Blue Form Tax Return in Japan: Benefits & Requirements

Key Takeaways

- Japan's Blue Form (aoiro shinkoku) tax return unlocks critical tax benefits unavailable to White Form filers — including loss carryforward for up to 10 years, special depreciation allowances of up to 30%, and full deductibility of family employee salaries. Approximately 60% of Japanese corporations file under Blue Form status.

- Advance application is mandatory and deadline-sensitive — new corporations must file within 3 months of incorporation, while existing corporations must submit by the day before the start of the fiscal year they want Blue Form status to apply. Retroactive qualification is not possible.

- Double-entry bookkeeping and 7-year document retention are non-negotiable requirements — Blue Form status demands rigorous accounting standards that exceed White Form's simple record-keeping, but these standards also improve financial governance and investor confidence.

- Revocation carries serious consequences and a mandatory waiting period — consecutive late filings, fraudulent returns, or inadequate record-keeping can trigger Blue Form revocation, after which companies must wait at least 1 year before re-applying and lose accumulated tax benefits in the interim.

- Foreign companies establishing operations in Japan should apply for Blue Form status from day one — the loss carryforward benefit alone can save millions of yen during the typically unprofitable market-entry period, sheltering future profits once the business becomes established.

What Is the Blue Form Tax Return?

The Blue Form tax return (aoiro shinkoku / 青色申告) is an elective filing status available to corporations and sole proprietors in Japan that provides preferential tax treatment in exchange for maintaining detailed accounting records. The system traces back to 1950, when the National Tax Agency introduced it to encourage proper bookkeeping across Japanese businesses.

Unlike many Western tax systems where all filers receive the same treatment, Japan distinguishes between Blue Form and White Form (shiroiro shinkoku / 白色申告) filers. White Form is the default status requiring minimal record-keeping, while Blue Form is an opt-in system that rewards companies maintaining rigorous double-entry bookkeeping with substantial tax advantages. According to NTA guidance, the system has become the standard for serious business operations in Japan.

For foreign companies entering the Japanese market, Blue Form filing is not merely an administrative choice — it is a strategic decision that directly impacts tax liability during the critical early years when operations typically generate losses. Understanding and securing Blue Form status should be among the first priorities when setting up tax compliance in Japan.

Benefits of Blue Form Filing

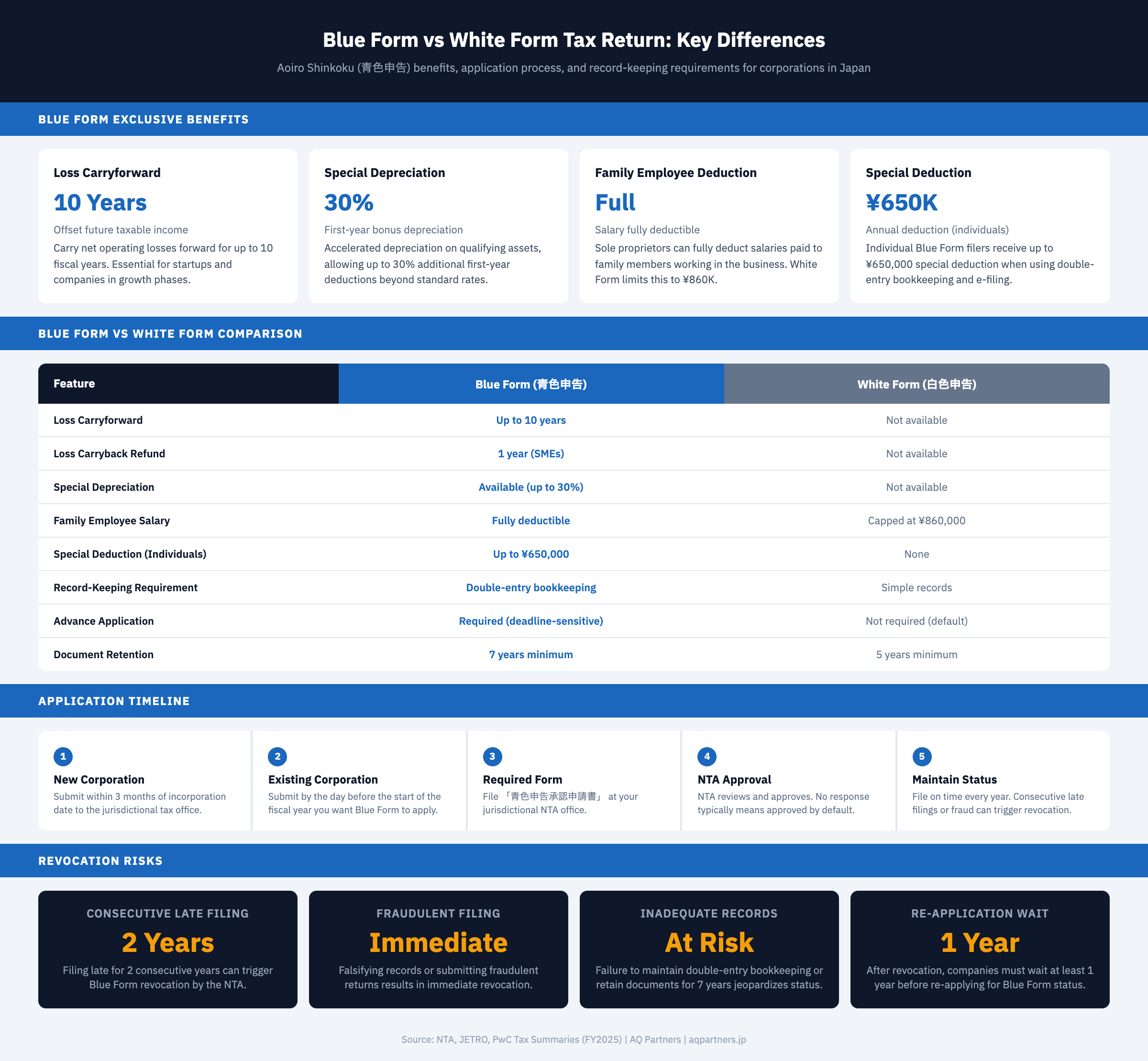

Blue Form filing provides six core tax advantages that collectively can reduce a corporation's effective tax burden by millions of yen over time, particularly during the first several years of operations in Japan.

Loss Carryforward (10 Years)

The most significant benefit for foreign companies is the ability to carry net operating losses forward for up to 10 fiscal years. Under Blue Form status, losses incurred during startup phases or market expansion can offset taxable income once the business becomes profitable. According to PwC's 2026 tax summary for Japan, this carryforward period is among the most generous in Asia-Pacific. White Form filers cannot carry losses forward at all — losses are permanently forfeited in the year they occur.

Loss Carryback Refund

SMEs (paid-in capital of ¥100 million or less) filing under Blue Form can carry losses back one year to claim a refund of previously paid corporate tax. While this invites enhanced NTA audit scrutiny, it provides immediate cash flow relief during downturns. This benefit is exclusively available to Blue Form filers.

Special Depreciation Allowances

Blue Form corporations can claim accelerated depreciation on qualifying assets, including up to 30% additional first-year depreciation for certain equipment and facility investments. This is particularly valuable for manufacturing, technology, and capital-intensive operations where large initial asset investments are required. Standard tax depreciation schedules apply to White Form filers without these enhancements.

Family Employee Salary Deduction

For sole proprietors, Blue Form status allows full deduction of salaries paid to family members working in the business, provided the salaries are pre-registered with the tax office and at reasonable levels. White Form filers face a cap of ¥860,000 per family employee — a restriction that can significantly increase taxable income for family-run businesses.

Special Blue Form Deduction (Individuals)

Individual Blue Form filers using double-entry bookkeeping and e-filing receive an annual special deduction of up to ¥650,000. This deduction reduces taxable income directly and is unavailable to White Form filers. Even those not using e-filing receive ¥550,000.

Enhanced Tax Credit Eligibility

Several tax incentive programs — including certain R&D tax credits, regional investment incentives, and SME support measures — require Blue Form filing status as a precondition. Without Blue Form, companies may be technically eligible for these credits but unable to claim them.

Eligibility and Application Process

Any corporation or sole proprietor conducting business in Japan can apply for Blue Form status, provided they commit to maintaining proper accounting records. There are no industry restrictions, minimum revenue requirements, or capitalization thresholds — the system is open to all entities willing to meet the bookkeeping standards.

Application Deadlines

The application timing is strict and missing the deadline means waiting an entire fiscal year:

| Situation | Application Deadline | Effective From | Form Required | Filing Location | Processing Time |

|---|---|---|---|---|---|

| Newly incorporated corporation | Within 3 months of incorporation | First fiscal year | Blue Form Approval Application (青色申告承認申請書) | Jurisdictional tax office | Typically 1–2 months |

| Existing corporation (first-time application) | Day before start of target fiscal year | Target fiscal year | Blue Form Approval Application | Jurisdictional tax office | Typically 1–2 months |

| New sole proprietor | Within 2 months of business start | First year of business | Blue Form Approval Application | Jurisdictional tax office | Typically 1–2 months |

| Existing sole proprietor | March 15 of target tax year | Target calendar year | Blue Form Approval Application | Jurisdictional tax office | Typically 1–2 months |

| Re-application after revocation | At least 1 year after revocation date | Following fiscal year | Blue Form Approval Application | Jurisdictional tax office | Enhanced review |

| Corporation changing fiscal year-end | Day before start of new fiscal period | New fiscal period | No re-application needed if already approved | N/A | N/A |

Application Process

The application itself is straightforward. File the 青色申告承認申請書 (Blue Form Approval Application) at your jurisdictional tax office. The form requires basic corporate information, fiscal year details, and a declaration of the bookkeeping method to be used. The NTA does not charge a fee for the application. If the NTA does not respond within the processing period, the application is generally considered approved by default.

Record-Keeping Requirements

Blue Form status demands significantly more rigorous accounting than White Form filing. The requirements are not merely bureaucratic — they form the foundation of Japan's tax administration system and are actively enforced through audits.

Double-Entry Bookkeeping

Blue Form corporations must maintain full double-entry bookkeeping, including a general ledger, journal, and subsidiary ledgers. Every transaction must be recorded with both debit and credit entries, and the books must be maintained on an accrual basis. This is consistent with generally accepted accounting principles under J-GAAP and does not present additional burden for companies already following standard corporate accounting practices.

Required Documents and Retention Periods

Blue Form filers must retain the following records for a minimum of 7 years (compared to 5 years for White Form):

- General ledger and journal entries — complete transaction records with supporting documentation

- Balance sheets and income statements — prepared at each fiscal year-end

- Invoices, receipts, and contracts — all source documents supporting recorded transactions

- Bank statements and payment records — reconciled monthly against ledger entries

- Inventory records — physical count documentation and valuation methods

- Fixed asset registers — acquisition costs, depreciation schedules, and disposal records

Electronic Record-Keeping

Japan's Electronic Books Preservation Act (Denshichoubo Hozonhou) allows Blue Form filers to maintain records electronically, provided specific requirements are met including timestamping, search functionality, and system documentation. As of January 2024, electronic preservation of electronically received transaction data (such as email invoices) became mandatory for all businesses, making digital record-keeping systems essential rather than optional.

Blue Form vs White Form Comparison

The decision between Blue Form and White Form filing fundamentally affects a corporation's tax position and long-term financial planning. While White Form offers simplicity, the tax savings from Blue Form almost always outweigh the additional administrative effort.

| Feature | Blue Form (青色申告) | White Form (白色申告) |

|---|---|---|

| Loss carryforward | Up to 10 years | Not available |

| Loss carryback refund | 1 year (SMEs) | Not available |

| Special depreciation allowances | Available (up to 30% bonus) | Not available |

| Family employee salary deduction | Fully deductible (pre-registered) | Capped at ¥860,000 |

| Special income deduction (individuals) | Up to ¥650,000 | None |

| Tax credit eligibility | Full access to all available credits | Limited to basic credits |

| Bookkeeping requirement | Double-entry bookkeeping (accrual basis) | Simple cash-basis records |

| Document retention period | 7 years minimum | 5 years minimum |

| Advance application required | Yes (deadline-sensitive) | No (default status) |

| NTA audit treatment | Presumption of accuracy on filed returns | NTA may estimate income if records insufficient |

The practical impact of White Form's limitations is severe. A company incurring ¥50 million in startup losses over two years under White Form permanently loses those deductions. Under Blue Form, those losses shelter the next ¥50 million in profits — at a combined effective tax rate of approximately 30%, that represents roughly ¥15 million in tax savings. For this reason, virtually every professional advisor recommends Blue Form filing for corporations operating in Japan.

Revocation Risks and How to Avoid Them

Blue Form status, once granted, is not permanent. The NTA can revoke approval under several circumstances, and revocation carries consequences that extend beyond losing tax benefits.

Grounds for Revocation

- Consecutive late filing: Filing tax returns late for two consecutive fiscal years triggers revocation consideration. Even one late filing generates a warning.

- Fraudulent filing: Submitting false information, fabricating records, or deliberately underreporting income results in immediate revocation, plus criminal penalties of up to 40% additional tax.

- Inadequate record-keeping: Failure to maintain double-entry bookkeeping, missing source documents, or inability to produce records during an audit demonstrates non-compliance with Blue Form requirements.

- Failure to comply with NTA orders: If the NTA issues corrective orders regarding bookkeeping practices and the corporation fails to comply, revocation proceedings may follow.

Consequences of Revocation

Revocation is retroactive to the beginning of the fiscal year in which the violation occurred. This means:

- Loss carryforward balances from the revoked year onward may be forfeited

- Special depreciation claimed in that year may be reversed and reassessed

- A mandatory waiting period of at least 1 year applies before re-application

- Re-applications undergo enhanced NTA scrutiny

How to Protect Your Blue Form Status

Maintaining Blue Form status requires consistent discipline rather than heroic effort. Companies should implement these safeguards:

- Establish filing calendars — set internal deadlines at least 2 weeks before NTA deadlines and assign clear responsibility

- Engage qualified tax professionals — a licensed tax accountant (zeirishi) provides both compliance assurance and early warning of potential issues

- Maintain contemporaneous records — record transactions as they occur rather than reconstructing records before filing season

- Conduct internal reviews — quarterly reconciliations catch discrepancies before they become systemic issues

- Use accounting software that meets NTA electronic record-keeping standards — ensures digital records are audit-ready and properly timestamped

Frequently Asked Questions

What is the Blue Form tax return in Japan?

The Blue Form tax return (aoiro shinkoku) is an elective filing status in Japan that provides enhanced tax benefits — including 10-year loss carryforward, special depreciation, and expanded deductions — to corporations and sole proprietors who maintain double-entry bookkeeping and submit an advance application to the National Tax Agency. It has been available since 1950 and is used by approximately 60% of Japanese corporations.

How do I apply for Blue Form status?

File the Blue Form Approval Application (青色申告承認申請書) at your jurisdictional tax office. New corporations must apply within 3 months of incorporation. Existing corporations must apply by the day before the start of the fiscal year they want Blue Form to take effect. There is no fee, and processing typically takes 1–2 months. No response from the NTA generally indicates approval.

Can Blue Form status be revoked?

Yes. The NTA can revoke Blue Form status for consecutive late filings (2 years), fraudulent returns, inadequate bookkeeping, or failure to comply with corrective orders. Revocation is retroactive to the start of the violation year, and companies must wait at least 1 year before re-applying. Revocation can result in loss of accumulated carryforward balances and reversal of special depreciation benefits.

Is Blue Form filing worth the additional record-keeping effort?

For virtually all corporations, yes. The tax savings from loss carryforward alone can exceed millions of yen, and the double-entry bookkeeping required is standard practice for any properly managed corporation. Companies already maintaining compliant accounting under J-GAAP will find that Blue Form requirements add minimal incremental burden. The benefits far outweigh the costs for any company with meaningful operations in Japan.

What happens if I miss the Blue Form application deadline?

You must wait until the next eligible fiscal year to apply. There is no late application process or exception mechanism. For new corporations, missing the 3-month window from incorporation means the earliest Blue Form status can begin is the second fiscal year. Any losses incurred during the White Form period cannot be carried forward, making timely application a high priority for companies expecting early-stage losses.

For assistance with Blue Form applications, ongoing tax compliance, and filing schedule management in Japan, contact AQ Partners for expert guidance tailored to foreign companies navigating the Japanese tax system. Learn more about loss carryforward strategies to maximize the value of your Blue Form status.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.