Corporate Income Tax in Japan: Rates, Calculation & Filing

Key Takeaways

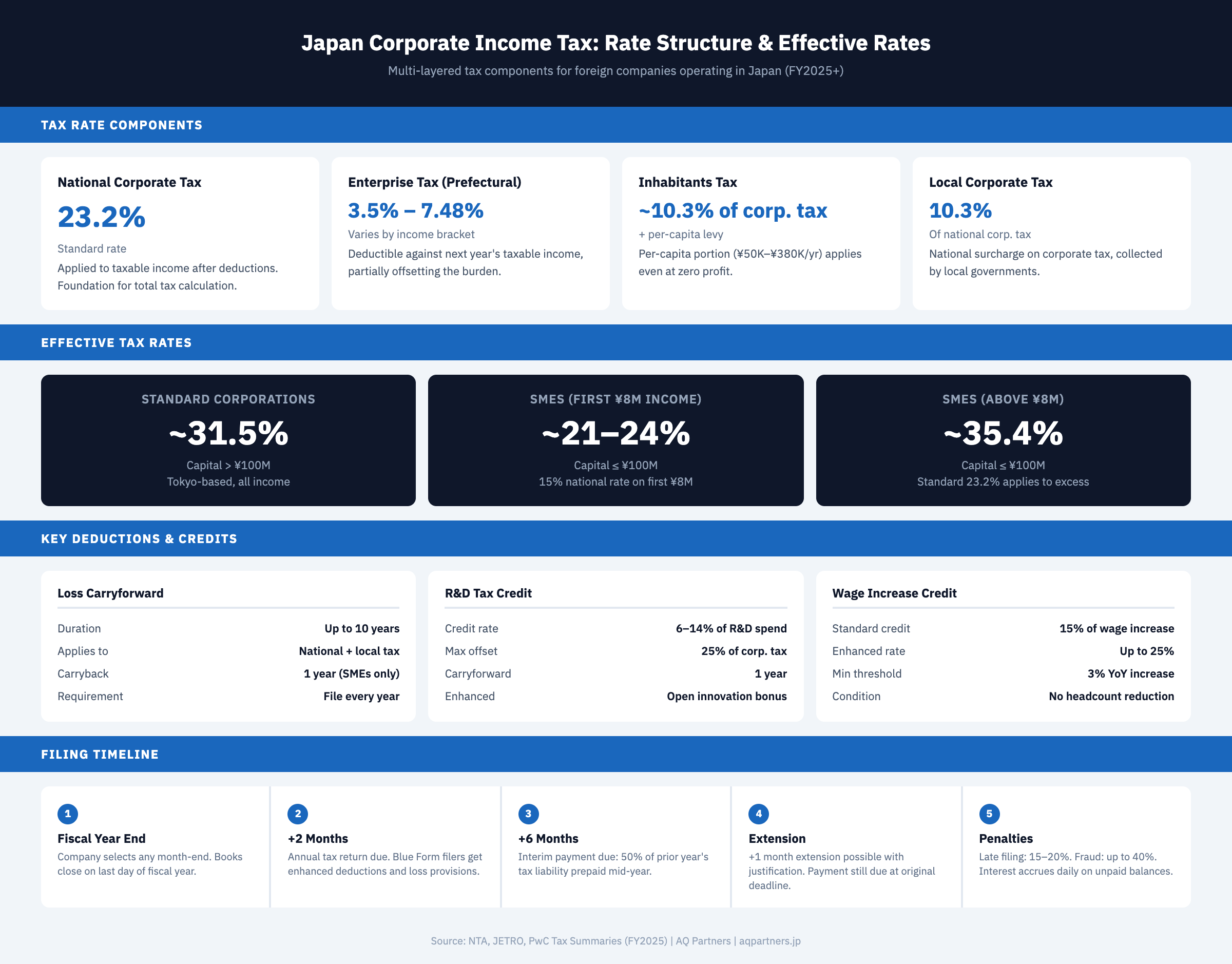

- Japan's effective corporate tax rate is approximately 29–31% for most companies — combining national corporate tax (23.2%), prefectural enterprise tax (3.5–7.48%), inhabitants tax, and local corporate tax. SMEs with paid-in capital of ¥100 million or less pay a reduced 15% national rate on the first ¥8 million of taxable income.

- Taxable income starts from J-GAAP or IFRS accounting profit, then requires numerous adjustments — entertainment expense limits, prescribed depreciation schedules, and transfer pricing rules create significant differences between book and taxable income that require professional guidance.

- Loss carryforward of up to 10 years shelters future profits — critical for startups and companies investing heavily in Japan market development. Loss carryback (1 year) is available for SMEs but invites enhanced NTA scrutiny.

- R&D tax credits of 6–14% and wage increase credits of 15–25% can substantially reduce effective rates — companies conducting R&D in Japan or expanding headcount should integrate these credits into tax planning from the outset.

- Tax returns are due within 2 months of fiscal year-end — Blue Form filing status provides enhanced deductions but requires advance application. Late filing penalties reach 15–20%, with fraud penalties up to 40%.

Understanding Japan's Corporate Income Tax System

Corporate income tax in Japan is a multi-layered obligation comprising national corporate tax, prefectural enterprise tax, inhabitants tax, and local corporate tax. For foreign companies establishing operations in Japan, the combined effective rate of approximately 29–31% places Japan in the middle range among OECD economies — neither a tax haven nor an outlier burden.

Unlike many Western tax systems with a single flat rate, Japan's corporate taxation involves a nuanced calculation that accounts for company size, profitability thresholds, and local jurisdiction. The effective tax rate varies based on entity structure, office location, and how well the company leverages available incentives. According to JETRO's 2025 business setup guide, SMEs with capital of ¥100 million or less pay an effective rate of approximately 21–24% on the first ¥8 million of taxable income — a significant advantage for smaller foreign subsidiaries.

This guide covers the standard and preferential rates, taxable income calculation methods, key deductions and credits available to foreign companies, filing requirements and deadlines, and strategic tax planning considerations.

Corporate Income Tax Rates in Japan

Japan's corporate income tax consists of four primary components: national corporate tax, prefectural enterprise tax, inhabitants tax, and local corporate tax. Each component applies different rates and bases, combining into an effective rate that varies by company size and location.

| Tax Component | Rate / Range | Applies To | Key Notes |

|---|---|---|---|

| National Corporate Tax (Standard) | 23.2% | All corporations | Applied to taxable income after deductions |

| National Corporate Tax (SME Preferential) | 15% | SMEs (capital ≤ ¥100M) | First ¥8M of taxable income only; excess at 23.2% |

| Local Corporate Tax | 10.3% of national tax | All corporations | National surcharge collected by local governments |

| Enterprise Tax (Income-based, Tokyo) | 3.75% – 7.48% | All corporations by prefecture | Deductible against following year's taxable income |

| Enterprise Tax (Size-based) | Added value + capital bases | Capital > ¥100M only | Pro forma taxation using multiple tax bases |

| Inhabitants Tax (Income portion) | ~10.3% of national tax | All corporations | Prefectural + municipal combined |

| Inhabitants Tax (Per-capita levy) | ¥50,000 – ¥380,000/year | All corporations | Applies even at zero profit based on capital and headcount |

| Combined Effective Rate (Standard, Tokyo) | ~31.5% | Capital > ¥100M | Varies by prefecture; Tokyo at upper end |

| Combined Effective Rate (SME, first ¥8M) | ~21–24% | Capital ≤ ¥100M | Significant savings on initial income bracket |

| Combined Effective Rate (SME, above ¥8M) | ~35.4% | Capital ≤ ¥100M | Standard 23.2% national rate on excess income |

The standard national corporate tax rate is 23.2%. According to PwC's 2026 Worldwide Tax Summaries, the combined effective rate for standard corporations (capital exceeding ¥100 million) in Tokyo is approximately 31.52%, while SMEs face a blended rate depending on income levels. The national rate has decreased from above 30% over the past decade as Japan works to enhance international competitiveness.

SMEs with paid-in capital of ¥100 million or less qualify for a 15% national rate on the first ¥8 million of annual taxable income. A company earning ¥10 million in taxable income saves approximately ¥656,000 annually compared to the standard rate. Companies where more than 50% of shares are held by a corporation with capital exceeding ¥100 million do not qualify, preventing large corporations from subdividing operations for tax benefits.

Local Taxes: Enterprise Tax and Inhabitants Tax

Enterprise tax and inhabitants tax add 8–12 percentage points on top of the national rate, making them significant components of total corporate tax liability in Japan.

Enterprise tax (jigyozei) is levied by prefectural governments at rates ranging from 3.75% to 7.48% in Tokyo, depending on income brackets. According to JETRO, the rates apply in three tiers: 3.75% on the first ¥4 million, 5.665% on the next ¥4 million, and 7.48% on income exceeding ¥8 million. Enterprise tax paid during the fiscal year is deductible when calculating taxable income for the following year, creating a timing benefit. Companies with capital exceeding ¥100 million face additional "pro forma taxation" using value-added and capital bases alongside the income base.

Inhabitants tax (juuminzei) consists of prefectural and municipal components totaling approximately 10.3% of national corporate tax liability, plus a fixed per-capita levy. The per-capita portion ranges from ¥50,000 to ¥380,000 annually based on paid-in capital and employee count. Even companies with zero profits must pay this per-capita levy — it functions as a minimum tax for maintaining a legal presence in Japan.

Calculating Taxable Income

Taxable income in Japan starts from accounting profit under J-GAAP (or IFRS for eligible companies), then requires numerous adjustments prescribed by tax law before arriving at the figure on which corporate tax is calculated.

Most foreign subsidiaries in Japan maintain books under J-GAAP, the domestic accounting framework. Companies meeting certain criteria — primarily large publicly traded corporations — may elect IFRS, reducing consolidation complexity with foreign parents. The choice between frameworks affects tax adjustments, audit requirements, and the expertise available from local service providers. The National Tax Agency primarily references J-GAAP treatment in its guidance.

Common Tax Adjustments

Japanese tax law requires adding back certain accounting expenses that are not deductible for tax purposes. Key adjustment areas include:

- Entertainment expenses: Tax law limits deductions to 50% of expenditures up to ¥8 million annually for most corporations. Amounts exceeding this threshold are added back to taxable income.

- Depreciation: Japan prescribes specific depreciation methods and useful life tables for each asset category, often differing from book depreciation. Companies must maintain parallel depreciation schedules and track timing differences.

- Provisions for doubtful accounts: Limited to amounts calculated using prescribed formulas rather than management estimates.

- Related-party transactions: Transfer pricing adjustments required where intra-group pricing does not reflect arm's length conditions.

- Donations: Deductibility subject to detailed rules and limits based on capital and income levels.

Branch vs. Subsidiary Tax Calculations

Branches must maintain separate books and calculate taxable income as if they were independent corporations, allocating expenses between the branch and foreign head office under arm's length principles. The NTA scrutinizes branch profit allocations closely, as improper allocation can artificially reduce Japanese taxable income. Transfer pricing rules apply to intra-company transactions, making many international companies prefer incorporating subsidiaries for clearer legal separation and simpler tax calculations.

Key Deductions and Tax Credits

Japan provides several tax credits and deductions that can reduce the effective rate by 5–10 percentage points for qualifying companies, particularly those investing in R&D, expanding headcount, or carrying forward startup losses.

| Deduction / Credit | Benefit | Eligibility | Duration | Key Condition |

|---|---|---|---|---|

| Loss Carryforward | Offset future taxable income | All corporations | Up to 10 years | Must file returns every year including loss years |

| Loss Carryback | Refund of prior-year tax paid | SMEs only (capital ≤ ¥100M) | 1 year back | Invites enhanced NTA audit scrutiny |

| R&D Tax Credit (Standard) | 6–14% of qualifying R&D spend | All corporations | Unused credits carry 1 year | Max offset: 25% of corporate tax liability |

| R&D Tax Credit (Open Innovation) | Enhanced rate above standard | Collaboration with universities/startups | Same as standard | Requires advance documentation |

| Wage Increase Credit (Standard) | 15% of salary increases above threshold | All corporations | Annual | Min 3% YoY payroll increase required |

| Wage Increase Credit (Enhanced) | Up to 25% of salary increases | Companies with larger increases | Annual | No headcount reduction allowed |

| Blue Form Filing Benefits | Enhanced loss provisions, special depreciation | Blue Form-approved corporations | Ongoing | Advance application + detailed bookkeeping |

| Regional Incentives | Reduced enterprise tax, accelerated depreciation | Companies in designated zones | Varies | Coordination with local government required |

Loss carryforward is critical for foreign companies investing heavily during Japan market entry. Operating losses can shelter profits for up to 10 years once operations become profitable. Companies must file tax returns for every year — including loss years — to preserve carryforward eligibility. Gaps in filing history forfeit losses for those periods. Ownership changes exceeding 50% may limit or eliminate accumulated losses.

R&D tax credits allow companies to claim 6–14% of qualifying R&D expenses, with the exact percentage depending on R&D intensity relative to total income. The credit offsets up to 25% of corporate tax liability per year. Qualifying activities include development of new products and services, improvement of existing offerings, and basic research conducted in Japan. Foreign companies in technology, pharmaceuticals, and manufacturing should systematically track R&D activities to capture all eligible expenses.

Wage increase credits of 15–25% reward companies that grow employee compensation above prior-year levels. The standard 15% credit applies when total payroll increases by at least 3% year-over-year. Enhanced credits of up to 25% apply for larger increases. Companies cannot reduce headcount while claiming these credits.

Filing Requirements and Deadlines

Corporate tax returns must be filed with the National Tax Agency within two months after fiscal year-end. Companies can select any month-end as their fiscal year-end, providing flexibility to align with global reporting cycles.

Blue Form Filing

All companies must file annual returns regardless of profit or loss. Companies maintaining proper books and records can elect "Blue Form" filing status, which provides preferential tax treatments including enhanced loss carryforward, special depreciation allowances, and certain credits unavailable to standard "White Form" filers. Blue Form requires advance application and ongoing compliance with detailed bookkeeping requirements — companies should establish compliant systems from the start, as retroactive qualification is not possible.

Interim Tax Payments

Companies with significant tax liability must make interim payments six months into their fiscal year, equal to half of the prior year's tax. Companies anticipating substantially lower current-year profits can apply to reduce interim payments based on actual half-year results. Growing companies should project full-year liability early and set aside monthly reserves to avoid cash crunches at payment deadlines.

Extensions and Penalties

One-month filing extensions are available with reasonable justification (complex transactions, personnel changes, parent company coordination), but must be requested before the original deadline. Extensions do not extend the payment deadline — estimated tax must still be paid on time. Late filing penalties reach 15–20% of unpaid tax for negligence and up to 40% for fraud, with daily interest accruing on unpaid balances. For foreign companies, tax compliance certificates are often required for visa renewals and government approvals.

Special Considerations for Foreign Companies

Foreign companies face additional complexity beyond standard corporate tax rules, including permanent establishment risk, transfer pricing documentation, and withholding tax on cross-border payments.

Permanent Establishment Risk

Foreign companies conducting business in Japan without a formal subsidiary or branch may still create a "permanent establishment" (PE), triggering tax obligations on income attributable to that PE. Activities that create PE exposure include maintaining a fixed place of business, employing dependent agents who regularly conclude contracts, or conducting construction/service projects exceeding specified duration thresholds. Japan's tax treaties with over 70 countries often raise PE thresholds, allowing certain preparatory activities without triggering PE status — but treaty benefits require proper documentation and advance claims.

Transfer Pricing Documentation

Transactions between Japanese subsidiaries and foreign affiliates must reflect arm's length conditions. Japan requires contemporaneous transfer pricing documentation — prepared before the tax return filing deadline — that includes functional analysis, comparability analysis, and economic analysis supporting the pricing methodology. The NTA actively audits transfer pricing, with penalties reaching 40% of additional tax assessed. Companies should invest in proper transfer pricing studies from the outset and update them as business functions evolve.

Withholding Tax on Cross-Border Payments

Japanese companies making payments to foreign parents or affiliates face 20% withholding tax on dividends, interest, and royalties. Tax treaties often reduce these rates significantly — to 5–10% for dividends from substantial shareholders, and frequently eliminate withholding on interest. Claiming treaty benefits requires certificates of residence from the recipient's home country tax authority, filed before making payments. Foreign companies should consider withholding tax alongside corporate income tax when structuring entity and financing arrangements.

Strategic Tax Planning

Effective corporate tax planning in Japan extends beyond compliance to active management of entity structure, timing strategies, and available incentives that can reduce the effective rate by several percentage points.

The choice between operating as a branch versus incorporated subsidiary carries significant tax implications. Branches allow losses to flow through to the foreign parent and avoid dividend withholding on profit repatriation, potentially advantageous during startup phases. Subsidiaries provide clearer legal separation and simplified tax calculations but introduce dividend withholding. Thin capitalization rules limit interest deductibility when debt-to-equity ratios exceed 3:1 for related-party debt.

Fourth-quarter tax planning reviews are standard practice for well-managed Japanese operations: project full-year taxable income, identify unclaimed credits and deductions, evaluate timing opportunities for major expenses, and confirm documentation is prepared. Regional incentives in special economic zones — including reduced enterprise tax, accelerated depreciation, and establishment grants — can benefit companies willing to locate beyond major metropolitan centers.

Frequently Asked Questions

What is the effective corporate tax rate in Japan?

The combined effective corporate tax rate in Japan is approximately 29–31% for most companies, combining national corporate tax (23.2%), enterprise tax (3.5–7.48%), inhabitants tax (~10.3% of national tax), and local corporate tax (10.3%). SMEs with paid-in capital of ¥100 million or less pay a reduced effective rate of approximately 21–24% on the first ¥8 million of taxable income. The exact rate varies by prefecture and municipality, with Tokyo-based companies generally at the higher end.

How is taxable income calculated in Japan?

Taxable income begins with accounting profit under J-GAAP (or IFRS for eligible companies), then undergoes numerous adjustments required by Japanese tax law. Common adjustments include adding back entertainment expenses exceeding deductibility limits, reconciling book depreciation to prescribed tax depreciation schedules, adjusting provisions for doubtful accounts to prescribed formulas, and applying transfer pricing rules to related-party transactions. The gap between book income and taxable income can be substantial.

What tax incentives are available for foreign companies?

Foreign companies can access loss carryforward (up to 10 years), R&D tax credits (6–14% of qualifying spend), wage increase credits (15–25% of payroll growth), and Blue Form filing benefits. Regional incentives in designated zones offer reduced enterprise tax rates and accelerated depreciation. SMEs with capital of ¥100 million or less qualify for a preferential 15% national rate on the first ¥8 million of income, and loss carryback claims can provide immediate cash flow relief.

When are corporate tax returns due?

Annual corporate tax returns must be filed within two months after the company's fiscal year-end. Companies can select any month-end as their fiscal year-end. Interim payments of 50% of prior-year liability are due six months into the fiscal year. One-month filing extensions are available with justification, but the payment deadline is not extended. Late filing penalties range from 15–20% for negligence to 40% for fraud, with daily interest on unpaid balances.

Do foreign companies need transfer pricing documentation?

Yes. All transactions between Japanese entities and foreign affiliates must comply with arm's length pricing requirements. Japan mandates contemporaneous transfer pricing documentation prepared before the tax return filing deadline, including functional analysis, comparability studies, and economic analysis. The National Tax Agency actively audits transfer pricing and can impose penalties of up to 40% of additional tax assessed. Advance pricing agreements are available but require significant time and resources to negotiate.

For guidance on navigating Japan's corporate tax system, including entity structuring, tax filing compliance, and local tax obligations, contact AQ Partners for a consultation.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.