Mastering Chart of Accounts Management in Japan

Key Takeaways

- A Japan-compliant chart of accounts must align with J-GAAP statutory captions — every account maps to a mandated balance sheet or P&L line item, ensuring regulatory filings, audits, and group consolidation proceed without reclassification delays.

- Bilingual account naming in English and Japanese is essential, not optional — dual-language fields using kanji, katakana, and ASCII prevent translation errors and allow both local staff and global headquarters to work from a single, consistent ledger.

- Consumption tax requires separate subaccounts for each JCT rate — the Qualified Invoice System (effective October 2023) demands that input tax credits be tracked by invoice qualification status, making rate-specific COA segregation a compliance requirement.

- Legal reserves and retained earnings need dedicated COA lines under Japanese law — unlike IFRS or US GAAP, Japan mandates specific reserve fund allocations that must be recorded and reported separately in statutory filings each fiscal year.

- Industry-specific COA templates accelerate market entry — manufacturers, trading companies, and SaaS providers each face distinct J-GAAP requirements for cost accounting, inventory flow, and revenue recognition that generic COA structures cannot address.

Foundations of Chart of Accounts Management in Japan

A well-structured chart of accounts is the backbone of compliant financial operations in Japan, connecting every transaction to statutory reporting, tax filings, and management analysis.

To succeed in Japan, businesses must develop a COA that combines statutory precision with operational flexibility. Unlike many Western systems, Japanese regulations require a COA that is not only compliant with J-GAAP, but also supports bilingual reporting and flexible segmentation by business unit or operational purpose. Overlooking these nuances can lead to compliance failures, time-consuming corrections, and friction between global and local teams.

For those in the process of registering and structuring a new entity in Japan, paying attention to the statutory compliance requirements for accounting setup is crucial right at the outset.

What a Japan-ready COA must accomplish

A Japan-ready COA must achieve several essential goals to ensure both compliance and operational efficiency:

- The COA must fully support statutory reporting under J-GAAP, allowing accurate financial statements to be submitted promptly to Japanese regulators, such as the Financial Services Agency.

- It should be structured for robust tax compliance, ensuring all required local taxes and disclosures are directly traceable through the accounts.

- Bilingual operations are critical; account titles, descriptions, and codes must function clearly in both Japanese and English, supporting the needs of local staff and global teams alike.

- Every account should map precisely to mandatory financial report line items, supporting both group and subsidiary reporting workflows.

- This structure reduces manual effort, minimizes errors, and enables business leaders to focus resources on growth rather than administrative corrections.

Data granularity and segments for reporting

Data granularity in Japan is mandatory—it is both a regulatory standard and a foundation of effective internal control. Japanese authorities and auditors require financial data that is traceable not only by major ledgers but also by specific purposes, such as projects, products, or departments, and across multiple legal entities. This level of detail allows organizations to produce both consolidated and stand-alone reports with precision. According to Deloitte and the Japanese Institute of Certified Public Accountants, a well-segmented COA ensures the transparency and adaptability needed to respond smoothly to new business models or regulatory changes.

Metrics to monitor COA health

Once your COA is in place, ongoing monitoring is crucial, especially as your business grows and operations become more complex. In Japan, several key metrics help track and improve COA health: the total number of active accounts (to prevent unnecessary proliferation), the rate of account reuse (which enhances efficiency and clarity), and the frequency of structural changes (which may signal design or compliance issues). Regular audits verify that accounts align with J-GAAP standards and internal control requirements, as highlighted by KPMG and Deloitte, reducing errors and compliance risks.

This strong foundation is essential for incorporating Japan's complex statutory requirements into your COA—where mistakes can be costly, and careful design delivers long-term value.

J-GAAP Alignment: Statutory Reporting and COA Mapping

Proper J-GAAP alignment ensures every account in your chart directly corresponds to a mandated statutory caption, preventing audit delays and restatement risks during financial statement preparation.

Compliance with J-GAAP is critical for businesses operating in Japan. Statutory alignment requires a COA that matches the captions and disclosures mandated by Japanese authorities. Neglecting J-GAAP alignment can result in regulatory penalties, delayed financial statement closure, and conflicts between group and local reporting—challenges best prevented through careful COA planning. For a deeper look at the differences between local and international standards, see our guide on IFRS vs J-GAAP compliance in Japan.

Required balance sheet and P/L captions

Japanese GAAP imposes strict requirements for balance sheet and profit and loss (P&L) captions:

- Statutory reporting requires a fixed, comprehensive list of captions for both the balance sheet and P&L statement, which must be observed in all COA structures.

- Key items including cash, receivables, payables, inventory, and granular revenue and expense accounts each need specific COA lines to enable accurate aggregation.

- Regulatory authorities define these captions rigorously, so companies must ensure their COA covers all local disclosure rules—regardless of group or global practices.

- Adhering to these requirements enables smoother statutory audits and helps businesses avoid costly oversights, misclassifications, or reporting deficiencies.

Reserves, allowances, and statutory disclosures

Japanese accounting requires particularly careful treatment of reserves and allowances, surpassing expectations in many global teams. Businesses must independently classify and monitor provisions such as bad debt reserves, employee bonus reserves, and retirement benefit obligations—with dedicated COA lines for each. These entries are essential for both internal control and annual statutory reports, which demand transparency regarding the purpose, amount, and accounting basis of every reserve. Guidance from Grant Thornton and the Accounting Standards Board of Japan shows that correct reserve classification not only ensures compliance but also strengthens audit preparedness, prevents year-end surprises, and reflects strong management practices.

Mapping accounts to statutory report lines

A thoroughly mapped COA is vital for efficient financial statement preparation in Japan. Each account must correspond directly to a statutory reporting line, as defined by J-GAAP, ensuring that statutory, tax, and management reporting all stem from a single, consistently maintained system. Advanced ERP systems support this through mapping tables and configuration tools linking every COA account to the necessary report captions. According to PwC and EY, documenting the mapping logic, conducting regular regulatory updates, and maintaining clear change procedures for accounts, captions, or rules are essential practices. These steps streamline compliance, facilitate consolidated reporting, and reduce the risk of last-minute restatements or regulatory issues.

Legal reserves and retained earnings treatment

Japanese compliance requires strict rules for legal reserves and retained earnings within the COA. Companies must allocate specific portions of profits to legal reserves, such as a statutory reserve fund, which must be clearly recorded and reported separately in statutory filings. Account handling for legal reserves in Japan differs from IFRS or US GAAP standards. The Japanese Institute of Certified Public Accountants and the Accounting Standards Board of Japan emphasize the need for dedicated COA accounts for legal reserves and diligent tracking of retained earnings distributions each year. Failing to segregate these items as required can invite auditor scrutiny or compromise statutory filings. International teams should be vigilant, as these local requirements may conflict with group consolidation practices.

Japan Consumption Tax Design in the COA

JCT compliance depends on rate-specific subaccounts and qualified invoice tracking built into the COA structure, enabling accurate monthly reconciliation and audit-ready tax filings.

Japan's consumption tax (JCT) framework is highly regulated, requiring businesses to design their COA to allow transparent tracking, reconciliation, and full compliance. Below are strategies and processes for managing JCT from both statutory and practical perspectives.

Control accounts and subaccounts by rate

Managing multiple JCT rates necessitates careful setup of control accounts and subaccounts:

- Companies must create separate control accounts and associated subaccounts for each JCT rate—standard and reduced—ensuring accurate tracking of tax liabilities.

- Rate segmentation is especially important for industries like retail and hospitality, where large volumes of reduced-rate transactions and detailed breakdowns are common.

- Specialized account structures help reduce the risk of overpayments and misstatements, simplify audit preparation, and streamline tax filing and compliance processes.

- Maintaining rate-specific tax accounts allows quick reconciliation of taxable amounts and prompt responses to audit inquiries or regulatory requests.

Qualified Invoice System and input credits

The Qualified Invoice System, introduced in October 2023, significantly changed how companies can claim input JCT credits. Now, only purchases with qualified invoices, including registered supplier numbers, qualify for tax credits. The Japan National Tax Agency stresses the importance of COA subaccounts or tracking mechanisms that clearly separate input tax by qualification status, ensuring there are no erroneous claims. Distinguishing input taxes from qualified versus unqualified invoices streamlines monthly checks and maintains the validity of tax credits. It is crucial to keep vendor records updated and to integrate invoice qualification checks into your COA configuration.

Month-end JCT reconciliation and checklist

Month-end reconciliation is a key internal control for JCT compliance. Companies must verify that all JCT entries in the COA match actual sales and purchases, and that only qualified invoices are counted for input tax credits. PwC recommends a detailed checklist: aggregate subaccount balances by rate, confirm credits against supporting documentation, and cross-check COA entries with external tax filings for the period. Robust reconciliation processes lower compliance risks and reduce the need for late corrections. Failure to reconcile properly can cause settlement delays, penalties, or even prompt tax investigations. Successful companies formalize JCT reconciliation as part of monthly closing routines and conduct routine audits to maintain process integrity.

Sample journal flows for JCT postings

Accurate journal entries are essential to COA integrity for consumption tax. According to Deloitte and the National Tax Agency, on a sale, output tax must be credited to the relevant JCT output account by rate, while input tax paid on purchases is debited to JCT input accounts. At month-end, qualifying credits are transferred to the tax payable account, and reversals are made if documentation fails to meet qualified invoice standards. For instance, if a valid qualified invoice is missing from a recorded purchase, the input tax entry must be reversed before filing. These controls ensure both gross and net JCT figures are accurate for statutory filing and daily cash flow management, reducing risk and ensuring transparency during tax audits.

Scalable Bilingual and Operational COA Design for Japan

Building a bilingual, scalable COA from the start prevents costly restructuring later and ensures both Japanese regulators and global headquarters can read the same financial data without translation friction.

As businesses grow in Japan—especially those with multinational structures or distributed teams—a COA that is fully bilingual and operationally resilient becomes crucial. Key considerations include language compatibility, code structure, statutory requirements, and industry standards. Teams planning their Japan market entry back office setup should integrate COA design into their operational blueprint from day one.

English/Japanese naming and character rules

To build a bilingual COA in Japan, certain naming and character conventions are important:

- Use both English and Japanese for all account names and descriptions, applying Unicode standards to include kanji, katakana, and ASCII as appropriate.

- Consistent naming conventions ensure that audit documents and management reports can be easily switched between languages, minimizing confusion.

- Dual-field account names in ERP systems support consistency, reduce translation errors, and simplify onboarding for international staff.

- Bilingual operations enable companies to meet statutory requirements and facilitate effective cross-border collaboration.

Code lengths, ranges, reserved Japan blocks

Japanese COA structures typically feature 4- to 6-digit account numbers, with reserved series for statutory purposes and future expansion. Deloitte and PwC recommend assigning specific code blocks for Japan-only requirements such as social insurance, special reserves, or fixed asset categories and depreciation methods, simplifying audits and regulatory updates. This approach is especially useful for companies operating across multiple entities or industries. Reserved code ranges aid detailed tracking, ease system upgrades, and strengthen access controls, supporting compliance and operational flexibility alike.

Employer health, pension, employment insurance

Mandatory employer contributions for health, pension, and employment insurance are central to Japanese labor compliance. The Ministry of Health, Labour and Welfare advises using dedicated COA lines for each category, supporting payroll reconciliation, detailed HR budgeting, and evidence of legal compliance. For teams operating remotely or across borders, clear account structures for social insurance contributions ensure smooth statutory reporting and reduce errors or omissions during payroll cycles. This clarity is especially important during regulatory or labor inspections, which are frequent among foreign-owned businesses in Japan. Companies should also ensure their COA integrates with post-incorporation filing requirements for social insurance registration.

Industry playbooks: manufacturing, trading, SaaS

Designing a COA that is tailored to industry needs is critical for compliant and insightful statutory and management reporting in Japan. Manufacturers need detailed, organized accounts for products, cost accounting, and inventory, meeting both domestic and global standards. Trading companies emphasize inventory flow and gross margin analysis, often with dedicated COA segments for order processing, logistics, and foreign currency activities. SaaS providers encounter unique Japanese demands, requiring accounts for deferred and recurring revenues, contract assets, and subscription billing. EY notes that SaaS COAs must accurately mirror complex revenue recognition patterns while complying with J-GAAP and Japanese consumption tax rules. Using industry-specific COA templates speeds market entry and reduces back-office rework as business models evolve. For companies still evaluating their Japan presence, our guide to opening a corporate bank account in Japan covers the financial infrastructure that connects directly to your COA.

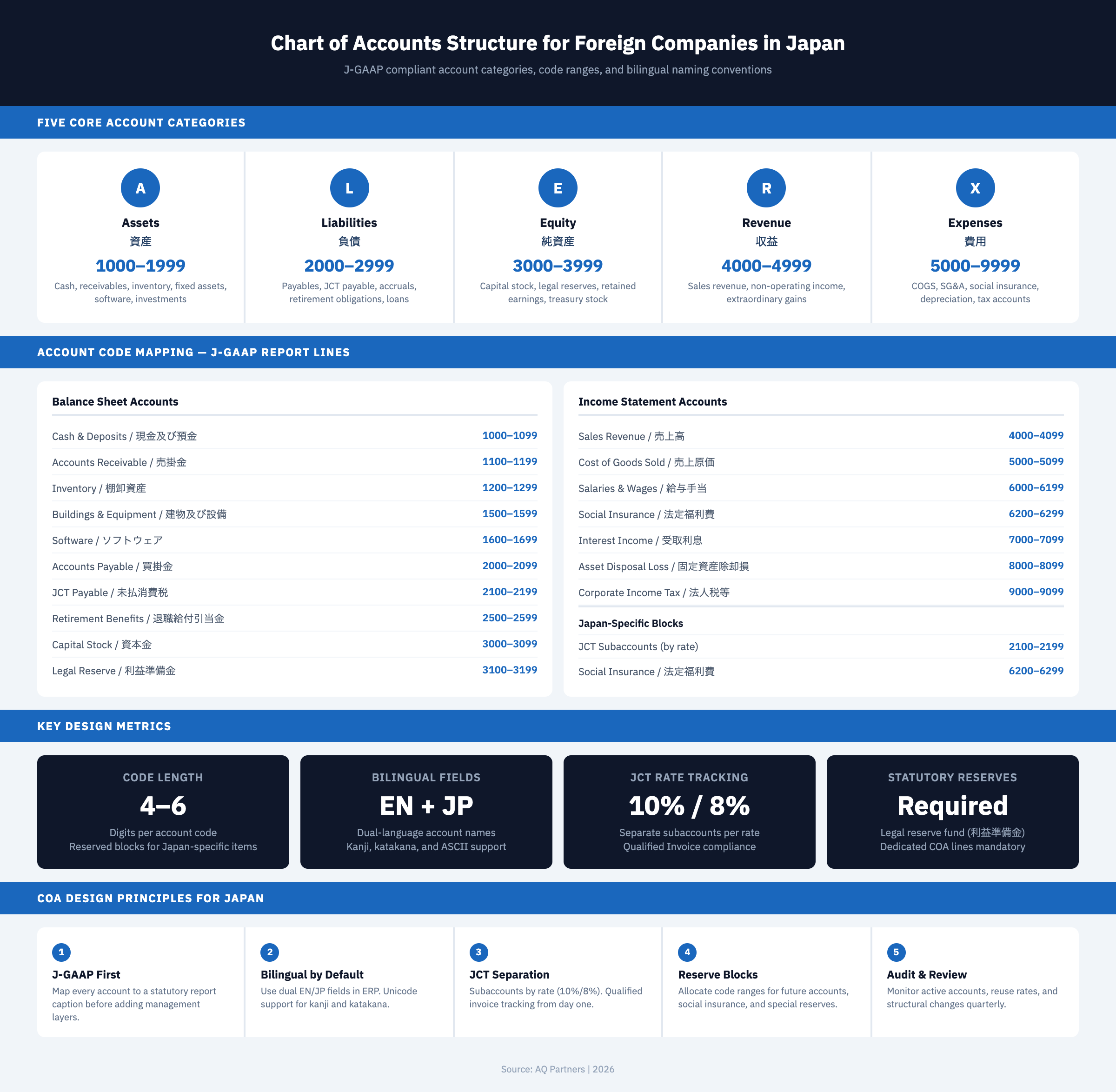

Sample Chart of Accounts Structure for Foreign Companies in Japan

This reference table maps the most common J-GAAP account categories to standardized code ranges, giving foreign companies a practical starting point for building a compliant COA.

The table below provides a representative COA framework that foreign companies commonly adopt when establishing operations in Japan. It maps account categories to typical J-GAAP report lines and includes bilingual naming conventions, offering a practical starting point for corporate income tax reporting in Japan and statutory compliance.

| Account Code Range | Category | Typical Account Names (EN / JP) | J-GAAP Report Line |

|---|---|---|---|

| 1000–1099 | Current Assets | Cash and Deposits / 現金及び預金 | Balance Sheet — Current Assets |

| 1100–1199 | Current Assets | Accounts Receivable / 売掛金 | Balance Sheet — Current Assets |

| 1200–1299 | Current Assets | Inventory / 棚卸資産 | Balance Sheet — Current Assets |

| 1500–1599 | Fixed Assets | Buildings & Equipment / 建物及び設備 | Balance Sheet — Fixed Assets (Tangible) |

| 1600–1699 | Fixed Assets | Software / ソフトウェア | Balance Sheet — Fixed Assets (Intangible) |

| 2000–2099 | Current Liabilities | Accounts Payable / 買掛金 | Balance Sheet — Current Liabilities |

| 2100–2199 | Current Liabilities | Consumption Tax Payable / 未払消費税 | Balance Sheet — Current Liabilities |

| 2200–2299 | Current Liabilities | Accrued Expenses / 未払費用 | Balance Sheet — Current Liabilities |

| 2500–2599 | Long-term Liabilities | Retirement Benefit Obligations / 退職給付引当金 | Balance Sheet — Long-term Liabilities |

| 3000–3099 | Shareholders' Equity | Capital Stock / 資本金 | Balance Sheet — Net Assets |

| 3100–3199 | Shareholders' Equity | Legal Reserve / 利益準備金 | Balance Sheet — Net Assets |

| 4000–4099 | Revenue | Sales Revenue / 売上高 | P&L — Net Sales |

| 5000–5099 | Cost of Sales | Cost of Goods Sold / 売上原価 | P&L — Cost of Sales |

| 6000–6199 | SG&A Expenses | Salaries & Wages / 給与手当 | P&L — Selling, General & Admin |

| 6200–6299 | SG&A Expenses | Social Insurance / 法定福利費 | P&L — Selling, General & Admin |

| 7000–7099 | Non-operating Income | Interest Income / 受取利息 | P&L — Non-operating Income |

| 8000–8099 | Extraordinary Items | Loss on Disposal of Assets / 固定資産除却損 | P&L — Extraordinary Losses |

| 9000–9099 | Tax Accounts | Corporate Income Tax / 法人税等 | P&L — Income Taxes |

Conclusion

Mastering chart of accounts management in Japan requires a disciplined, systematic approach that integrates statutory compliance, tax accuracy, and operational adaptability. By aligning with J-GAAP, enabling seamless group-to-local mapping, and enforcing strong governance, businesses achieve reliable audit readiness and practical management insight. Japan's unique requirements—such as stringent consumption tax tracking and bilingual operations—demand thoughtful COA design, supported by advanced ERP configurations and continuous review. A well-constructed Japanese COA not only fulfills legal duties but also builds a foundation for ongoing growth, cross-border visibility, and strong internal controls, empowering founders and finance teams to focus on their core mission with full confidence in their compliance and reporting systems.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.