Transfer Pricing Documentation Requirements in Japan

Transfer pricing documentation in Japan refers to the formal records that multinational enterprises (MNEs) must prepare and maintain to demonstrate that transactions between related parties — such as a foreign parent company and its Japanese subsidiary — are conducted at arm's length prices. Governed by Articles 66-4 and 68-88 of Japan's Special Taxation Measures Act, these requirements align with the OECD's BEPS Action 13 framework. Japan adopted a three-tier documentation structure in 2016, requiring qualifying companies to prepare a Local File, Master File, and Country-by-Country Report (CbCR). Failure to maintain adequate documentation exposes companies to penalties and the risk that the National Tax Agency (NTA) will apply "secret comparables" to determine pricing unilaterally.

Key Takeaways

- Japan's three-tier framework mirrors OECD BEPS Action 13 standards — companies must prepare a Local File for related-party transactions exceeding ¥5 billion (or ¥300 million for intangibles), a Master File when consolidated group revenue reaches ¥100 billion, and a CbCR at the same threshold.

- Contemporaneous documentation is essential for audit defense — the NTA can request Local File documentation within 45 days of an examination notice. Companies that fail to produce it lose control of the pricing analysis, as the NTA may apply secret comparables.

- TNMM is the most commonly applied pricing method in Japan — approximately 80% of advance pricing arrangements concluded during 2019-2023 relied on TNMM benchmarking, according to NTA statistics.

- Penalties include under-reporting surcharges of 10-15% plus interest — aggravated penalties apply when taxpayers fail to maintain documentation. Double taxation risk compounds the financial exposure.

- Foreign subsidiaries should prepare documentation proactively, even below formal thresholds — the NTA can request transfer pricing information from any company with related-party transactions, regardless of whether statutory thresholds are met.

What Is Transfer Pricing Documentation in Japan?

Transfer pricing documentation is the set of contemporaneous records proving that intercompany transactions are priced consistently with the arm's length principle — the cornerstone of Japan's international tax enforcement.

Japan's transfer pricing rules are codified in the Special Taxation Measures Act, which empowers the NTA to adjust taxable income when related-party transactions deviate from prices that independent enterprises would agree under comparable circumstances. A "related party" generally includes any entity where one party holds 50% or more of voting rights, directly or indirectly, though functional control tests can extend this definition.

According to the PwC Japan tax summary, Japan's implementation closely follows the OECD's three-tier structure but with Japan-specific thresholds and filing requirements that differ from other BEPS-adopting jurisdictions.

Three-Tier Documentation Framework

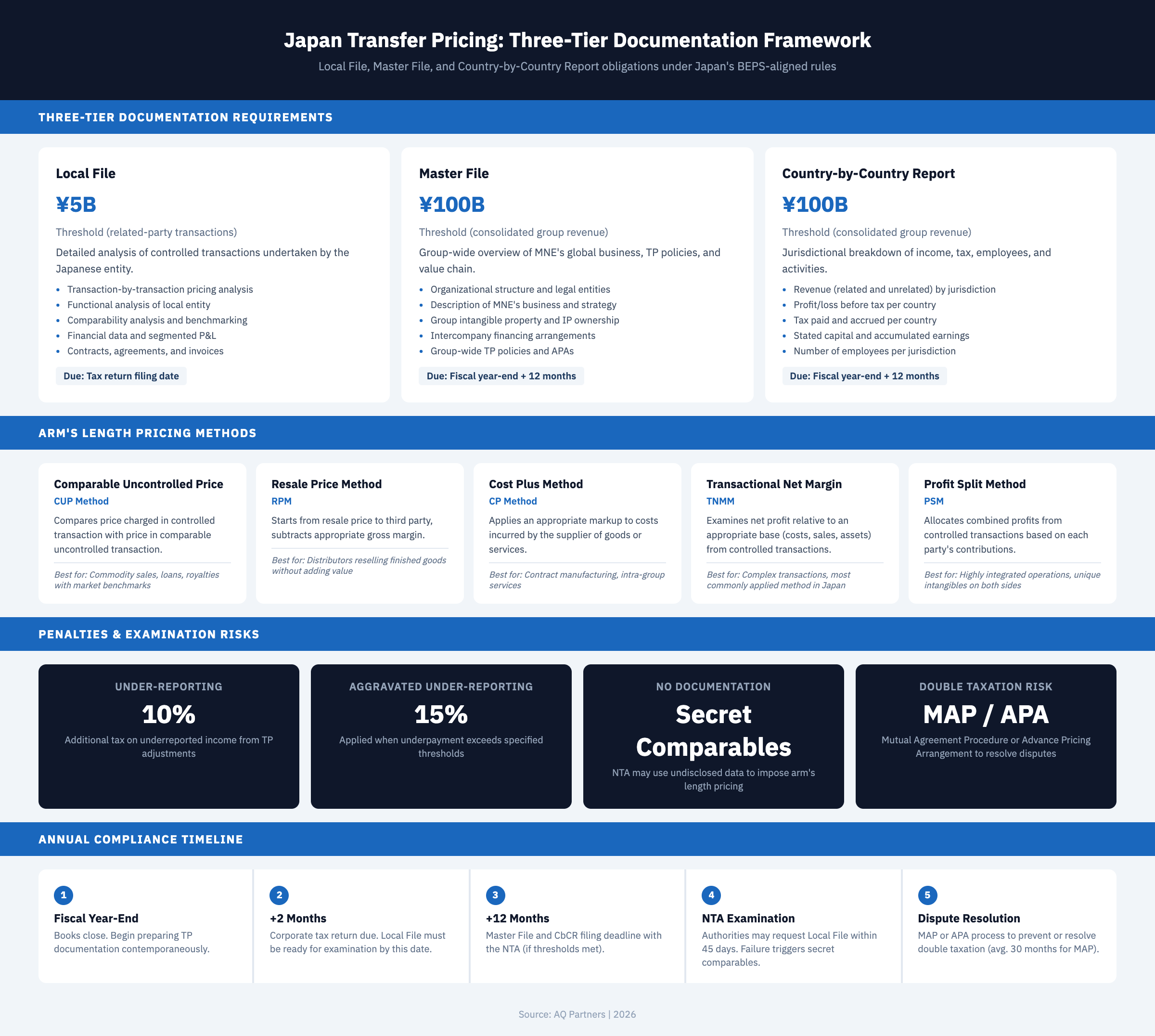

Japan requires three documentation tiers — the Local File, Master File, and Country-by-Country Report — each subject to separate filing thresholds and targeting different aspects of an MNE's transfer pricing arrangements.

The Local File contains a detailed transactional analysis of the Japanese entity's intercompany dealings. Companies must prepare it when related-party transactions with a single counterpart exceed ¥5 billion in a fiscal year, or when intangible transactions exceed ¥300 million. It must be ready by the corporate tax return filing deadline — typically two months after fiscal year-end — and produced within 45 days of an NTA examination request.

The Master File provides a high-level overview of the MNE group's global operations and transfer pricing policies. This applies when the group's consolidated revenue reaches ¥100 billion or more. It must be filed electronically with the NTA within 12 months of the ultimate parent entity's fiscal year-end.

The Country-by-Country Report provides a jurisdictional breakdown of revenue, profit, tax paid, employees, and tangible assets. The same ¥100 billion threshold applies. According to the NTA's 2024 annual report, Japan exchanges CbCR data with over 80 jurisdictions under the Multilateral Competent Authority Agreement.

| Documentation Tier | Threshold | Content Focus | Deadline | Filing Method | Language |

|---|---|---|---|---|---|

| Local File | ¥5B per counterpart or ¥300M intangibles | Transaction-level pricing analysis, comparables | Tax return date (FY-end + 2 months) | Prepared; produced on NTA request | Japanese preferred |

| Master File | ¥100B consolidated revenue | Group TP policies, structure, IP allocation | Parent FY-end + 12 months | e-Tax electronic filing | Japanese or English |

| CbCR | ¥100B consolidated revenue | Jurisdictional revenue, profit, tax, employees | Parent FY-end + 12 months | e-Tax electronic filing | Japanese or English |

| Parent Entity Notification | All MNE groups with CbCR obligations | Identification of ultimate parent or surrogate filer | Ultimate parent FY-end | Filed with NTA | Japanese |

| Voluntary Local File | No formal threshold | Same as Local File — for audit defense | Best practice: tax return date | Not required but recommended | Japanese preferred |

| APA Documentation | Elective | Prospective pricing methodology agreed with NTA | Filed before transactions occur | Application to NTA | Japanese |

Filing Thresholds and Deadlines

Japan's documentation thresholds are among the highest in Asia-Pacific, meaning many mid-sized foreign subsidiaries fall below the formal mandate — but the NTA can still examine any company's transfer pricing.

The ¥5 billion (approximately USD 34 million) Local File threshold applies per related-party counterpart. A subsidiary transacting with three affiliates — each below ¥5 billion — would not trigger the requirement, even if aggregate transactions far exceed that amount. Tax practitioners widely recommend voluntary documentation when total intercompany transactions are material relative to revenue.

The ¥100 billion (approximately USD 680 million) Master File/CbCR threshold aligns with the OECD's EUR 750 million benchmark. According to PwC's analysis, approximately 800-900 Japanese-headquartered MNE groups file CbCRs annually. Foreign-headquartered groups may have their CbCR filed by the ultimate parent in the home jurisdiction, provided that country has an exchange agreement with Japan.

Key deadlines follow the Japanese fiscal year cycle. The corporate tax return is due two months after fiscal year-end, with the Local File ready by that date. Master Files and CbCRs are due 12 months after the ultimate parent's fiscal year-end.

Arm's Length Methods and Comparable Analysis

Japanese law recognizes five transfer pricing methods — CUP, Resale Price, Cost Plus, TNMM, and Profit Split — with a "most appropriate method" rule requiring taxpayers to select the method best suited to each transaction.

The Transactional Net Margin Method (TNMM) dominates Japanese transfer pricing practice. NTA statistics indicate TNMM was applied in approximately 80% of APAs concluded during 2019-2023. TNMM examines net profit relative to an appropriate base (costs, sales, or assets) and is favored for benchmarking routine activities of Japanese subsidiaries.

The Comparable Uncontrolled Price (CUP) method compares controlled transaction prices directly with comparable uncontrolled prices. It requires high comparability and suits commodity transactions, intercompany loans, and royalties with market benchmarks. The Resale Price and Cost Plus methods focus on gross margins — Resale Price for distributors, Cost Plus for contract manufacturers. The Profit Split method allocates combined profits based on each party's contributions and applies when both parties contribute unique intangibles.

Comparability analysis requires consideration of five factors: characteristics of goods or services, functional analysis, contractual terms, economic circumstances, and business strategies. Database searches using tools such as Bureau van Dijk's Orbis are standard for TNMM benchmarking in Japan.

NTA Examinations and Penalties

The NTA's transfer pricing examination program targets high-risk transactions through CbCR data analysis — non-compliant taxpayers face penalties of 10-15%, interest charges, and the punitive application of secret comparables.

The NTA concluded approximately 200 transfer pricing examinations with adjustments in fiscal year 2022, with total adjustments exceeding ¥60 billion (NTA Annual Report 2023). Audits typically span 2-4 assessment years. When the NTA issues an examination notice, the taxpayer must produce the Local File within 45 days. Failure triggers the NTA's authority to use its undisclosed third-party database — "secret comparables" — to determine arm's length pricing, with no taxpayer review of the data used.

| Penalty / Risk | Rate or Consequence | Trigger | Notes |

|---|---|---|---|

| Under-Reporting Penalty | 10% of additional tax | TP adjustment by NTA | Standard penalty for non-arm's length pricing |

| Aggravated Under-Reporting | 15% of additional tax | Significant underpayment or no documentation | Applies when taxpayer lacks required records |

| Delinquent Tax Interest | ~8.7% per annum | Any additional tax from TP adjustment | Accrues from original due date; rate varies annually |

| Secret Comparables | NTA unilateral pricing | No Local File within 45 days | Taxpayer cannot review NTA's benchmark data |

| Double Taxation | Tax in two jurisdictions | TP adjustment without corresponding relief | Requires MAP or bilateral APA to resolve |

| MAP Resolution Timeline | Average 30.1 months | Taxpayer initiates competent authority request | Below OECD average of 32 months (OECD 2023) |

Double taxation is a critical risk. Japan processed 159 MAP cases in fiscal year 2023, with average resolution of 30.1 months according to NTA statistics. Bilateral APAs provide a proactive alternative, typically covering 3-5 fiscal years. The NTA concluded approximately 117 bilateral APAs in fiscal year 2022, making Japan one of the world's most active APA jurisdictions.

Practical Compliance Strategies for Foreign Subsidiaries

Foreign companies in Japan should treat transfer pricing documentation as an annual compliance obligation integrated into the tax return filing cycle — not a reactive exercise triggered by audit.

The most effective approach is contemporaneous documentation: preparing the Local File alongside the annual financial close. This ensures the analysis reflects current business conditions and is ready before the NTA's 45-day deadline becomes relevant. Companies that defer documentation until audit often find key personnel have departed and reconstructing the analysis years later produces weaker results.

Even below the ¥5 billion threshold, voluntary preparation remains advisable when intercompany transactions are material. The JETRO business setup guide notes that tax compliance is among the most complex aspects of operating in Japan for foreign companies.

Key strategies include: aligning intercompany agreements with actual conduct (the NTA examines economic substance, not just contracts); maintaining segmented financial data for transaction-level analysis; refreshing benchmark studies periodically; and considering bilateral APAs for high-value arrangements. Japanese documentation must also be consistent with the group's global TP policy — inconsistencies between the Master File and Local File create audit risk. Corporate income tax obligations in Japan are complex enough that transfer pricing coordination deserves dedicated attention.

AQ Partners supports foreign companies in Japan with back-office operations including tax compliance, financial reporting, and transfer pricing documentation coordination — ensuring intercompany pricing aligns with both Japanese requirements and global group policies.

Frequently Asked Questions

Do all companies with intercompany transactions need TP documentation?

Mandatory Local File preparation applies only above the ¥5 billion (single counterpart) or ¥300 million (intangibles) thresholds. However, the NTA can request transfer pricing information from any company with related-party transactions during an examination. Tax advisors strongly recommend voluntary documentation for any subsidiary with material intercompany dealings, as it strengthens audit defense and prevents the NTA from invoking secret comparables.

What happens if documentation is not produced within 45 days?

The NTA gains authority to apply "secret comparables" — undisclosed third-party data — to determine arm's length pricing. The taxpayer cannot review or challenge the specific comparables used, effectively losing control of the pricing analysis. This is the most severe procedural consequence in Japan's TP framework.

How does Japan's TP regime interact with tax treaties?

Japan has over 80 tax treaties with MAP and associated enterprise provisions. When an NTA adjustment creates double taxation, companies can request MAP relief through both jurisdictions' competent authorities. Japan also actively participates in bilateral APAs — concluding approximately 117 in fiscal year 2022, among the highest globally.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.