiscal year-end, with an optional one-month extension available upon application.

Filing Requirements

Companies file a single comprehensive return covering corporate income tax, inhabitants tax, and enterprise tax. This integrated approach reduces paperwork burden while ensuring coordinated compliance across all tax levels. For a detailed walkthrough, see our Japanese tax filing and compliance guide.

The standard filing deadline falls two months after the end of a company's fiscal year. For companies with a March 31 fiscal year-end, the deadline is May 31. Calendar-year companies face a February 28 deadline. This relatively short filing window requires companies to close their books and complete all tax calculations efficiently. Our Japan tax filing schedule and key dates overview can help you stay on track.

Companies may request a one-month filing extension, primarily when they need additional time to finalize financial statements. However, even when an extension is granted, companies must pay estimated taxes by the original deadline to avoid late payment penalties and interest charges. For large corporations with paid-in capital exceeding 100 million yen, electronic filing through the NTA's e-Tax system is mandatory.

Interim Payments

Companies whose fiscal year exceeds six months must file an interim return and make interim tax payments covering the first six months of the fiscal year. This interim payment is due within two months after the six-month point. These interim payments are later credited against the final annual tax liability, functioning similarly to estimated tax payments in other countries.

Payment Methods & Late Penalties

Most companies make payments through designated financial institutions or the e-Tax electronic payment system. For businesses operating in multiple prefectures, separate payments must be made to each jurisdiction. Late payment triggers penalties and interest charges. Japan's tax authorities enforce strict deadlines, and companies failing to pay on time face both a penalty for late payment and interest charges on the unpaid amount. The interest rate typically ranges from 2.4% to 8.7% annually, depending on the specific tax and how late the payment is.

Companies experiencing financial difficulties may request payment extensions or installment arrangements, though these are granted sparingly and require demonstrating genuine financial hardship. Tax authorities expect companies to maintain sufficient cash reserves to meet their tax obligations on time.

Tax Planning, National Tax Coordination & Compliance

Enterprise tax's one-year-delayed deductibility and the multiplier effect between national and local layers create planning opportunities — but also traps for foreign companies unfamiliar with Japan's multi-tiered system.

National-Local Tax Interaction

The calculation of local taxes begins with taxable income determined for national corporate income tax purposes. Enterprise tax paid in one fiscal year becomes deductible when calculating taxable income for the following fiscal year. This creates a cascading pattern: this year's enterprise tax reduces next year's corporate income tax, which in turn reduces next year's inhabitants tax since it's calculated as a percentage of corporate tax. Planning for this timing difference is essential for accurate cash flow forecasting, particularly for companies with volatile income levels.

Tax credits and incentives available for corporate income tax may or may not carry through to local taxes. Some national tax credits reduce corporate income tax but don't reduce the base for calculating inhabitants tax. Companies evaluating potential tax benefits must analyze their impact across all tax types to determine true economic value. When the national government adjusts corporate income tax rates, the change automatically affects inhabitants tax, making the effective increase larger than the nominal change in national rates.

Capital Structure & Entity Planning

Companies approaching the 100 million yen paid-in capital threshold should carefully evaluate whether to cross this threshold. While higher capital may support business growth and credibility, it triggers significantly more complex and potentially burdensome local tax obligations. Some companies maintain capital levels just below the threshold, though recent tax reforms have limited this strategy's effectiveness. These considerations are central to developing a sound entity structuring strategy for Japan entry.

Operating structure decisions significantly impact local tax burden. A foreign company can choose between establishing a subsidiary and operating through a branch office. Branches of foreign corporations face the same local tax obligations as domestic corporations but may face different effective tax rates depending on how profits are calculated and allocated. Our comparison of KK vs GK vs branch office structures provides further detail on this decision.

Common Compliance Challenges for Foreign Companies

Foreign companies frequently underestimate the complexity of Japan's local tax system. Many enter the Japanese market with budgets based solely on national corporate income tax rates, only to discover that local taxes add 10 to 15 percentage points to their effective tax rate. The per capita levy catches many companies off guard during loss-making periods — Western tax systems typically don't impose minimum corporate tax obligations on unprofitable companies.

Apportionment across multiple jurisdictions creates calculation errors. Multi-prefecture operations require allocating income, value-added, and capital bases according to complex formulas. The value-added calculation for size-based enterprise tax presents particular challenges, as foreign companies may lack familiarity with segregating employee compensation, interest, and rent in the ways required by Japanese tax law. Accounting systems designed for home-country reporting may not naturally generate the data needed for these formulas.

Electronic filing mandates and Japanese-language documentation requirements create additional barriers. Large corporations must file electronically through Japan's e-Tax system, which may present language and technical challenges. Many companies underestimate the staff hours required for local tax compliance, making professional advisory support essential.

Impact on Foreign Companies & 2026 Tax Reforms

The combined effective corporate tax rate in Japan typically falls between 30% and 35% after local taxes, and new 2026 reforms — including a 4% defense surtax — will push that figure higher for most corporations.

Financial Impact on Foreign Operations

Foreign companies establishing Japan operations must factor local taxes into their market entry financial modeling and back-office planning. The combined burden of national corporate income tax at 23.2%, local corporate tax at 10.3% of the national tax, inhabitants tax, and enterprise tax creates effective tax rates typically ranging from 30% to 35% depending on company size and structure. The per capita levy represents a minimum annual expense that persists regardless of business performance — particularly significant for new market entrants who often operate at a loss during their initial years.

Multi-national companies must reconcile Japan's local tax structure with their global tax planning strategies. Transfer pricing decisions that optimize global tax positions may create unintended consequences for Japanese local taxes. Currency fluctuations also affect the real burden of fixed per capita levies for foreign parent companies reporting in other currencies. Repatriation planning must account for the full tax burden including local taxes, as high local tax burdens reduce distributable profits available for dividend payments.

2026 Defense Surtax & Upcoming Changes

Starting with fiscal years beginning April 1, 2026, corporations will face an additional 4% surtax on their national corporate income tax liability. This defense enhancement tax responds to Japan's increased security spending needs. Because inhabitants tax is computed as a percentage of corporate income tax, the 4% increase in the base tax translates into additional inhabitants tax liability as well, compounding the overall impact.

Global minimum tax provisions introduce entirely new obligations for multinational enterprises. The qualified domestic minimum top-up tax and undertaxed profits rule implement Japan's commitments under the OECD's Pillar Two framework. Companies with global revenue exceeding 750 million euros must calculate and pay these additional taxes, which interact with existing local tax obligations in complex ways.

Professional Assistance

The complexity of Japan's local tax system makes professional assistance valuable for most foreign companies. Japanese certified public accountants and tax accountants provide specialized expertise, and firms range from large international practices offering English-language service to specialized local firms focusing solely on Japanese taxation. Government resources include the NTA website with English-language sections, and the JETRO investor guides that provide high-level tax overviews for foreign companies. Be sure to also review your post-incorporation filing requirements to stay compliant from day one.

| Tax Component | Applicable To | Basis of Calculation | Approximate Rate / Amount |

|---|---|---|---|

| Enterprise Tax (Income-based, SME) | Paid-in capital ≤ 100M yen | Taxable income (progressive brackets) | 3.5% – 6.7% |

| Enterprise Tax (Income-based, Large Corp.) | Paid-in capital > 100M yen | Taxable income | 1.0% – 1.75% |

| Enterprise Tax (Value-added) | Paid-in capital > 100M yen | Compensation + net interest + net rent ± income | 0.37% – 0.7% |

| Enterprise Tax (Capital-based) | Paid-in capital > 100M yen | Paid-in capital + capital surplus | 0.175% – 0.35% |

| Special Local Corporate Tax | All corporations | % of standard enterprise tax (income portion) | 37% of income-based enterprise tax |

| Inhabitants Tax (Corporate tax-rate portion) | All corporations | % of national corporate income tax liability | ~10.4% (prefectural) + ~6.0% (municipal) |

| Inhabitants Tax (Per capita levy) | All corporations | Fixed amount based on capital & employee count | ¥70,000 – ¥3,800,000 per year |

| Defense Surtax (from FY2026) | All corporations | % of national corporate income tax | 4% of corporate tax liability |

Need help navigating Japan's local enterprise and inhabitants taxes?

AQ Partners handles local tax filing, multi-prefecture apportionment, and size-based calculations for foreign companies across Japan.

Book a Free ConsultationFrequently Asked Questions

What is the difference between enterprise tax and inhabitants tax?

Enterprise tax is levied by prefectures on business income and, for large corporations, on value-added and capital bases. Inhabitants tax is imposed by both prefectures and municipalities and consists of a corporate tax rate portion calculated as a percentage of national corporate income tax plus a per capita levy based on capital and employees.

Do I have to pay local taxes if my company operates at a loss?

Yes. Even when a company has no taxable income, it must still pay the per capita levy portion of inhabitants tax. This fixed annual amount ranges from approximately 70,000 yen for small companies to over 3 million yen for large corporations, depending on paid-in capital and employee count.

How is size-based enterprise tax calculated?

Size-based enterprise tax applies to corporations with paid-in capital exceeding 100 million yen and includes three components: income-based tax at reduced rates, value-added tax calculated on employee compensation plus net interest and rent, and capital-based tax calculated on paid-in capital and capital surplus.

When are local tax returns due?

Local tax returns are filed together with the national corporate income tax return, typically due two months after the fiscal year-end. Companies may request a one-month extension, though estimated taxes must still be paid by the original deadline.

How do I pay taxes if I operate in multiple prefectures?

Companies must file separate returns and make separate tax payments to each prefecture and municipality where they maintain an office. Income is apportioned across jurisdictions based on factors such as employee count and office space in each location.

Is enterprise tax deductible?

Yes, enterprise tax is deductible for corporate income tax purposes, but with a timing difference. Enterprise tax paid in one fiscal year becomes deductible when calculating taxable income for the following fiscal year, creating a one-year delay in the tax benefit.

What happens if I miss the filing deadline?

Late filing triggers penalties and interest charges. Japan's tax authorities enforce strict deadlines, and companies face both a penalty for late filing and interest charges on unpaid tax amounts. The interest rate can range from 2.4% to 8.7% annually depending on circumstances.

Do foreign branch offices pay the same local taxes as Japanese companies?

Yes. Foreign companies operating through branch offices in Japan face the same enterprise tax and inhabitants tax obligations as domestic corporations. They must file returns and pay taxes based on their income attributed to Japanese operations.

How will the 2026 defense surtax affect my local tax burden?

The 4% defense surtax on corporate income tax, effective for fiscal years beginning April 1, 2026, will increase both your national tax and your inhabitants tax since inhabitants tax is calculated as a percentage of corporate income tax. This creates a compounding effect on your effective tax rate.

Should I keep my paid-in capital below 100 million yen to avoid size-based taxation?

While maintaining capital below 100 million yen avoids size-based enterprise taxation, recent reforms have expanded this system to include wholly-owned subsidiaries of large corporations and companies with combined capital and capital surplus exceeding certain thresholds. Capital structure decisions should balance tax considerations with business needs for credibility and operational flexibility.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.