Japan Consumption Tax (Shouhizei): Complete Guide for Foreign Companies

Japan's consumption tax (消費税, shōhizei) is a value-added tax levied at 10% on most goods and services sold within Japan, with a reduced 8% rate on qualifying food items and newspaper subscriptions. Every foreign company operating in Japan—whether selling products, providing services, or maintaining a local subsidiary—must understand consumption tax obligations from the earliest stages of market entry. Unlike sales taxes in some jurisdictions, Japan's consumption tax applies at every stage of the supply chain, with businesses claiming input tax credits to avoid cascading taxation. Since October 2023, the Qualified Invoice System (インボイス制度, invoice seido) has fundamentally changed how these credits work, requiring registered invoices for all input tax deductions.

Key Takeaways

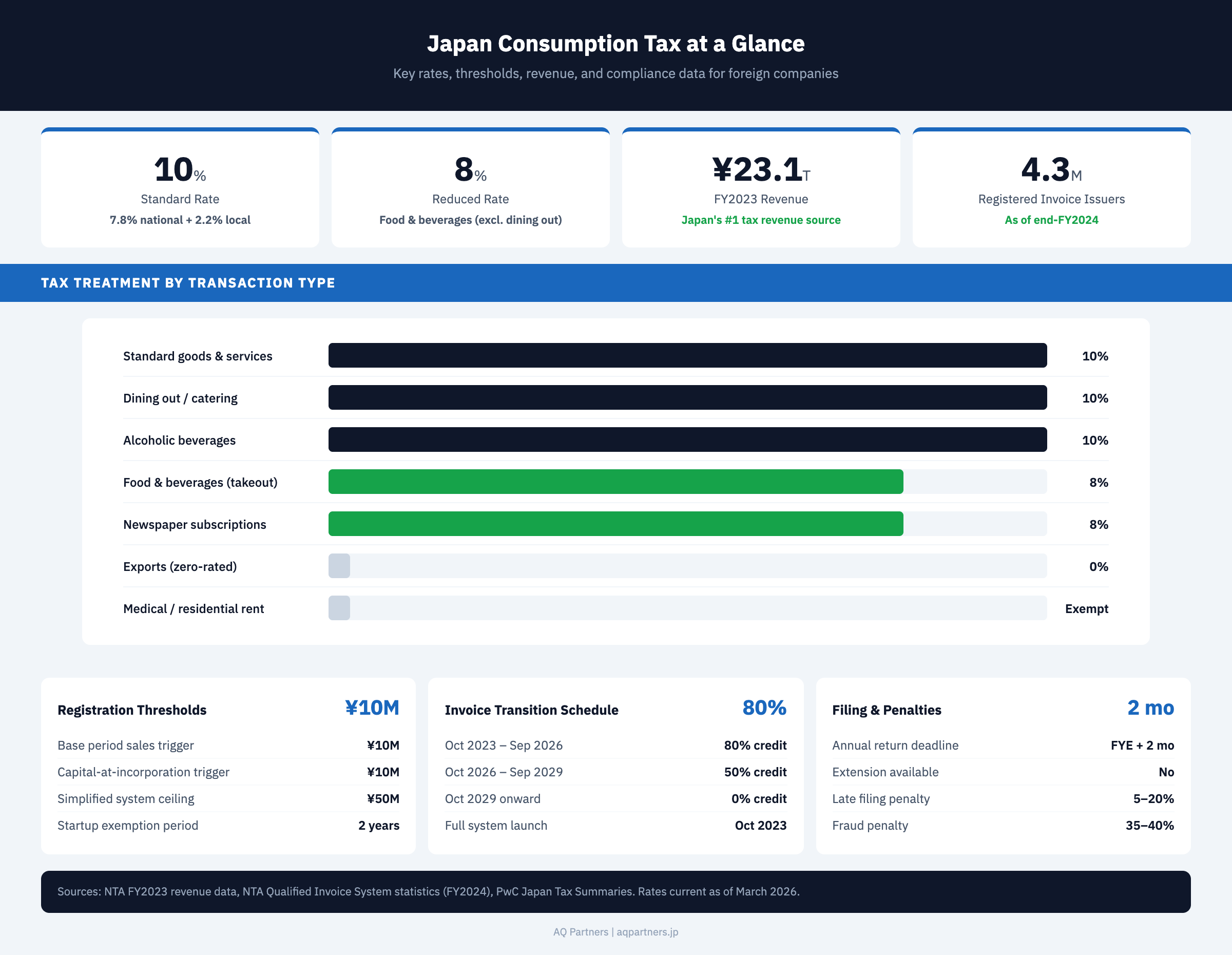

- Japan's consumption tax applies at two rates—10% standard and 8% reduced—the standard rate covers most goods and services, while the reduced rate applies exclusively to food and non-alcoholic beverages (excluding dining out) and newspaper subscriptions delivered twice or more per week.

- Companies with taxable sales exceeding ¥10 million in the base period must register—the base period is the fiscal year two years prior, meaning newly incorporated companies are generally exempt for their first two fiscal years unless their stated capital is ¥10 million or more at incorporation.

- The Qualified Invoice System launched October 2023 requires registered invoices for input tax credits—businesses purchasing from unregistered suppliers can only claim transitional credits of 80% (through September 2026), then 50% (through September 2029), then 0% from October 2029 onward.

- Exports are zero-rated while imports are taxed at the border—foreign companies selling into Japan face import consumption tax at customs, while those exporting from Japan can claim full refunds on input tax through zero-rating. B2B digital services from overseas trigger a reverse-charge mechanism.

- Late filing and underpayment penalties range from 5% to 40% of the tax due—the National Tax Agency (NTA) imposes graduated penalties including a 15–20% additional tax for underreporting, up to 35–40% for fraudulent returns, plus delinquency interest at approximately 8.7% annually on unpaid balances.

Understanding Japan's Consumption Tax System

Japan's consumption tax is a multi-stage value-added tax collected at each point of the supply chain, with the final economic burden falling on the end consumer. Businesses act as collection agents—they charge consumption tax on sales (output tax), deduct consumption tax paid on purchases (input tax), and remit the difference to the tax authorities.

The consumption tax was first introduced in 1989 at 3%, raised to 5% in 1997, to 8% in 2014, and to the current 10% in October 2019. The October 2019 increase also introduced the dual-rate system with an 8% reduced rate for the first time. According to the NTA's consumption tax overview, the tax generated approximately ¥23.1 trillion in revenue for fiscal year 2023, making it Japan's single largest tax revenue source—surpassing both income tax and corporate tax.

For foreign companies establishing operations in Japan, consumption tax affects virtually every business transaction: purchasing office supplies, leasing real estate, hiring contractors, importing goods, and selling products or services domestically. Understanding the registration threshold, invoice requirements, and filing obligations is essential for accurate financial planning and maintaining tax compliance in Japan.

Standard and Reduced Tax Rates

Japan applies a 10% standard consumption tax rate to most goods and services and an 8% reduced rate to specified food and beverage items and newspaper subscriptions. Both rates include a national component and a local consumption tax component.

The rate breakdown is as follows: the 10% standard rate comprises 7.8% national consumption tax and 2.2% local consumption tax. The 8% reduced rate comprises 6.24% national and 1.76% local. While businesses file a single return covering both components, understanding this split matters for calculating input tax credits correctly under the Qualified Invoice System.

| Category | Tax Rate | National Component | Local Component | Examples |

|---|---|---|---|---|

| Standard rate | 10% | 7.8% | 2.2% | Electronics, consulting fees, rent, transportation |

| Reduced rate | 8% | 6.24% | 1.76% | Grocery food, non-alcoholic beverages, newspaper subscriptions (2+/week) |

| Dining out / catering | 10% | 7.8% | 2.2% | Restaurant meals, in-store dining, catering services |

| Takeout food | 8% | 6.24% | 1.76% | Food purchased for takeaway, delivery meals |

| Alcoholic beverages | 10% | 7.8% | 2.2% | Beer, wine, spirits (even when sold at grocery stores) |

| Medical services | Exempt | — | — | Services covered by public health insurance |

| Residential rent | Exempt | — | — | Residential leases (commercial rent is taxable at 10%) |

| Financial transactions | Exempt | — | — | Interest, insurance premiums, securities transactions |

| Exports | 0% (zero-rated) | — | — | Goods shipped outside Japan, international transport |

| Land sales | Exempt | — | — | Transfer of land (building sales are taxable) |

The distinction between dining-in (10%) and takeout (8%) creates one of the most discussed edge cases in Japan's tax system. A convenience store onigiri (rice ball) taxed at 8% when taken away becomes 10% if the customer uses an in-store eating area. Businesses selling both dine-in and takeout food must track each transaction type separately for accurate consumption tax reporting.

Exempt transactions differ fundamentally from zero-rated transactions. Exempt sales—such as medical services, residential rent, and financial transactions—do not allow the seller to claim input tax credits on related purchases. Zero-rated sales (primarily exports) allow full input tax credit recovery, making zero-rating significantly more favorable for businesses. This distinction is critical for foreign companies with export-heavy operations, as discussed in the cross-border consumption tax guide.

Registration Thresholds and Exemptions

Companies with taxable sales exceeding ¥10 million in the base period (the fiscal year two years prior) are required to register as consumption tax taxpayers. Companies below this threshold may elect voluntary registration to recover input tax credits.

The base period rule creates a two-year lag: a company's consumption tax obligation for fiscal year 2026 is determined by its taxable sales in fiscal year 2024. Newly incorporated companies with no base period are generally treated as tax-exempt enterprises for their first two fiscal years. However, there are important exceptions.

Companies incorporated with stated capital of ¥10 million or more are immediately subject to consumption tax from their first fiscal year, regardless of actual sales. Additionally, if a company's taxable sales in the first six months of the preceding fiscal year exceed ¥10 million (or if taxable payroll in that six-month period exceeds ¥10 million), the company becomes a taxable enterprise in the current year. According to PwC's Japan tax summary, approximately 60% of all corporations in Japan are classified as tax-exempt enterprises—primarily small businesses below the ¥10 million threshold.

For foreign companies entering Japan, the capital threshold is particularly relevant. Most foreign subsidiaries are capitalized above ¥10 million to meet Business Manager Visa requirements and demonstrate financial credibility. This means consumption tax obligations typically begin from day one of operations, with no two-year exemption period. Detailed registration procedures are covered in the consumption tax registration guide.

The Qualified Invoice System (Invoice Seido)

Since October 1, 2023, the Qualified Invoice System (適格請求書等保存方式, tekikaku seikyūsho-tō hozon hōshiki) requires businesses to obtain and retain qualified invoices to claim input tax credits on purchases. Only invoices issued by registered invoice issuers carry credit eligibility.

The system replaced the previous account-based method where any invoice supporting a purchase could serve as the basis for an input tax credit. Under the new system, businesses must register with the NTA to receive a registration number (T + 13-digit number for corporations, matching the corporate number). This registration number must appear on all invoices, along with specific required information including the applicable tax rate and tax amount broken down by rate category.

According to the NTA's invoice system guidance, approximately 4.3 million businesses had registered as qualified invoice issuers by the end of fiscal year 2024. The system is particularly significant for foreign companies because purchases from unregistered suppliers—including many small Japanese vendors and freelancers—no longer qualify for full input tax credits.

Transitional Credit Rules

To ease the transition, the NTA established a phased reduction in credits available for purchases from unregistered suppliers:

- October 2023 – September 2026: 80% of the input tax on purchases from unregistered suppliers can still be credited

- October 2026 – September 2029: Credit reduced to 50% of input tax

- October 2029 onward: No credit available for purchases from unregistered suppliers

Foreign companies should audit their Japanese supplier base to identify unregistered vendors and factor the declining credit into procurement planning. The full details of invoice requirements, format specifications, and digital recordkeeping obligations are covered in the Qualified Invoice System guide.

Input Tax Credits: How Consumption Tax Recovery Works

Input tax credits allow businesses to deduct the consumption tax paid on business purchases from the consumption tax collected on sales, so only the net difference is remitted to the tax authorities. Proper documentation under the Qualified Invoice System is now mandatory for claiming these credits.

The basic calculation is straightforward: Output Tax (consumption tax charged on sales) minus Input Tax (consumption tax paid on purchases) equals the amount due to the NTA. If input tax exceeds output tax—common for export-oriented businesses and companies making large capital investments—the difference is refunded.

The input tax credit system operates under two methods: the itemized method (個別対応方式) and the proportional method (一括比例配分方式). Under the itemized method, input tax is allocated directly to taxable sales, exempt sales, or common expenses. Under the proportional method, input tax is credited based on the ratio of taxable sales to total sales. Companies with a taxable sales ratio of 95% or higher and taxable sales of ¥500 million or less may credit all input tax without allocation.

The Simplified Tax System (Kan'i Kazei)

Companies with base period taxable sales of ¥50 million or less can elect the Simplified Tax System (簡易課税制度, kan'i kazei seido), which calculates input tax credits as a fixed percentage of output tax based on industry classification. This eliminates the need to track actual input tax on every purchase.

| Industry Classification | Deemed Purchase Rate | Effective Tax Burden | Typical Businesses |

|---|---|---|---|

| Type 1: Wholesale | 90% | 1% of sales | Trading companies, distributors |

| Type 2: Retail | 80% | 2% of sales | Retail stores, e-commerce sellers |

| Type 3: Manufacturing | 70% | 3% of sales | Manufacturers, construction |

| Type 4: Other | 60% | 4% of sales | Restaurants, food processing (from purchased materials) |

| Type 5: Services | 50% | 5% of sales | Consulting, IT services, transportation, communications |

| Type 6: Real estate | 40% | 6% of sales | Real estate rental, leasing |

The Simplified Tax System is attractive for service businesses (Type 5) that have few deductible purchases—the deemed 50% purchase rate may exceed their actual input tax, creating a tax advantage. However, service-heavy foreign subsidiaries should model both the standard and simplified methods before electing, as the election must be filed by the day before the fiscal year starts and is binding for at least two years.

Filing and Payment Requirements

Corporations must file an annual consumption tax return within two months after the end of their fiscal year. Depending on the prior year's consumption tax liability, interim payments may also be required quarterly, semi-annually, or monthly.

The filing deadline mirrors the corporate income tax filing deadline—both are due two months after the fiscal year end. For a company with a March 31 fiscal year end, the consumption tax return is due by May 31. Unlike corporate tax, consumption tax returns cannot receive a one-month filing extension.

Interim Payment Requirements

The NTA requires interim consumption tax payments based on the previous year's annual liability:

- Annual liability under ¥480,000: No interim payments required

- ¥480,000 to ¥4 million: One semi-annual interim payment

- ¥4 million to ¥48 million: Three quarterly interim payments

- Over ¥48 million: Eleven monthly interim payments

Interim payments are calculated as equal installments of the prior year's liability divided by the applicable number of periods. Companies may instead file actual interim returns based on current-period figures, which is beneficial when business volume has decreased. The full details of filing schedules, payment methods, and deadline management are covered in the consumption tax filing and deadlines guide.

Cross-Border Consumption Tax Rules

Exports from Japan are zero-rated (0% consumption tax with full input credit recovery), while imports are subject to consumption tax at the border. Digital services provided cross-border have specific rules depending on whether the recipient is a business or consumer.

Zero-rating on exports means a Japan-based manufacturer exporting goods pays no consumption tax on the export sale but can still claim credits for all consumption tax paid on domestic purchases used to produce those goods. This creates a net refund position—one reason why export-heavy manufacturers in Japan routinely receive consumption tax refunds from the NTA.

For imports, Japan Customs assesses consumption tax on the CIF (cost, insurance, freight) value of imported goods plus any applicable customs duties. The importer pays this at the time of customs clearance and can claim it as an input tax credit on their consumption tax return, provided they retain proper documentation.

Cross-border digital services—including cloud computing, streaming, advertising, and SaaS provided to Japanese customers from overseas—are subject to consumption tax under rules introduced in 2015. B2B digital services trigger a reverse-charge mechanism where the Japanese recipient self-assesses and reports the consumption tax. B2C digital services require the foreign provider to register with the NTA and file consumption tax returns directly. Platform operators became liable for consumption tax on B2C digital services from foreign providers effective April 2025. The full treatment of exports, imports, and digital services is explained in the cross-border consumption tax guide.

Penalties for Non-Compliance

The NTA imposes a graduated penalty structure for late filing, underreporting, and non-payment of consumption tax, with additional penalties for fraudulent or willfully negligent behavior.

| Violation | Penalty | Rate / Amount | Notes |

|---|---|---|---|

| Late filing (voluntary) | Delinquent return penalty | 5% of tax due | Filed voluntarily before NTA notice |

| Late filing (after NTA notice) | Delinquent return penalty | 15–20% of tax due | 15% on first ¥500K; 20% on amounts exceeding ¥500K |

| Underreporting (negligent) | Additional tax | 10–15% | 10% on first ¥500K of additional tax; 15% on excess |

| Underreporting (fraudulent) | Heavy additional tax | 35–40% | Applied when willful concealment or fraud is found |

| Non-filing | Delinquent return penalty | 15–20% | Plus potential criminal prosecution for willful evasion |

| Late payment | Delinquency interest | ~2.4% (first 2 months); ~8.7% thereafter | Rates adjusted annually; FY2024 rates shown |

| Repeat offender | Enhanced penalty | +10% surcharge | Additional surcharge for entities penalized within prior 5 years |

| Criminal tax evasion | Criminal penalty | Up to 10 years imprisonment; ¥10M fine | Prosecuted in serious evasion cases |

For foreign companies, consumption tax non-compliance can trigger broader scrutiny from the NTA. Tax audits initiated by consumption tax irregularities frequently expand to cover corporate income tax, withholding tax, and source taxation on cross-border payments. The NTA conducted approximately 56,000 consumption tax audits in fiscal year 2023, resulting in additional assessments totaling ¥132.8 billion. Companies operating in Japan should ensure consumption tax compliance is integrated into their overall tax compliance framework.

Frequently Asked Questions

Does my foreign company need to charge consumption tax on services provided from outside Japan to Japanese clients?

It depends on the type of service. For B2B digital services (cloud services, SaaS, digital advertising) provided to Japanese business customers, the reverse-charge mechanism applies—your Japanese client self-assesses and reports the consumption tax. For B2C digital services provided to Japanese consumers, the foreign provider must register with the NTA and file consumption tax returns directly. Non-digital services provided from outside Japan are generally outside the scope of Japanese consumption tax.

Can newly incorporated companies in Japan avoid consumption tax registration?

Companies with stated capital under ¥10 million and no base period sales history are generally exempt from consumption tax for their first two fiscal years. However, most foreign subsidiaries are capitalized at ¥10 million or above to meet Business Manager Visa requirements, which triggers immediate consumption tax obligations. Companies may also become taxable mid-year if their first six months' taxable sales or payroll exceeds ¥10 million.

What is the difference between exempt and zero-rated transactions for consumption tax purposes?

Zero-rated transactions (primarily exports) are taxable at 0%, which means the seller can still claim input tax credits on purchases related to those sales—often resulting in a net refund from the NTA. Exempt transactions (such as medical services, residential rent, and financial transactions) carry no consumption tax, but the seller cannot claim input tax credits on related purchases. For businesses with significant exempt sales, this can create a permanent consumption tax cost on inputs.

How does the Simplified Tax System benefit foreign companies?

The Simplified Tax System allows companies with base period taxable sales of ¥50 million or less to calculate input tax credits as a fixed percentage of output tax, eliminating the need to track actual input tax on every purchase. This reduces administrative burden and can create a tax advantage for service companies (Type 5) where the deemed 50% purchase rate exceeds actual deductible inputs. The election must be filed before the start of the fiscal year and is binding for at least two years.

Consumption tax is one of the most operationally significant taxes for foreign companies in Japan—affecting every purchase, sale, and import. Proper registration, invoice compliance, and filing discipline are essential to avoiding penalties and maximizing input tax credit recovery. AQ Partners provides comprehensive back office support including consumption tax registration, return preparation, and Qualified Invoice System compliance for foreign companies operating in Japan. Contact us at hello@aqpartners.jp to discuss your consumption tax obligations.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.