Bookkeeping Requirements for Companies in Japan

Key Takeaways

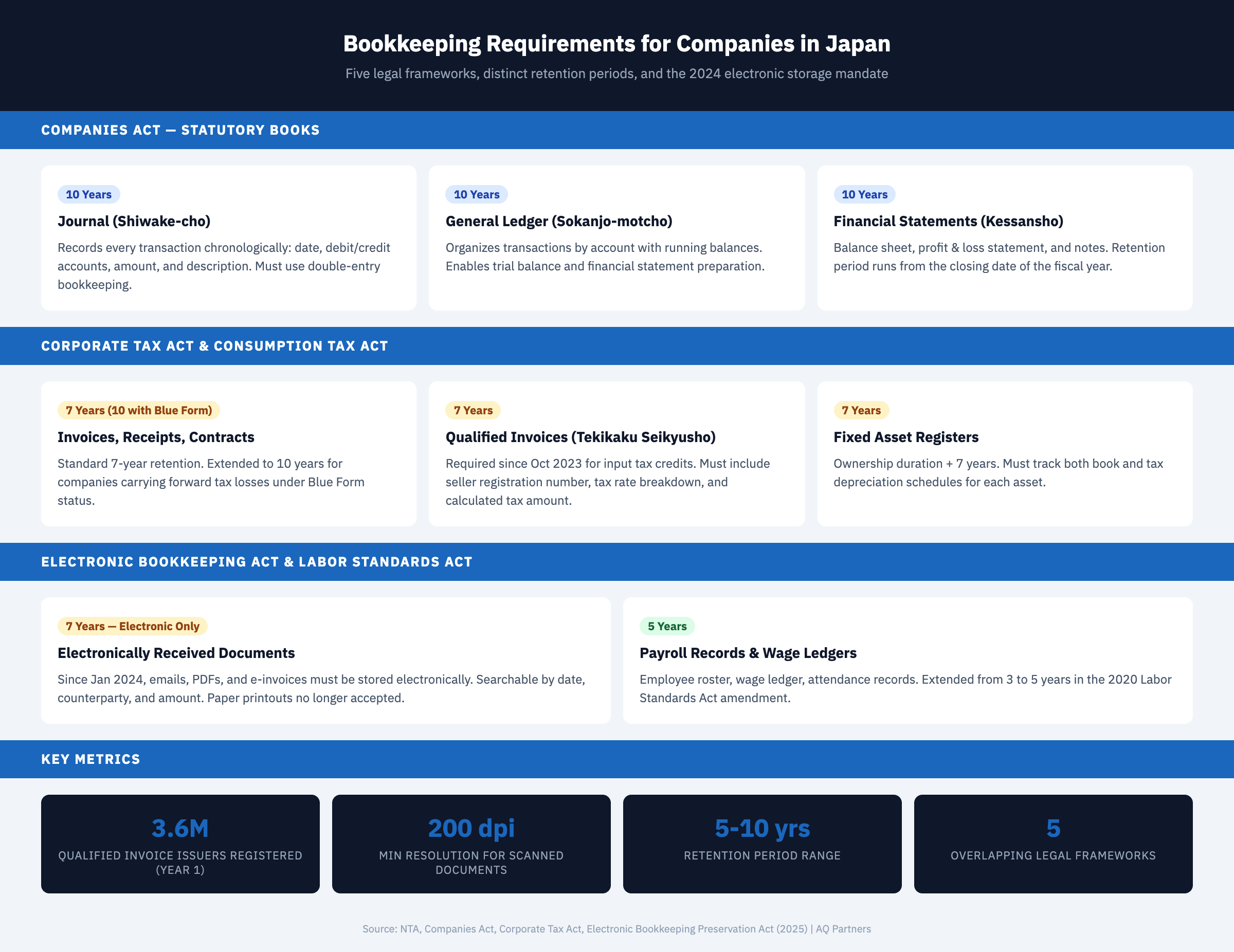

- Japan requires two mandatory statutory books: the journal (shiwake-cho) and general ledger (sokanjo-motcho) — both must be maintained on a double-entry basis under the Companies Act. These are the minimum bookkeeping requirements for any corporation, including foreign subsidiaries, regardless of size or revenue.

- Document retention periods range from 7 to 10 years depending on the document type — the Companies Act mandates 10-year retention for accounting books and financial statements, while the Corporate Tax Act requires 7 years for transaction documents (invoices, receipts, contracts), extended to 10 years for companies carrying forward tax losses under Blue Form status.

- The Electronic Bookkeeping Preservation Act (denshi chobo hozon ho) now requires electronic retention of electronic transactions — since January 2024, all electronically received documents (emails, PDFs, e-invoices) must be stored electronically with searchability by date, counterparty, and amount. Paper printouts are no longer an acceptable alternative for electronic originals.

- The Qualified Invoice System (tekikaku seikyusho) adds per-transaction documentation requirements — since October 2023, claiming consumption tax input credits requires retaining a qualified invoice from a registered issuer. According to the NTA, approximately 3.6 million businesses registered as qualified invoice issuers in the system's first year.

- Blue Form tax filing status depends on meeting minimum bookkeeping standards — companies must maintain organized, double-entry books with proper documentation to retain Blue Form benefits including 10-year loss carryforward and special depreciation allowances worth up to JPY 3 million annually for SMEs.

What Japanese Law Requires Companies to Record and Retain

Bookkeeping requirements in Japan are defined by three overlapping legal frameworks — the Companies Act, the Corporate Tax Act, and the Consumption Tax Act — each specifying what must be recorded, how it must be organized, and how long it must be kept.

For foreign companies operating in Japan, these requirements are not optional guidelines. They are enforceable obligations with direct consequences for non-compliance, ranging from tax penalty assessments to Blue Form status revocation. Understanding exactly what must be recorded, in what format, and for how long is the first step toward building a compliant accounting operation. This post covers the specific requirements — statutory books, document retention periods, electronic storage rules, consumption tax invoice obligations, payroll records, and the bookkeeping standards needed to maintain Blue Form filing status.

Statutory Books: Journal and General Ledger

Every corporation in Japan must maintain two core accounting records — the journal and the general ledger — both prepared using double-entry bookkeeping methods.

The journal (shiwake-cho) records every financial transaction in chronological order. Each journal entry must include the transaction date, the debit and credit accounts affected, the monetary amount, and a brief description. The journal serves as the primary transaction log and the source document for all subsequent accounting records.

The general ledger (sokanjo-motcho) organizes the same transactions by account, providing a running balance for each account in the chart of accounts. The general ledger enables the preparation of trial balances and financial statements. Both the journal and general ledger must be retained for 10 years from the closing date of the fiscal year in which the transactions occurred.

In addition to these two mandatory books, companies typically maintain subsidiary ledgers (hojobo) for accounts receivable, accounts payable, fixed assets, and inventory. While subsidiary ledgers are not explicitly mandated by the Companies Act, they are practically necessary for accurate record-keeping and are expected by tax authorities during audits. The NTA's examination procedures assume that companies can produce detailed breakdowns of major balance sheet accounts on request.

| Document Type | Governing Law | Retention Period | Notes |

|---|---|---|---|

| Journal (shiwake-cho) | Companies Act | 10 years | From closing date of the fiscal year |

| General ledger (sokanjo-motcho) | Companies Act | 10 years | From closing date of the fiscal year |

| Financial statements (kessansho) | Companies Act | 10 years | Balance sheet, P&L, notes |

| Invoices, receipts, contracts | Corporate Tax Act | 7 years | 10 years if carrying forward losses under Blue Form |

| Qualified invoices (tekikaku seikyusho) | Consumption Tax Act | 7 years | Required for input tax credit claims since Oct 2023 |

| Payroll records and wage ledgers | Labor Standards Act | 5 years | Transitional: previously 3 years, extended to 5 in 2020 |

| Electronically received documents | Electronic Bookkeeping Act | 7 years | Must be stored electronically since Jan 2024 |

| Fixed asset registers | Corporate Tax Act | Duration of ownership + 7 years | Must track both book and tax depreciation schedules |

Electronic Bookkeeping Preservation Act: What Changed in 2024

The Electronic Bookkeeping Preservation Act (denshi chobo hozon ho) underwent major reform effective January 2024 — electronic transactions must now be stored electronically, and paper printouts are no longer an acceptable substitute.

Before the 2024 reform, companies could print and file paper copies of electronically received documents (email invoices, PDF contracts, online purchase confirmations). This option was eliminated after a two-year grace period. Companies must now store all electronically received transaction documents in their original electronic format, with the ability to search by date, counterparty name, and amount.

The law specifies two categories of electronic storage. Category 1 covers documents that originated electronically — emails, PDFs, e-invoices, and online platform receipts. These must be retained in their original electronic format with timestamp preservation and searchability. Category 2 covers the optional electronic storage of documents originally created on paper — companies can choose to scan and store paper invoices electronically, but this requires meeting additional standards including resolution requirements (200 dpi minimum) and timestamp verification.

For foreign companies, this reform has practical implications for how they receive and store documents from Japanese vendors, landlords, and service providers. According to the NTA, non-compliance with electronic storage requirements can result in the denial of expense deductions during tax audits, making proper electronic document management a prerequisite for accurate corporate tax filing.

Qualified Invoice System and Consumption Tax Documentation

Since October 2023, claiming consumption tax input credits requires retaining a qualified invoice (tekikaku seikyusho) from a registered issuer — adding a per-transaction documentation requirement to standard bookkeeping obligations.

The Qualified Invoice System requires that every invoice used to claim input tax credits contain specific information: the seller's registered invoice number, the transaction date, a description of goods or services, the amount broken down by tax rate (10% standard and 8% reduced rate), and the consumption tax amount. Invoices that lack any of these elements cannot support input tax credit claims.

For bookkeeping purposes, this means companies must verify the validity of every received invoice against the NTA's registration database, ensure the invoice contains all required elements, and retain the invoice for 7 years. According to NTA data, approximately 3.6 million businesses registered as qualified invoice issuers in the system's first year. Companies transacting with non-registered suppliers cannot claim input tax credits on those purchases, making vendor registration verification a routine part of accounts payable processing.

The bookkeeping system must track consumption tax at the transaction level, distinguishing between standard-rate (10%) and reduced-rate (8%) transactions, exempt transactions, and transactions with non-registered suppliers. This level of detail goes beyond what most foreign companies are accustomed to from VAT/GST systems in other jurisdictions.

Payroll Records and Employment Documentation

Payroll bookkeeping in Japan requires maintaining detailed employee-level records with specific retention periods governed by the Labor Standards Act — separate from but interconnected with general accounting records.

The Labor Standards Act requires employers to maintain three categories of payroll records: the employee roster (rodosha meibo), the wage ledger (chingin dai-cho), and attendance records. Since the 2020 amendment, these records must be retained for 5 years from the date they were created (previously 3 years), though a transitional provision currently applies. The wage ledger must document each employee's base salary, allowances, overtime calculations, social insurance deductions, income tax withholding, and net payment for every pay period.

From an accounting perspective, payroll journal entries must reconcile with these employment records. Social insurance contributions (health insurance, pension, employment insurance) require separate tracking because employer and employee portions are recorded differently and remitted on different schedules. Withholding tax on employee salaries must be calculated, deducted, and remitted to the tax office by the 10th of the following month. Companies with fewer than 10 employees can apply for semi-annual remittance, reducing the frequency to twice per year. Proper coordination between payroll records and the general ledger is essential for both corporate income tax deductions and labor compliance.

Blue Form Bookkeeping Standards

Blue Form (aoiro shinkoku) tax filing status — which unlocks Japan's most valuable tax benefits — requires specific bookkeeping standards that go beyond basic legal minimums.

To qualify for and maintain Blue Form status, a company must maintain accounting books on a double-entry basis, prepare financial statements (balance sheet and income statement) from those books, and retain all supporting documentation in an organized manner. The NTA evaluates Blue Form compliance based on the quality and completeness of bookkeeping — not just whether records exist, but whether they are accurate, current, and accessible.

Key Blue Form requirements include: all transactions recorded promptly (not batched at year-end), accounts organized in a systematic chart of accounts, supporting documents filed and cross-referenced to journal entries, and fixed assets tracked with proper depreciation schedules. Companies that allow bookkeeping to fall behind — recording transactions months late, losing invoices, or maintaining incomplete records — risk Blue Form revocation with consequences that extend far beyond the bookkeeping deficiency itself. The downstream consequences of accounting non-compliance make Blue Form maintenance one of the highest-priority ongoing obligations for any company operating in Japan.

Frequently Asked Questions

Can foreign companies use their global accounting system for Japan bookkeeping?

Global accounting systems can be used, but they must be configured to meet Japan-specific requirements: double-entry bookkeeping, Japan chart of accounts structure, consumption tax tracking at the transaction level, and Japanese-language documentation capability for tax authority interactions. Many foreign companies use Japan-specific accounting software such as freee or Money Forward alongside their global ERP to meet local requirements while feeding consolidated data to headquarters.

What happens if we cannot produce records during an NTA audit?

Inability to produce required records during an NTA audit can result in expense deductions being denied, estimated tax assessments based on the NTA's own calculations (which are typically unfavorable), penalties for non-compliance with retention requirements, and potential Blue Form revocation. The NTA expects companies to produce supporting documents for any transaction within the retention period within a reasonable timeframe during an examination.

Do branch offices have the same bookkeeping requirements as subsidiaries?

Yes. Branch offices of foreign companies operating in Japan are subject to the same bookkeeping and retention requirements under the Corporate Tax Act and Consumption Tax Act. While branches may follow the parent company's accounting policies for internal purposes, Japan-source income must be calculated and documented according to Japanese tax rules, and all Japan-related transaction documents must be retained for the prescribed periods.

Meeting Japan's bookkeeping requirements requires Japan-specific systems, processes, and expertise. AQ Partners provides comprehensive bookkeeping services designed to meet every statutory requirement while integrating with your global reporting framework. Contact us to ensure your Japan bookkeeping is fully compliant.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.