Consumption Tax Filing & Payment Deadlines in Japan

Consumption tax filing in Japan requires taxable enterprises to submit an annual return within two months after their fiscal year end and, depending on the prior year's tax liability, make interim payments on a monthly, quarterly, or semi-annual basis. Unlike corporate income tax, consumption tax returns are not eligible for filing extensions—missing the deadline triggers automatic penalties regardless of circumstances. For foreign companies operating in Japan, coordinating consumption tax deadlines with corporate tax, local tax, and withholding tax obligations requires careful calendar management throughout the fiscal year.

Key Takeaways

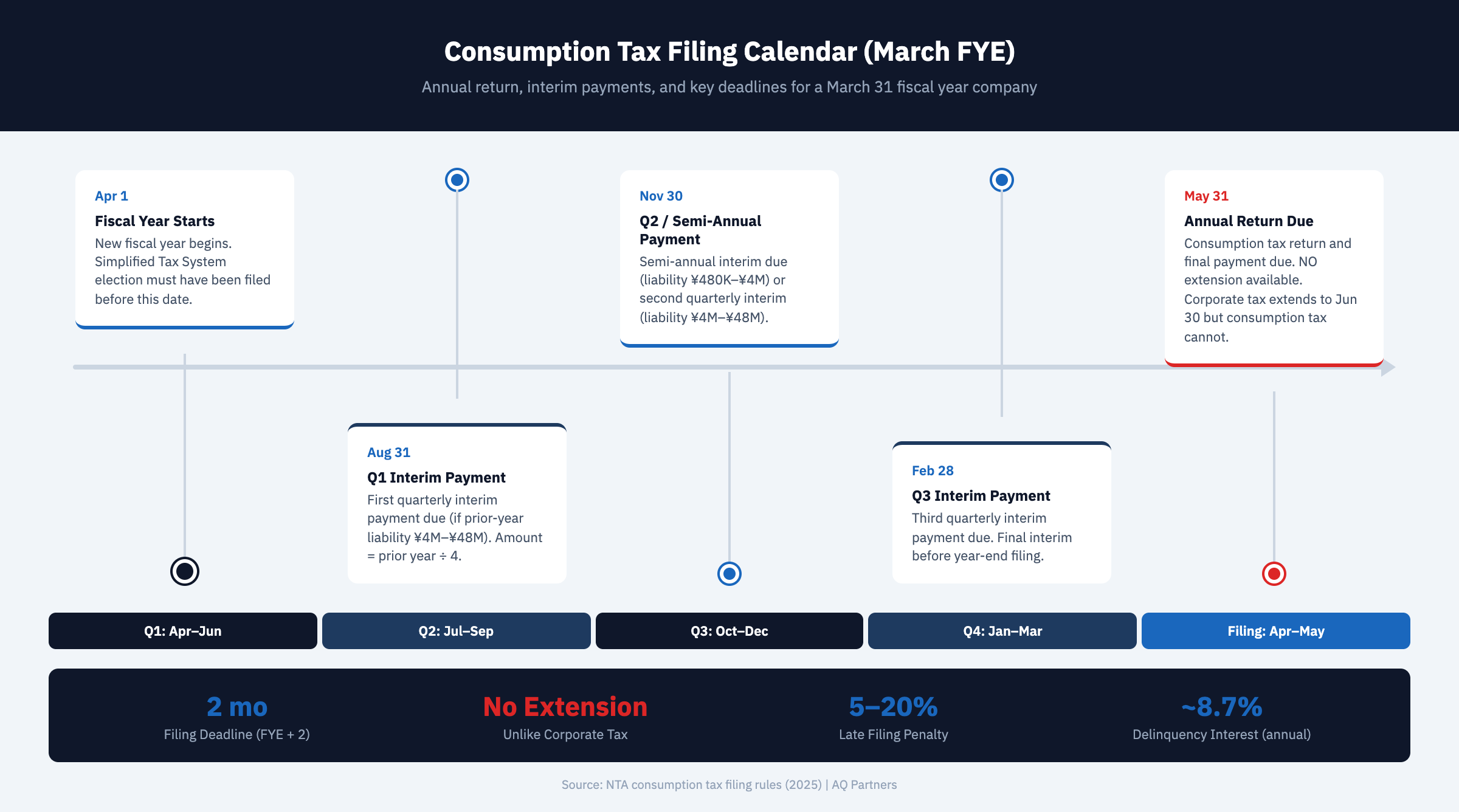

- Annual consumption tax returns are due two months after fiscal year end—with no extension available—for a March 31 fiscal year, the return is due May 31. Corporate income tax allows a one-month extension to June 30, but consumption tax does not, creating a split deadline that catches many foreign companies off guard.

- Interim payments are mandatory when prior-year liability exceeds ¥480,000—the NTA requires one semi-annual, three quarterly, or eleven monthly interim payments depending on the prior year's consumption tax amount, with payment due within two months after each interim period ends.

- Late filing penalties start at 5% and can reach 20% of the tax due—voluntary late filing incurs a 5% penalty, while filing after NTA notice triggers 15–20%, plus delinquency interest at approximately 8.7% per annum on unpaid balances accruing from the original due date.

- Refund claims for export-heavy businesses follow the same deadline—companies in a net refund position must file the annual return by the two-month deadline to claim their refund, with the NTA typically processing refunds within one to two months of filing.

- The consumption tax filing calendar differs from corporate tax in critical ways—no filing extension, different interim payment thresholds, and separate forms create a parallel compliance track that must be managed independently from corporate income tax obligations.

Annual Return Filing Deadline

Every taxable enterprise must file an annual consumption tax return (消費税確定申告書) within two months after the end of its fiscal year. Payment of the net consumption tax due must accompany the filing.

For a company with a March 31 fiscal year end, the consumption tax return is due by May 31. If the due date falls on a Saturday, Sunday, or national holiday, the deadline extends to the next business day. The return covers the entire fiscal year and reconciles all output tax collected, input tax credits claimed, and interim payments already made during the year.

Foreign companies often operate with fiscal years aligned to their global parent—December 31 is common for US- and Europe-headquartered companies. In that case, the consumption tax return is due by the last day of February. The consumption tax guide covers the underlying tax calculation, rate structure, and input credit mechanics that determine the amounts reported on the annual return.

Why Consumption Tax Has No Filing Extension

Unlike corporate income tax, which permits a one-month filing extension (from two months to three months after fiscal year end) upon application, consumption tax returns cannot be extended under any circumstances. This is one of the most commonly misunderstood differences in Japan's tax filing system.

The distinction exists because the consumption tax is an indirect tax—the company is holding tax collected from customers, and the NTA treats timely remittance as a priority. Companies that routinely extend their corporate tax filing deadline must still file their consumption tax return on the original two-month deadline. For a March 31 fiscal year company that extends corporate tax filing to June 30, consumption tax is still due May 31—a full month earlier.

This split deadline requires separate preparation workflows for consumption tax and corporate tax returns. According to the NTA's consumption tax guidance, failure to file by the deadline results in automatic penalties regardless of whether payment was made on time.

Interim Payment Schedule

The NTA requires interim consumption tax payments based on the prior fiscal year's annual net consumption tax liability. The number of interim payments increases with the size of the liability.

| Prior-Year Liability | Interim Frequency | Number of Payments | Payment Due | Amount Per Payment |

|---|---|---|---|---|

| Under ¥480,000 | None | 0 | N/A | Full amount at year-end filing |

| ¥480,000 – ¥4,000,000 | Semi-annual | 1 | 2 months after mid-year | Prior year liability ÷ 2 |

| ¥4,000,000 – ¥48,000,000 | Quarterly | 3 | 2 months after each quarter | Prior year liability ÷ 4 |

| Over ¥48,000,000 | Monthly | 11 | 2 months after each month | Prior year liability ÷ 12 |

Interim payments are calculated based on the prior year's national consumption tax component (7.8% rate portion) only, not the full 10% amount. The local consumption tax portion (2.2% rate) is settled on the annual return. Each interim payment is due within two months after the end of the interim period. For a March 31 fiscal year company with quarterly interim payments, payments are due by November 30, February 28 (or 29), and August 31 for the first three quarters, with the final settlement on the May 31 annual return.

Actual Interim Returns

Companies may choose to file actual interim consumption tax returns instead of using the prior-year-based calculation. This is advantageous when the current year's consumption tax liability is expected to be significantly lower than the prior year—for example, due to reduced sales volume, a shift toward export (zero-rated) sales, or major capital investments generating large input tax credits. Actual interim returns require complete calculation of consumption tax for the interim period, effectively creating a mini annual return for each period.

Consumption Tax vs. Corporate Tax Filing Calendar

Foreign companies must manage consumption tax and corporate income tax as separate compliance tracks with different deadlines, extension rules, and interim payment structures.

| Feature | Consumption Tax | Corporate Income Tax |

|---|---|---|

| Annual return deadline | FYE + 2 months | FYE + 2 months |

| Filing extension available | No | Yes (+1 month, to FYE + 3 months) |

| Interim payment threshold | ¥480,000 prior-year liability | ¥200,000 prior-year tax |

| Interim payment frequency | Semi-annual, quarterly, or monthly | Semi-annual (one interim payment) |

| Late filing penalty | 5–20% of tax due | 5–20% of tax due |

| Delinquency interest rate | ~2.4% (first 2 months); ~8.7% thereafter | Same rates |

| Filing method | e-Tax or paper | e-Tax (mandatory for large corps) or paper |

| Refund processing time | 1–2 months | 1–2 months |

The split deadline is the most critical difference. Companies that routinely file corporate tax on the extended deadline must build a separate internal process to ensure their consumption tax return is completed a month earlier. Failure to recognize this distinction is one of the most common compliance errors among foreign companies operating in Japan, according to JETRO's business setup guide.

Penalties for Late Filing and Non-Payment

The NTA imposes a graduated penalty structure for late filing, underpayment, and non-payment of consumption tax. Penalties apply automatically—there is no discretionary waiver process for first-time offenders.

Voluntary late filing (filing after the deadline but before receiving NTA notice) incurs a 5% delinquent return penalty (無申告加算税). Filing after NTA notice raises the penalty to 15% on the first ¥500,000 of tax due and 20% on amounts exceeding ¥500,000. Underreporting discovered during an NTA audit triggers an additional tax (過少申告加算税) of 10–15%, escalating to 35–40% if fraud or willful concealment is found.

Delinquency interest (延滞税) accrues from the original due date on any unpaid balance. The rate for fiscal year 2024 is approximately 2.4% for the first two months and 8.7% thereafter. These rates are adjusted annually based on market interest rates. Companies with repeated violations within five years face an additional 10% surcharge on all penalties.

The full penalty schedule including criminal prosecution thresholds is covered in the consumption tax guide.

Refund Claims and Processing

Companies with input tax credits exceeding output tax—common for exporters, companies in their startup phase, and businesses making large capital investments—receive consumption tax refunds by filing the annual return showing a negative net amount.

The refund is processed through the same annual return filing—there is no separate refund application. The NTA typically processes refund claims within one to two months of filing, depositing the refund directly to the company's designated bank account. Companies filing via e-Tax generally receive refunds faster than paper filers. To claim a refund, the company must be registered as a taxable enterprise; tax-exempt enterprises cannot claim refunds even if they paid consumption tax on purchases.

Export-heavy companies should consider the cash flow benefits of filing actual interim returns rather than waiting for the annual return to claim refunds. By filing interim returns showing net refund positions each quarter (or month), companies can accelerate refund recovery throughout the year rather than waiting for a single year-end refund.

Payment Methods

The NTA accepts consumption tax payments through several channels, each with different processing timelines and convenience factors.

- e-Tax electronic payment: Direct debit from the company's bank account via the e-Tax system. Most efficient for companies already using e-Tax for filing.

- Bank transfer: Payment at designated banks using the NTA-issued payment slip (納付書). Payment is reflected on the next business day.

- Credit card payment: Available through the NTA's online payment portal for amounts up to ¥10 million. A processing fee of approximately 0.83% applies.

- Convenience store payment: Available for amounts up to ¥300,000 using a barcode-enabled payment slip.

- QR code payment: Generated through the NTA's QR code creation tool and paid at designated financial institutions.

Large corporations (capital of ¥100 million or more) are required to file consumption tax returns electronically via e-Tax. This e-Tax mandate also applies to corporations that are part of a 100% group with a parent whose capital is ¥100 million or more.

Building a Consumption Tax Compliance Calendar

Foreign companies should maintain a dedicated compliance calendar that tracks consumption tax deadlines alongside other Japanese tax obligations. Key dates for a March 31 fiscal year include:

- May 31: Annual consumption tax return and payment due (no extension available)

- June 30: Corporate income tax return due (if filing extension elected)

- Interim dates: Vary by frequency—semi-annual (November 30), quarterly (August 31, November 30, February 28), or monthly (two months after each month-end)

- Election deadlines: Simplified Tax System election must be filed by the day before the fiscal year starts (March 30 for March FYE companies)

Companies should also track the registration threshold during each fiscal year, as crossing ¥10 million in taxable sales in the current period may trigger obligations for two fiscal years later. A comprehensive view of all Japanese tax deadlines including the full tax calendar helps prevent missed filings and overlapping payment obligations.

Managing consumption tax filing deadlines alongside corporate tax, local tax, and withholding tax obligations requires disciplined calendar management and early preparation. AQ Partners handles consumption tax return preparation, interim payment calculations, and deadline management as part of our back office services for foreign companies in Japan. Contact us at hello@aqpartners.jp.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.