Japan Tax Compliance: Filings, Deadlines & Duties

Key Takeaways

- Tax compliance in Japan is a continuous, year-round process involving monthly, quarterly, and annual obligations — companies must manage payroll withholding remittances every month, consumption tax filings up to four times per year, interim corporate tax payments at the six-month mark, and annual filings for national and local taxes within two months of fiscal year end.

- Record-keeping requirements mandate retention of books and supporting documents for 7 to 10 years — Blue Form filers must retain accounting records for 10 years, while all corporations must keep transaction evidence (invoices, receipts, contracts) for at least 7 years. Since January 2024, the Electronic Books Preservation Act requires electronic transaction data to be stored in its original electronic format (NTA, 2024).

- Provisional (interim) corporate tax payments are required six months into each fiscal year — companies must pay either 50% of the prior year's final tax liability or an amount calculated from actual first-half results. Failure to make interim payments on time triggers delinquency interest at approximately 8.7% per annum (NTA rate for 2025).

- Consumption tax filing frequency depends on prior-year liability: monthly, quarterly, or annually — companies with annual consumption tax liability exceeding 48 million yen must file monthly, those exceeding 4 million yen file quarterly, and others file annually. Each interim period requires its own calculation and payment.

- Statutory audit requirements apply to companies meeting specific size thresholds — Kabushiki Kaisha (KK) entities with stated capital of 500 million yen or more, or total liabilities of 20 billion yen or more, must appoint an independent auditor. According to PwC (2025), companies approaching these thresholds should prepare for audit requirements 12-18 months in advance.

What Does Ongoing Tax Compliance Look Like in Japan?

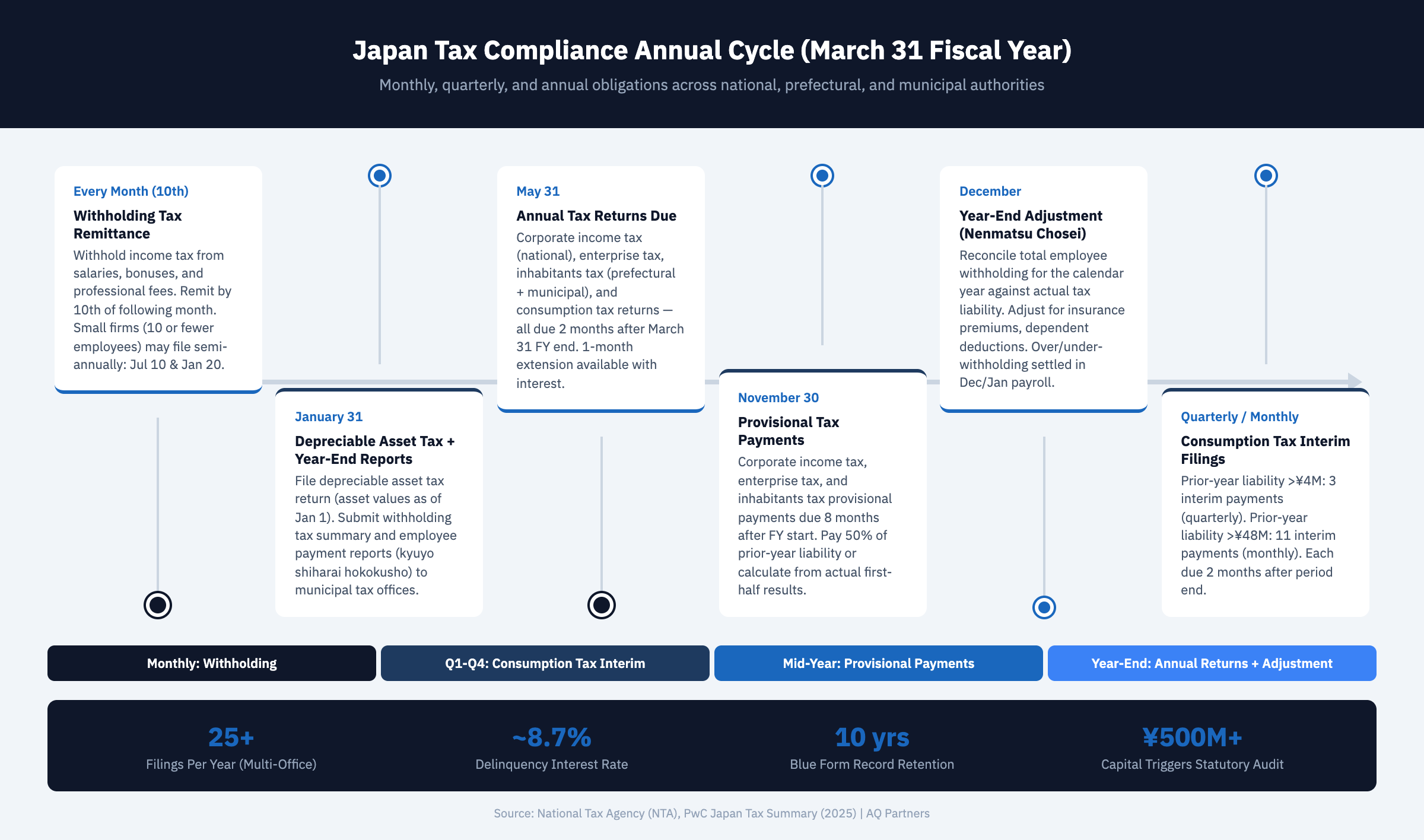

Japan tax compliance responsibilities encompass the full cycle of record-keeping, calculation, filing, and payment obligations that companies must perform on a continuous basis throughout the fiscal year. Unlike jurisdictions where tax compliance is primarily an annual event, Japan's system demands attention every month — from withholding tax remittances and consumption tax interim payments to document retention under evolving electronic storage rules. This guide focuses on the operational reality of maintaining compliance: the day-to-day and month-to-month processes that keep a company in good standing with the National Tax Agency, prefectural tax offices, and municipal authorities.

For a foreign company operating in Japan, the compliance landscape can appear overwhelming. The volume of filings, the number of tax authorities involved, and the specificity of record-keeping requirements exceed what most companies encounter in their home jurisdictions. Understanding these responsibilities as a structured annual cycle — rather than a collection of isolated deadlines — is the key to managing them efficiently. This post complements our Japan tax filing schedule (which lists specific dates) and our tax calendar for foreign companies (which addresses timing for foreign-owned entities) by explaining the substance behind each obligation.

Monthly Obligations: Withholding Tax and Payroll Remittances

Every month, companies in Japan must calculate, withhold, and remit income tax from employee compensation and certain other payments — the remittance deadline is the 10th of the following month.

Withholding tax (gensen choshu) is the most frequent tax compliance obligation in Japan. Each time a company pays salaries, bonuses, director compensation, or fees to certain professionals (attorneys, tax advisors, consultants), it must calculate and withhold the appropriate amount of income tax. The withheld amounts must be deposited with the tax office by the 10th of the month following payment. For example, tax withheld from January salaries paid on January 25 must be remitted by February 10.

The calculation follows NTA-published withholding tax tables that account for the employee's monthly compensation level, number of dependents, and whether they have filed a dependent deduction declaration (fuyo kojo shinkokusho). Companies must also withhold and remit social insurance premiums (health insurance, pension, employment insurance) through a parallel monthly process, though these are administered by different agencies. For more on withholding mechanics, see our complete withholding tax guide.

Small companies with 10 or fewer employees can apply for the 納期の特例 (noki no tokurei) — a semi-annual remittance exception. Under this system, withholding tax for January through June is remitted by July 10, and tax for July through December by January 20. This halves the number of remittance deadlines from 12 to 2, but the company must still calculate withholding correctly each month and maintain complete records.

Quarterly and Interim Obligations: Consumption Tax and Provisional Payments

Companies with significant tax liabilities must make interim consumption tax payments and provisional corporate tax payments during the fiscal year — these are not optional and carry penalties for late payment.

Consumption tax interim payments follow a tiered schedule based on the company's prior-year consumption tax liability. Companies with annual liability between 4 million and 48 million yen must make three interim payments (quarterly), while those exceeding 48 million yen must make eleven interim payments (monthly). Each interim payment equals a proportional fraction of the prior year's liability, though companies may elect to file based on actual results for the interim period if doing so would result in a lower payment. According to the NTA's consumption tax guidance, interim payments are due within two months after each interim period ends.

Provisional corporate income tax payments operate differently. Companies must make a single interim payment six months after the start of the fiscal year. For a company with a March 31 fiscal year end, the provisional payment is due by November 30. The amount is calculated as either 50% of the prior year's final corporate tax liability or the actual tax computed on results for the first six months. Companies expecting significantly lower profits in the current year may benefit from the actual-results method to avoid overpayment.

Enterprise tax and inhabitants tax also require provisional payments on the same six-month schedule as corporate income tax. The mechanics mirror the national tax — either 50% of prior-year liability or actual first-half results. Late payment of any interim obligation triggers delinquency tax (entaizei) at a rate of approximately 8.7% per annum for the first two months and 14.6% thereafter (NTA published rates, 2025).

| Obligation | Frequency | Deadline | Basis for Calculation |

|---|---|---|---|

| Withholding Tax Remittance | Monthly | 10th of following month | NTA withholding tax tables; actual payroll amounts |

| Withholding Tax (Semi-Annual Exception) | Twice yearly | July 10 / January 20 | Aggregated 6-month withholding; 10 or fewer employees |

| Consumption Tax Interim (Quarterly) | 3 times/year | 2 months after interim period | Prior-year liability (4M–48M yen) or actual results |

| Consumption Tax Interim (Monthly) | 11 times/year | 2 months after each month | Prior-year liability (>48M yen) or actual results |

| Provisional Corporate Income Tax | Once/year | 8 months after fiscal year start | 50% of prior-year tax or actual first-half results |

| Provisional Enterprise Tax | Once/year | 8 months after fiscal year start | 50% of prior-year tax or actual first-half results |

| Provisional Inhabitants Tax | Once/year | 8 months after fiscal year start | 50% of prior-year tax or actual first-half results |

| Depreciable Asset Tax Return | Once/year | January 31 | Asset values as of January 1 in each municipality |

| Annual Corporate Tax Return | Once/year | 2 months after fiscal year end | Full fiscal year taxable income |

| Annual Consumption Tax Return | Once/year | 2 months after fiscal year end | Full year output tax minus input tax credits |

| Year-End Adjustment (Nenmatsu Chosei) | Once/year | December (process) / January 31 (reporting) | Reconciliation of employee withholding for calendar year |

Annual Filings: Corporate Tax, Local Tax, and Consumption Tax Returns

The annual corporate tax return is due within two months of the fiscal year end and must be filed with the NTA, prefectural tax office, and municipal tax office — each requires its own set of forms.

The national corporate tax return is the most comprehensive annual filing. It includes the corporation tax return form (beppyo), detailed schedules for income adjustments, depreciation calculations, tax credit claims, and supporting financial statements. The return must be filed in Japanese using NTA-prescribed forms. For a company with a March 31 fiscal year end, the filing deadline is May 31. A one-month extension (to June 30) is available if the company applies in advance and pays interest on any tax due between the original and extended deadlines.

Prefectural and municipal tax returns for enterprise tax and inhabitants tax follow the same two-month deadline. Companies must file separate returns with each prefecture and municipality where they maintain a place of business. A company with offices in Tokyo and Osaka, for example, must file with the Tokyo Metropolitan Government, the applicable Tokyo ward office, the Osaka Prefectural Government, and the Osaka City office — four separate filings in addition to the national return.

The annual consumption tax return is due within two months of the fiscal year end for corporations. This return reconciles all output tax charged on sales against input tax credits claimed on purchases for the full fiscal year, accounting for any interim payments already made. Companies must ensure all claimed input tax credits are supported by qualified invoices from registered suppliers, as required under the Qualified Invoice System introduced in October 2023.

The year-end adjustment (nenmatsu chosei) is an employer-side obligation performed in December each year. Companies must reconcile the total income tax withheld from each employee's compensation during the calendar year against the employee's actual annual tax liability, accounting for insurance premium deductions, dependent deductions, and other credits. Any over- or under-withholding is adjusted in the December or January payroll. The results are reported to the relevant municipal tax offices by January 31 via the withholding tax summary report (gensen choshu hyo) and individual employee payment reports (kyuyo shiharai hokokusho).

Record-Keeping and Document Retention Requirements

Japanese tax law imposes specific retention periods for accounting records, transaction documents, and electronic data — non-compliance can result in loss of Blue Form status and associated tax benefits.

All corporations in Japan must maintain proper books and records (chobo shorui) as the foundation of their tax compliance. The minimum retention period is 7 years for transaction-related documents including invoices, receipts, contracts, delivery slips, and bank statements. Companies that have obtained Blue Form tax return status face an extended retention period of 10 years for accounting books (general ledger, journal, subsidiary ledgers) — a prerequisite for maintaining the loss carryforward and other Blue Form benefits.

Since January 2024, the Electronic Books Preservation Act (denshi chobo hozon ho) requires companies to store electronic transaction data — such as email invoices, PDF receipts, and electronically transmitted contracts — in their original electronic format. Paper printouts of electronic documents are no longer accepted as the primary record. Companies must implement searchable storage systems that allow retrieval by date, counterparty name, and transaction amount. According to PwC's Japan tax administration summary, the NTA has signaled increasing enforcement focus on electronic records compliance during tax audits.

| Document Category | Examples | Retention Period | Key Requirement |

|---|---|---|---|

| Accounting Books (Blue Form) | General ledger, journal, subsidiary ledgers | 10 years | Required for Blue Form status and loss carryforward |

| Accounting Books (Standard) | General ledger, journal | 7 years | Minimum period for all corporations |

| Transaction Evidence | Invoices, receipts, contracts, delivery slips | 7 years | Must support all claimed deductions |

| Qualified Invoices | Invoices with registered number, tax rate, tax amount | 7 years | Required for consumption tax input credits (since Oct 2023) |

| Electronic Transaction Data | Email invoices, PDF receipts, e-contracts | 7 years | Must be stored electronically since Jan 2024 |

| Withholding Tax Records | Employee payment reports, withholding summaries | 7 years | Support for year-end adjustment and employee filings |

| Transfer Pricing Documentation | Local file, master file, CbCR | 7 years | Contemporaneous preparation required for related-party transactions |

| Fixed Asset Registers | Asset acquisition records, depreciation schedules | 7–10 years | Supports depreciation claims and depreciable asset tax filings |

Statutory Audit Triggers and Governance Thresholds

Companies exceeding certain capital or liability thresholds must appoint statutory auditors or independent accounting auditors — triggering additional compliance costs and governance requirements.

Under Japan's Companies Act, a Kabushiki Kaisha (KK) must appoint an independent accounting auditor (kaikei kansanin) if it qualifies as a "large company" — defined as having stated capital of 500 million yen or more, or total liabilities of 20 billion yen or more. Large companies must have their financial statements audited annually by a certified public accountant or audit firm, with the audit report submitted alongside the annual shareholders' meeting materials.

Even below the large-company threshold, KK entities must establish some form of governance structure. Companies with a board of directors typically must appoint at least one statutory auditor (kansayaku) or establish an audit and supervisory committee. The specific requirements depend on the company's organizational structure as chosen under the Companies Act. According to Deloitte's corporate tax guide for Japan, foreign parent companies often underestimate the governance costs associated with growing their Japanese subsidiary past these thresholds.

Goudou Kaisha (GK) entities face simpler governance requirements — they are not required to appoint auditors or hold formal shareholders' meetings. However, if a GK converts to a KK (which some foreign companies do as they scale), it immediately becomes subject to the KK governance framework. For further reading on entity structure implications, see our corporate income tax guide.

The Continuous Nature of Tax Compliance

Tax compliance in Japan is best understood as a continuous operational function rather than a periodic event — companies that treat it as year-end-only will inevitably face penalties and administrative disruption.

The practical reality for a company operating in Japan is that every month brings compliance tasks. January requires depreciable asset tax returns and the second semi-annual withholding remittance. The six-month mark of the fiscal year triggers provisional payment calculations for corporate tax, enterprise tax, and inhabitants tax. Quarterly consumption tax filers have four separate filing and payment cycles. December brings the year-end adjustment process for employee withholding. And within two months of fiscal year end, the annual returns for national corporate tax, consumption tax, enterprise tax, and inhabitants tax must all be completed and filed.

Several factors make Japan's compliance requirements particularly demanding for foreign companies. Tax returns and most supporting documents must be prepared in Japanese. The NTA's e-Tax electronic filing system, while increasingly capable, requires specific Japanese digital certificates for authentication. Transfer pricing documentation must be prepared contemporaneously — meaning at the time of the transaction, not retroactively during audit. And the interaction between national and local filings means that a single error in the national return can cascade into corrections needed across multiple prefectural and municipal filings.

Companies maintaining Blue Form filing status gain significant tax benefits — including loss carryforwards for up to 10 years and higher depreciation limits — but losing that status due to compliance failures is difficult to reverse. The NTA can revoke Blue Form status if a company fails to maintain proper books, misses filing deadlines, or commits significant filing errors. Once revoked, the company loses access to benefits that may represent millions of yen in tax savings.

Frequently Asked Questions

How many tax filings does a Japanese company make per year?

The total number of filings depends on company size and consumption tax liability. At minimum, a standard corporation files an annual corporate tax return (national), annual enterprise tax and inhabitants tax returns (with each relevant prefecture and municipality), an annual consumption tax return, monthly withholding tax remittances (12 per year, or 2 with the semi-annual exception), a depreciable asset tax return, and year-end adjustment reports. A company with offices in two cities and quarterly consumption tax filings could easily have 25 or more filings per year.

What happens if interim tax payments are missed?

Late interim payments trigger delinquency tax (entaizei) at approximately 8.7% per annum for the first two months and 14.6% thereafter, calculated from the original due date. The NTA may also issue demand notices and, in extreme cases, pursue seizure of assets. Repeated late payments can damage the company's compliance record and may affect its ability to obtain filing extensions or maintain Blue Form status.

Are electronic filings mandatory in Japan?

Large corporations (capital of 100 million yen or more) have been required to file corporate tax and consumption tax returns electronically via e-Tax since fiscal years beginning on or after April 1, 2020. Smaller companies may file on paper but are strongly encouraged to use e-Tax. Separately, the Electronic Books Preservation Act (effective January 2024) requires all companies to store electronic transaction data in electronic format — this is a record-keeping requirement, not a filing requirement, but non-compliance can lead to penalties during audit.

How long must tax records be kept?

The standard retention period for transaction-related documents (invoices, receipts, contracts) is 7 years. Companies with Blue Form tax return status must retain accounting books (general ledger, journal, subsidiary ledgers) for 10 years. Since January 2024, electronic transaction data must be stored in its original electronic format for the same retention periods. Companies should implement systematic retention policies that cover both paper and electronic records across all document categories.

Managing Japan's continuous tax compliance obligations requires dedicated expertise and systematic processes. AQ Partners supports foreign companies with end-to-end tax compliance — from monthly withholding calculations through annual filings and audit preparation. Contact us to ensure your Japan tax compliance stays on track year-round.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.