Back Office in Japan: The Complete Operations Guide

Key Takeaways

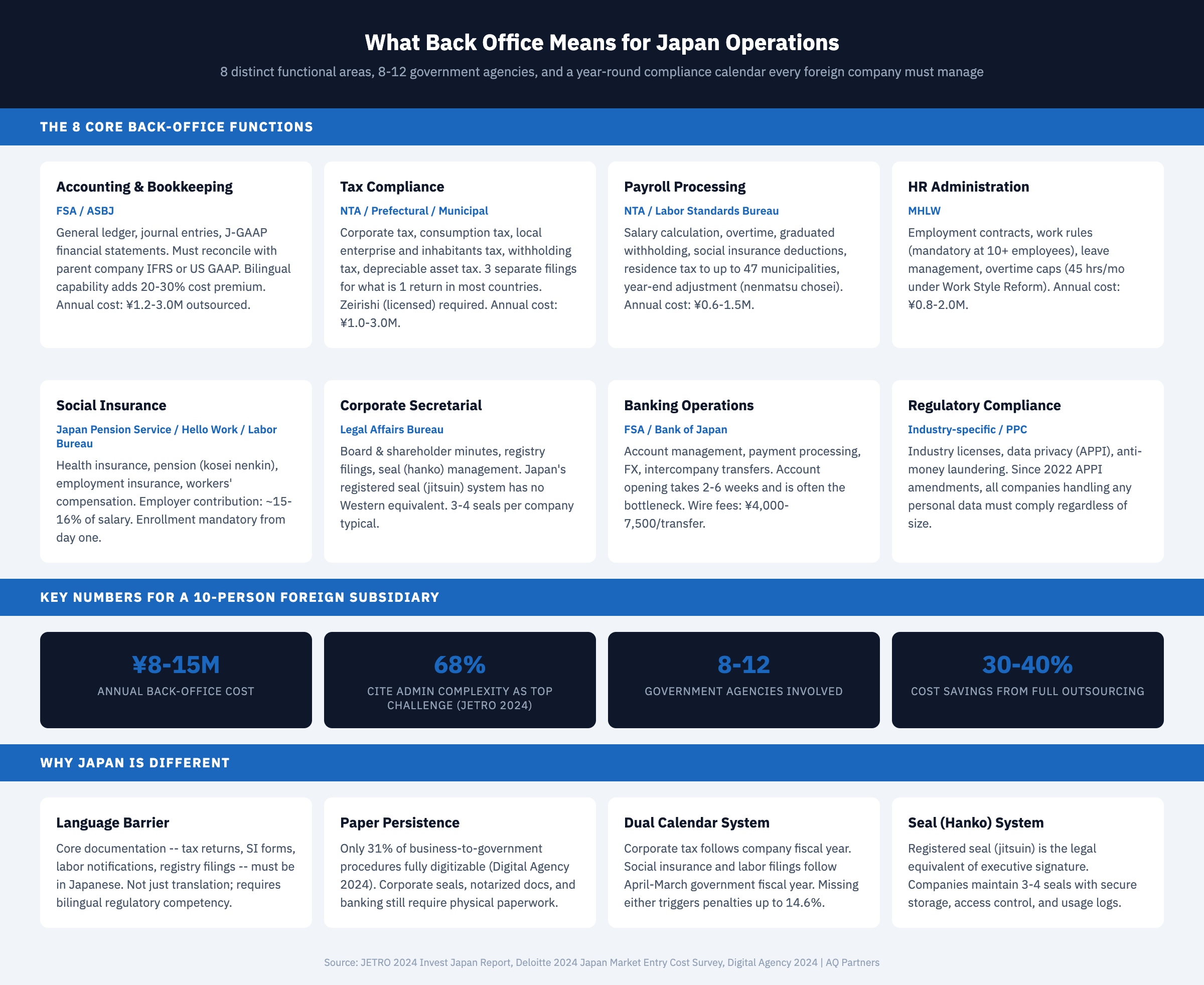

- Back office in Japan encompasses far more functions than in most Western markets — beyond accounting and HR, it includes mandatory statutory filings with up to 12 government agencies, hanko seal management, social insurance administration, and Japanese-language document compliance. According to JETRO's 2024 Invest Japan report, 68% of foreign companies cite back-office complexity as their top operational challenge.

- Japan's back office runs on a dual-calendar compliance system — corporate tax follows the company's chosen fiscal year, while social insurance and labor filings follow the April-to-March government fiscal year. Missing either calendar's deadlines triggers penalties ranging from 10% surcharges on late tax filings to criminal liability for labor standards violations.

- Paper-based and in-person processes persist despite digitization efforts — the Digital Agency's 2024 survey found that only 31% of business-to-government procedures were fully digitizable. Corporate bank account opening, certain tax filings, and labor inspector interactions still require physical presence or wet-ink documents.

- A typical foreign subsidiary in Japan needs 5-8 specialized back-office functions operating simultaneously — accounting, tax coordination, payroll, HR administration, social insurance, corporate secretarial, banking operations, and regulatory compliance. Each function requires Japanese-language capability and specific regulatory knowledge.

- Annual back-office operating costs for a 10-person subsidiary range from ¥8-15 million — according to Deloitte's 2024 Japan Market Entry Cost Survey, this includes accounting fees, tax advisory, payroll processing, social insurance administration, and corporate secretarial services. Outsourcing typically reduces this by 30-40% compared to fully in-house staffing.

What "Back Office" Means in the Japanese Business Context

Back office in Japan refers to the full spectrum of administrative, financial, regulatory, and compliance functions required to legally operate a company — spanning accounting, tax, payroll, HR, social insurance, corporate governance, and government reporting obligations that are substantially more complex than comparable functions in most other developed markets.

For foreign companies entering Japan, the term "back office" carries weight that it simply does not in markets like the United States, the United Kingdom, or Singapore. In those jurisdictions, back-office operations are often lightweight, digitized, and can be managed with a small team or a single software platform. Japan is different. The combination of Japanese-language regulatory requirements, paper-based government interactions, a distinctive fiscal calendar structure, and industry-specific compliance layers means that back-office operations in Japan demand specialized knowledge, dedicated resources, and constant attention.

The Japan External Trade Organization (JETRO) regularly surveys foreign-affiliated companies operating in Japan. Their 2024 survey on business conditions found that 68% of respondents identified administrative and regulatory complexity as their primary operational challenge — ahead of talent acquisition, language barriers, and market competition. This statistic reflects a reality that many foreign executives only discover after incorporation: the back office in Japan is not a support function to be minimized. It is a core operational requirement that directly impacts a company's ability to remain compliant, pay employees correctly, file taxes on time, and maintain its corporate standing.

This guide breaks down every component of Japan's back-office landscape, explains why each function matters, and provides the practical framework foreign companies need to plan their operational infrastructure. Whether you are evaluating a Kabushiki Kaisha, Goudou Kaisha, or branch office structure, understanding the full scope of back-office requirements is essential to making informed decisions about staffing, budgeting, and operational strategy.

Core Back-Office Functions: The Complete Operational Map

Japan's back office comprises 8 distinct functional areas, each governed by separate regulatory frameworks and requiring specific expertise — no single generalist can cover all of them competently.

Understanding what each function entails helps foreign companies avoid the common mistake of under-resourcing their Japan operations. Below is the complete operational map of back-office functions that every company operating in Japan must address.

| Function | What It Covers | Governing Authority | Frequency |

|---|---|---|---|

| Accounting & Bookkeeping | General ledger, journal entries, financial statements, J-GAAP or IFRS compliance | Financial Services Agency (FSA), ASBJ | Daily / Monthly / Annual |

| Tax Compliance | Corporate tax, consumption tax, local taxes, withholding tax, depreciable asset tax | National Tax Agency (NTA), Prefectural/Municipal Tax Offices | Monthly / Quarterly / Annual |

| Payroll Processing | Salary calculation, overtime, tax withholding, year-end adjustment (nenmatsu chosei) | NTA, Labor Standards Bureau | Monthly / Semi-annual / Annual |

| HR Administration | Employment contracts, work rules, leave management, labor dispute handling | Ministry of Health, Labour and Welfare (MHLW) | Ongoing / Annual |

| Social Insurance | Health insurance, pension (kosei nenkin), employment insurance, workers' compensation | Japan Pension Service, Hello Work, Labor Bureau | Monthly / Annual |

| Corporate Secretarial | Board minutes, shareholder meetings, registry filings, seal (hanko) management | Legal Affairs Bureau (Houmukyoku) | As needed / Annual |

| Banking Operations | Account management, payment processing, foreign exchange, intercompany transfers | Financial Services Agency (FSA), Bank of Japan | Daily / Monthly |

| Regulatory Compliance | Industry licenses, data privacy (APPI), anti-money laundering, annual reporting | Industry-specific regulators, PPC | Ongoing / Annual |

Accounting and bookkeeping in Japan requires maintaining books in Japanese using the Japanese chart of accounts structure. Foreign subsidiaries must reconcile between their parent company's reporting framework (typically IFRS or US GAAP) and Japanese Generally Accepted Accounting Principles (J-GAAP). The differences between Japanese and international accounting standards affect everything from revenue recognition to lease accounting, creating parallel workstreams that do not exist in single-framework jurisdictions.

Tax compliance in Japan involves filing with multiple authorities at national, prefectural, and municipal levels. A single corporate entity files corporate income tax with the NTA, enterprise tax and inhabitants tax with the prefectural tax office, and inhabitants tax with the municipal tax office — three separate filings for what would be a single return in many countries. The corporate tax filing and compliance process requires coordination between accountants and licensed tax accountants (zeirishi), as only licensed professionals can sign and submit tax returns in Japan.

Payroll processing extends well beyond salary calculation. Japanese payroll requires computing graduated income tax withholding, social insurance premium deductions (employer and employee portions), residence tax collection and remittance to municipalities, and the year-end adjustment (nenmatsu chosei) — an employer-administered tax reconciliation that replaces individual tax returns for most employees. According to PwC's Japan individual tax summary, employers must calculate and remit withholdings to up to 47 different municipal governments depending on where employees reside.

HR administration under Japanese labor law is notably employee-protective. The Labor Standards Act, Labor Contract Act, and related legislation create obligations around working hours, overtime management, paid leave accrual, and termination procedures that are substantially more rigid than those in at-will employment jurisdictions. Companies with 10 or more employees must file work rules (shugyo kisoku) with the Labor Standards Inspection Office. For foreign companies building teams in Japan, understanding HR compliance strategies for global teams is critical to avoiding costly labor disputes.

Social insurance enrollment is mandatory from the first employee. Japan's social insurance system comprises four programs: health insurance (kenko hoken), employees' pension (kosei nenkin hoken), employment insurance (koyo hoken), and workers' compensation insurance (rosai hoken). The employer's combined contribution for health insurance and pension alone runs approximately 15-16% of each employee's salary, according to the Japan Pension Service. Enrollment, premium calculation, and annual standard remuneration reviews all require filings with the Japan Pension Service and Hello Work offices.

Corporate secretarial work includes maintaining the company's registered information at the Legal Affairs Bureau, managing corporate seals (hanko), preparing board and shareholder meeting minutes, and filing any changes to directors, capital, or registered address. Japan's corporate seal system — where the registered seal (jitsuin) serves as the legal equivalent of an executive signature — adds a layer of physical document management that has no parallel in most Western jurisdictions.

The Japanese Compliance Calendar: A Year-Round Obligation

Japan's back-office compliance calendar operates on two overlapping cycles — the company's fiscal year for tax purposes and the government's April-to-March fiscal year for labor and social insurance filings — creating a continuous stream of deadlines throughout the year.

Foreign companies accustomed to a handful of annual filing deadlines are often unprepared for the volume and frequency of Japanese compliance obligations. A company with a March fiscal year-end faces its most intense period between April and June, when corporate tax returns, consumption tax returns, local tax filings, social insurance annual updates, and labor insurance annual declarations all converge.

| Month | Obligation | Authority | Penalty for Non-Compliance |

|---|---|---|---|

| January | Depreciable asset tax return; withholding tax summary (gensen choshu-hyo) | Municipal tax office; NTA | 10% surcharge on underpaid amounts |

| March | Corporate tax interim return (if applicable); consumption tax annual return | NTA | 14.6% delinquency tax after 2 months |

| May | Corporate tax final return (March FY-end); local tax returns | NTA; Prefectural/Municipal offices | 10-15% additional tax + interest |

| June | Residence tax special collection amount notification; new FY rates take effect | Municipal tax offices | Payroll errors if rates not updated |

| July | Social insurance standard remuneration review (santei kiso todoke); labor insurance annual declaration | Japan Pension Service; Labor Bureau | Incorrect premium calculations; penalties |

| September | New social insurance premium rates take effect (from July review) | Japan Pension Service | Incorrect payroll deductions |

| November | Year-end adjustment preparation begins (nenmatsu chosei) | NTA | Employee tax under/overpayment issues |

| December | Year-end adjustment completion; final payroll of the year | NTA | Incorrect final withholding amounts |

| Monthly | Withholding tax remittance; social insurance premium payments; payroll processing | NTA; Japan Pension Service | 10% surcharge on late remittance |

The critical point that foreign companies must understand is that these deadlines are not flexible. Japan's NTA imposes a 10% additional tax on late-filed corporate tax returns, escalating to 15% for returns more than 50 days late. Delinquency tax accrues at approximately 2.4% for the first two months and 8.7% thereafter (FY2024 rates). These penalties apply automatically — there is no informal grace period or relationship-based leniency that foreign companies sometimes expect based on experience in other Asian markets.

The social insurance calendar adds another layer. Every July, employers must review each employee's standard monthly remuneration — the basis for premium calculations — by comparing actual compensation paid during April through June against the standard remuneration grades published by the Japan Pension Service. Updated premiums take effect in September. Failing to perform this annual review results in incorrect premium payments, which the Japan Pension Service will rectify with retroactive adjustments and potential penalties.

Why Japan's Back Office Is Different from Other Markets

Japan's back-office complexity stems from five structural factors that distinguish it from comparable developed economies — language requirements, paper-based processes, multi-agency oversight, the seal system, and employment law rigidity.

Language as a compliance barrier: Most government forms, official correspondence, and regulatory submissions must be in Japanese. While the NTA has introduced English-language guides and some e-filing systems accept romaji input, the core documentation — tax returns, social insurance forms, labor notifications, and corporate registry filings — must be submitted in Japanese. This is not merely a translation issue. Japanese accounting terminology, legal concepts, and bureaucratic conventions do not map directly to English equivalents, requiring personnel with genuine bilingual competency in both language and regulatory context.

Paper persistence: Japan's government has made significant strides in digitization through the Digital Agency (established September 2021), yet paper-based processes remain embedded in daily operations. The Digital Agency's 2024 progress report acknowledged that only 31% of business-to-government procedures could be completed entirely online. Corporate seal certificates, certain notarized documents, and specific banking operations still require physical paperwork. Foreign companies accustomed to fully digital back-office workflows must budget for this paper-handling reality.

Multi-agency oversight: A single company interacts with multiple government entities for different back-office functions. The NTA handles national tax matters. Prefectural and municipal tax offices manage local taxes independently. The Japan Pension Service oversees health insurance and pension. Hello Work (Public Employment Security Office) administers employment insurance. The Labor Standards Inspection Office enforces working conditions. The Legal Affairs Bureau maintains corporate registries. Each agency has its own filing systems, deadlines, forms, and — in many cases — its own physical offices that must be visited in person.

The seal (hanko) system: Japan's corporate seal system requires companies to register an official seal (jitsuin) with the Legal Affairs Bureau. This registered seal — not an executive's signature — serves as the primary method of authenticating corporate decisions, contracts, and government filings. Companies typically maintain three to four seals: the registered seal (jitsuin) for the most important documents, a banking seal (ginko-in) for financial transactions, a company seal (kaisha-in) for routine correspondence, and individual employee seals for internal approvals. Managing these physical artifacts — secure storage, access control, usage logs — constitutes a back-office function with no equivalent in most Western operations.

Employment law rigidity: Japan's labor protections make personnel management a significant back-office burden. Termination of employees requires "objectively reasonable grounds" and must be "socially acceptable" — vague standards that courts have interpreted very favorably for employees. According to the Ministry of Health, Labour and Welfare, companies must maintain detailed records of working hours, overtime, paid leave usage, and health check compliance for each employee. The 2019 Work Style Reform Act introduced overtime caps of 45 hours per month and 360 hours per year (with exceptions), requiring employers to track and enforce these limits through their payroll and attendance systems. Understanding labor compliance risks in Japan is essential for any company with employees.

Back-Office Costs: What Foreign Companies Should Budget

Annual back-office costs for a foreign subsidiary in Japan typically range from ¥8 million to ¥15 million for a 10-person company — driven by professional service fees, software subscriptions, and the administrative overhead unique to the Japanese regulatory environment.

Cost planning for Japan's back office requires granularity that foreign companies often underestimate. Below is a realistic cost breakdown based on market rates for professional services serving foreign-affiliated companies in Japan.

| Back-Office Function | Annual Cost Range (¥) | Outsourced vs In-House | Notes |

|---|---|---|---|

| Accounting & Bookkeeping | ¥1.2M - ¥3.0M | Outsourced: ¥1.2-2.0M; In-house: ¥4-6M (full-time accountant salary) | Bilingual capability adds 20-30% premium |

| Tax Filing & Advisory | ¥1.0M - ¥3.0M | Always outsourced (zeirishi license required) | Increases with revenue and transaction complexity |

| Payroll Processing | ¥0.6M - ¥1.5M | Outsourced: ¥5,000-10,000/employee/month | Includes year-end adjustment processing |

| Social Insurance Admin | ¥0.5M - ¥1.2M | Often bundled with payroll or HR outsourcing | Sharoushi (labor consultant) may be needed |

| HR Administration | ¥0.8M - ¥2.0M | Outsourced: ¥0.8-1.5M; In-house: ¥5-7M (HR manager salary) | Work rules drafting is a one-time cost of ¥200-500K |

| Corporate Secretarial | ¥0.3M - ¥0.8M | Outsourced: ¥0.3-0.5M; scales with changes filed | Director changes, address changes add ¥50-100K each |

| Software & Systems | ¥0.3M - ¥1.0M | Cloud accounting (freee, MoneyForward) + payroll software | Japanese-language platforms dominate |

| Banking & FX | ¥0.1M - ¥0.5M | Bank fees + wire transfer costs | International wire fees of ¥4,000-7,500 per transfer |

| Total (10-person company) | ¥4.8M - ¥13.0M | Fully outsourced model saves 30-40% | Excludes one-time incorporation costs |

Deloitte's 2024 Japan Market Entry Cost Survey found that total back-office costs for a 10-person subsidiary averaged ¥11.2 million annually when using a combination of outsourced and in-house resources. Companies that fully outsource their back office to integrated service providers typically reduce this to ¥7-9 million — a 30-40% reduction driven primarily by eliminating the need for full-time bilingual administrative staff whose salaries in Tokyo average ¥5-7 million per year.

The decision between outsourcing and in-house back-office operations depends on company size, growth trajectory, and the availability of bilingual talent — but for companies under 30 employees, the outsourcing model is almost universally more cost-effective.

One frequently overlooked cost driver is the corporate bank account opening process. Japanese banks require extensive documentation, in-person interviews (sometimes multiple rounds), and a physical office address. The process typically takes 2-6 weeks and may require a Japanese-speaking representative to navigate the bank's requirements. Companies unable to open a bank account cannot pay employees, remit taxes, or process invoices — making banking operations a gating factor for the entire back office.

How Back-Office Complexity Scales with Growth

Back-office complexity in Japan does not increase linearly with headcount — it escalates at specific thresholds tied to employee count, revenue, and entity structure, creating step-function jumps in administrative burden.

Understanding these thresholds allows foreign companies to plan ahead rather than react to sudden compliance increases. The relationship between back-office complexity, speed, and cost becomes increasingly important as companies grow beyond their initial setup phase.

1-9 employees: The base compliance level. Requires standard social insurance enrollment, payroll processing, and tax filings. Work rules are optional but recommended. A single outsourced provider can typically handle all back-office functions.

10-49 employees: Mandatory work rules filing triggers at 10 employees. Stress check obligations begin at 50 employees (under the Industrial Safety and Health Act). The volume of payroll processing, social insurance notifications, and residence tax administration grows proportionally. Most companies at this stage need dedicated payroll software rather than spreadsheet-based processing.

50-99 employees: Significant new obligations emerge. Companies must appoint a health manager (eisei kanrisha), conduct annual stress checks for all employees, and submit detailed working-hour reports. The MHLW's labor standards framework imposes additional reporting requirements at this threshold. The back-office team or outsourced provider needs labor law expertise beyond basic administration.

100+ employees: Additional health and safety committee requirements apply. Companies become subject to enhanced corporate governance expectations if publicly listed. Transfer pricing documentation obligations increase for companies with cross-border intercompany transactions exceeding specific thresholds. The back office at this scale typically requires a mix of in-house coordination staff and specialized external providers.

Revenue thresholds also trigger compliance changes independently of headcount. Companies whose taxable sales exceed ¥10 million become consumption tax payers, adding quarterly or monthly filing obligations. Companies with capital exceeding ¥100 million lose access to SME tax benefits including the reduced corporate tax rate on the first ¥8 million of income, various small business deductions, and the simplified consumption tax calculation method.

Getting Your Japan Back Office Right from Day One

The most cost-effective approach to Japan's back office is to set it up correctly during initial market entry — retrofitting compliance after the fact is invariably more expensive and disruptive than building the right infrastructure from the start.

Companies entering Japan face an immediate sequence of back-office decisions that cascade from the entity structuring choice. A Kabushiki Kaisha (KK) has different governance and reporting requirements than a Goudou Kaisha (GK) or a branch office. These structural decisions determine which back-office functions are required, how they must be organized, and what professional service relationships are needed.

The critical first 90 days after incorporation involve establishing the following back-office foundations:

- Tax registrations — Notifications to the NTA, prefectural tax office, and municipal tax office must be filed within specific deadlines after incorporation. Blue Form tax filing status — which unlocks significant tax benefits including loss carryforward — requires a separate application within the first fiscal year.

- Social insurance setup — Health insurance and pension enrollment with the Japan Pension Service, plus employment insurance and workers' compensation registration at Hello Work, must be completed before the first employee starts.

- Banking operations — Corporate bank account opening should begin immediately upon incorporation, as processing times of 2-6 weeks can delay the entire operational launch.

- Accounting system deployment — Selecting and configuring a Japanese-compatible accounting platform that supports both J-GAAP reporting and parent company consolidation requirements.

- Payroll infrastructure — Setting up payroll calculation, withholding tax tables, social insurance premium rates, and residence tax collection mechanisms before the first salary payment.

- Work rules and employment contracts — Drafting Japanese-compliant employment agreements and, for companies expecting to reach 10 employees, preparing work rules for filing with the Labor Standards Inspection Office.

For companies evaluating whether to handle these functions in-house, through an EOR arrangement, or with an outsourced provider, the decision depends on long-term Japan strategy, budget constraints, and the availability of bilingual staff who understand Japanese regulatory requirements.

Common Mistakes Foreign Companies Make with Japan Back Office

Foreign companies consistently make five predictable mistakes with their Japan back office — each one stems from applying assumptions formed in less regulated markets to Japan's distinctive administrative environment.

Mistake 1: Treating back office as a cost to minimize rather than infrastructure to invest in. Companies that underfund their Japan back office inevitably encounter compliance failures. Tax filing errors trigger NTA audits. Payroll mistakes create employee disputes. Social insurance lapses generate retroactive premium demands with interest. The cost of remediation always exceeds the cost of proper setup. According to a 2023 survey by the Japan Association of Corporate Directors, compliance failures cost foreign-affiliated companies an average of ¥3.2 million in penalties and professional fees per incident.

Mistake 2: Assuming headquarters' back-office systems work in Japan. Global ERP systems, payroll platforms, and accounting software rarely accommodate Japan's specific requirements out of the box. Japanese payroll requires calculating commuting allowance tax exclusions, social insurance grade-based premiums, and the year-end adjustment — none of which standard Western payroll software handles natively. Companies that try to force headquarters systems onto their Japan operations create manual workaround processes that are error-prone and unsustainable.

Mistake 3: Hiring a single "Japan admin" to handle everything. No single individual can competently manage accounting, tax coordination, payroll, HR compliance, social insurance, and corporate secretarial functions simultaneously. Tax filing requires a licensed zeirishi. Social insurance advisory work requires a licensed sharoushi (certified social insurance and labor consultant). Trying to consolidate all back-office functions into one generalist role creates compliance risk and burnout.

Mistake 4: Ignoring the compliance calendar until deadlines approach. Japan's overlapping compliance calendars require advance planning. The year-end adjustment process begins with employee data collection in November and concludes with withholding tax summary submission in January. Social insurance annual reviews require April-June payroll data compiled and submitted in July. Companies that treat each deadline as a standalone event rather than part of an integrated calendar inevitably miss filings or submit inaccurate information.

Mistake 5: Delaying back-office setup during incorporation. Some companies incorporate their Japan entity and then begin searching for back-office service providers after the fact. This approach creates a dangerous gap period where tax registration deadlines pass, social insurance enrollment windows close, and early transactions go unrecorded. By the time professional support is engaged, the company faces retroactive filings, potential penalties, and a disorganized financial record that takes months to reconstruct.

Frequently Asked Questions

What back-office functions are legally required for a company in Japan?

Every company operating in Japan must maintain proper accounting books (per the Companies Act), file corporate tax returns (national, prefectural, and municipal), process payroll with correct withholding calculations, enroll employees in social insurance (health, pension, employment, workers' compensation), and maintain corporate registry filings with the Legal Affairs Bureau. Companies with 10 or more employees must also file work rules with the Labor Standards Inspection Office. Failure to fulfill any of these functions carries specific statutory penalties.

How many government agencies does a Japan subsidiary interact with?

A typical Japan subsidiary interacts with 8-12 government agencies on a regular basis: the National Tax Agency, prefectural tax office, municipal tax office, Japan Pension Service, Hello Work (employment insurance), Labor Standards Inspection Office, Labor Bureau (workers' compensation), Legal Affairs Bureau, and potentially industry-specific regulators. Each agency maintains separate filing systems, deadlines, and communication channels, many of which operate primarily in Japanese.

Can a foreign company manage Japan's back office remotely from overseas?

Partial remote management is possible but full remote administration is impractical. While accounting, payroll calculations, and some tax coordination can be performed remotely, many functions require physical presence in Japan — corporate bank account operations, seal management, Labor Standards Inspection Office interactions, and certain government filings. Companies attempting fully remote back-office management typically engage a local representative or outsourced provider for on-the-ground functions.

What is the year-end adjustment (nenmatsu chosei) and why does it matter?

The year-end adjustment is an employer-administered process that reconciles each employee's income tax withholdings for the calendar year against their actual tax liability. Unlike many countries where individuals file their own tax returns, in Japan the employer calculates the final tax, accounts for deductions (insurance premiums, dependents, mortgage interest), and either refunds overpayments or collects underpayments through December or January payroll. This process eliminates the need for individual tax returns for most salaried employees and is mandatory for all employers.

How long does it take to set up a fully functional back office in Japan?

Setting up a fully functional back office typically takes 60-90 days from the date of incorporation. This includes corporate bank account opening (2-6 weeks), tax registrations (1-2 weeks), social insurance enrollment (1-2 weeks), accounting system setup (1-2 weeks), and payroll infrastructure configuration (1-2 weeks). Some of these processes run in parallel, but the bank account opening typically determines the overall timeline because many other functions depend on having an operational bank account.

Japan's back office demands more planning, more expertise, and more ongoing attention than most foreign companies expect. The good news is that with the right infrastructure and professional support, it operates predictably and efficiently. AQ Partners provides integrated back-office services — accounting, tax coordination, payroll, HR administration, and corporate secretarial — designed specifically for foreign companies operating in Japan. Contact us for a consultation to discuss how we can build or streamline your Japan back-office operations.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.