Outsourcing vs In-House Back Office in Japan

Key Takeaways

- Outsourcing back-office functions saves foreign companies 30-40% compared to in-house staffing in Japan — Deloitte's 2024 Japan Market Entry Cost Survey found that fully outsourced back-office operations for a 10-person subsidiary cost ¥7-9 million annually versus ¥11-15 million for an equivalent in-house setup, primarily because outsourcing eliminates the need for full-time bilingual administrative hires at Tokyo salary levels.

- Tax filing and social insurance advisory cannot legally be handled in-house without licensed professionals — Japan requires a licensed zeirishi (tax accountant) to prepare and sign corporate tax returns, and complex social insurance matters often require a certified sharoushi (social insurance and labor consultant). These licensing requirements make some degree of outsourcing mandatory for every company.

- Companies under 30 employees almost universally benefit from full outsourcing — the administrative volume at this scale does not justify the cost of dedicated back-office hires, and outsourced providers offer access to multi-specialist teams (accountants, tax advisors, labor consultants) that no single hire can replicate.

- The hybrid model — outsourced specialists plus one in-house coordinator — delivers the best balance for growing companies — according to a 2023 EY Japan survey, 62% of foreign-affiliated companies with 30-100 employees use this approach, outsourcing tax, payroll, and social insurance while keeping a bilingual administrative coordinator in-house for daily operations.

- Switching from in-house to outsourced is significantly harder than starting outsourced — companies that build in-house back-office teams first face knowledge transfer challenges, data migration costs, and organizational resistance when later transitioning to outsourced providers. Starting with an outsourced model and selectively insourcing as the company grows is the lower-risk path.

The Core Decision: Outsource, In-House, or Hybrid

The outsourcing decision for Japan back-office operations comes down to three models — full outsourcing, full in-house, or a hybrid approach — each suited to different company sizes, growth stages, and strategic priorities.

Foreign companies entering Japan face this decision early, often within weeks of incorporation. The choice has long-term implications for cost structure, compliance reliability, operational agility, and the company's ability to scale. Unlike markets where back-office functions can be incrementally built with generalist hires, Japan's regulatory complexity means that the wrong model creates compounding problems — missed filings, incorrect payroll calculations, and compliance gaps that are expensive to remediate. As JETRO's guide to setting up business in Japan details, the multi-agency registration and reporting requirements make professional back-office support especially important for foreign entrants.

Understanding what back office actually means in the Japan context is an essential prerequisite to making this decision. Japan's back office encompasses 8 distinct functional areas — accounting, tax, payroll, HR, social insurance, corporate secretarial, banking, and regulatory compliance — each governed by separate authorities with separate requirements. The outsourcing question must be answered for each function individually, not as a blanket yes-or-no decision.

What Full Outsourcing Looks Like in Practice

Full outsourcing means engaging an external provider or coordinated set of providers to handle all back-office functions — the company retains no dedicated administrative staff in Japan beyond its core business team.

In this model, the outsourced provider manages monthly bookkeeping, prepares financial statements, coordinates with a licensed zeirishi for tax filings, processes payroll including year-end adjustments, handles social insurance enrollments and annual reviews, maintains corporate registry filings, and manages banking operations on behalf of the company.

The primary advantage is cost efficiency. A full-time bilingual accountant in Tokyo commands a salary of ¥5-7 million per year, according to Robert Half Japan's 2024 Salary Guide. Add a bilingual HR/admin generalist at ¥4-6 million, and the company is spending ¥9-13 million on salaries alone before accounting for office space, software licenses, training, and benefits (employer social insurance contributions of approximately 15-16% per employee). An outsourced provider delivering equivalent functions typically charges ¥5-8 million annually for a company with 10-15 employees.

Full outsourcing is most effective for:

- Early-stage subsidiaries with fewer than 15 employees and predictable back-office volumes

- Branch offices with limited Japan-based decision-making authority and centralized headquarters control

- Companies testing the Japan market that want to minimize fixed costs during their initial 1-3 years

- Remote-first companies with no physical Japan office but with employees or contractors in Japan

The main risk of full outsourcing is reduced control over day-to-day operations and potential communication latency. When an employee has a payroll question or a vendor needs immediate payment processing, the response time depends on the provider's service model. Companies with high-frequency transactional needs or complex intercompany arrangements may find this friction unacceptable.

When In-House Back Office Makes Sense

In-house back-office staffing becomes justifiable when a company reaches 50+ employees, generates complex transactions requiring daily oversight, or operates in a regulated industry with continuous compliance monitoring needs.

Building an in-house back-office team in Japan requires hiring across multiple specializations. A single generalist cannot competently manage accounting, payroll, HR compliance, and social insurance — each function requires specific training and, in some cases, professional licensing. A realistic in-house back-office team for a 50-100 person subsidiary includes:

| Role | Annual Salary Range (¥) | Responsibilities | Required Qualifications |

|---|---|---|---|

| Finance Manager | ¥8M - ¥12M | Accounting oversight, financial reporting, HQ liaison | Bilingual, J-GAAP + IFRS experience |

| Staff Accountant | ¥4M - ¥6M | Daily bookkeeping, journal entries, AP/AR | Japanese, accounting certification preferred |

| HR/Admin Manager | ¥6M - ¥9M | Payroll oversight, HR compliance, labor relations | Bilingual, labor law knowledge |

| Admin Assistant | ¥3M - ¥4.5M | Office management, document handling, seal administration | Japanese, basic office skills |

| External Zeirishi (Tax) | ¥1.5M - ¥3M | Tax return preparation, tax advisory | Licensed zeirishi (mandatory) |

| External Sharoushi (Labor) | ¥0.5M - ¥1.2M | Social insurance filings, labor advisory | Licensed sharoushi (recommended) |

| Total Annual Cost | ¥23M - ¥35.7M | Before employer SI contributions (~15%) | Plus software, office space, training |

Note that even with a full in-house team, companies still require external licensed professionals for tax filing (zeirishi) and often for social insurance advisory (sharoushi). There is no fully self-sufficient in-house model in Japan — some outsourcing is always mandatory.

In-house back-office operations make strategic sense when the company has complex, high-frequency transactions (50+ invoices monthly), needs real-time financial data for fast decision-making, operates in a regulated industry requiring continuous compliance monitoring, or plans to grow to 100+ employees in Japan within 2-3 years. Companies navigating Japan's labor compliance landscape may also benefit from in-house HR expertise as their workforce grows.

The Hybrid Model: Why Most Growing Companies Choose It

The hybrid model combines outsourced specialist functions with a lean in-house coordination team — this approach dominates among foreign companies with 20-100 employees because it balances cost efficiency with operational control.

In a typical hybrid arrangement, the company employs one bilingual administrative coordinator (¥4-6 million annual salary) who serves as the internal point of contact for all back-office matters. This coordinator manages vendor invoices, employee queries, and daily banking operations while liaising with outsourced providers who handle accounting, tax, payroll, and social insurance. The coordinator does not replace specialized expertise but ensures that information flows smoothly between the company's business operations and its external back-office partners.

According to a 2023 EY Japan survey of foreign-affiliated companies, 62% of respondents with 30-100 employees used this hybrid model. The survey found that hybrid companies reported 23% higher satisfaction with their back-office operations compared to fully outsourced companies, primarily because the in-house coordinator reduced response times for routine matters from 24-48 hours to same-day resolution.

The hybrid model works best when structured around a clear division of responsibilities:

- In-house coordinator handles: Daily banking transactions, vendor payment scheduling, employee document requests, office administration, seal management, and communication relay between HQ and local providers

- Outsourced provider handles: Monthly bookkeeping and financial statements, payroll calculation and processing, social insurance filings and annual reviews, year-end adjustment, corporate secretarial filings

- Licensed professionals handle: Tax return preparation and filing (zeirishi), complex labor advisory (sharoushi), legal matters (bengoshi/attorney as needed)

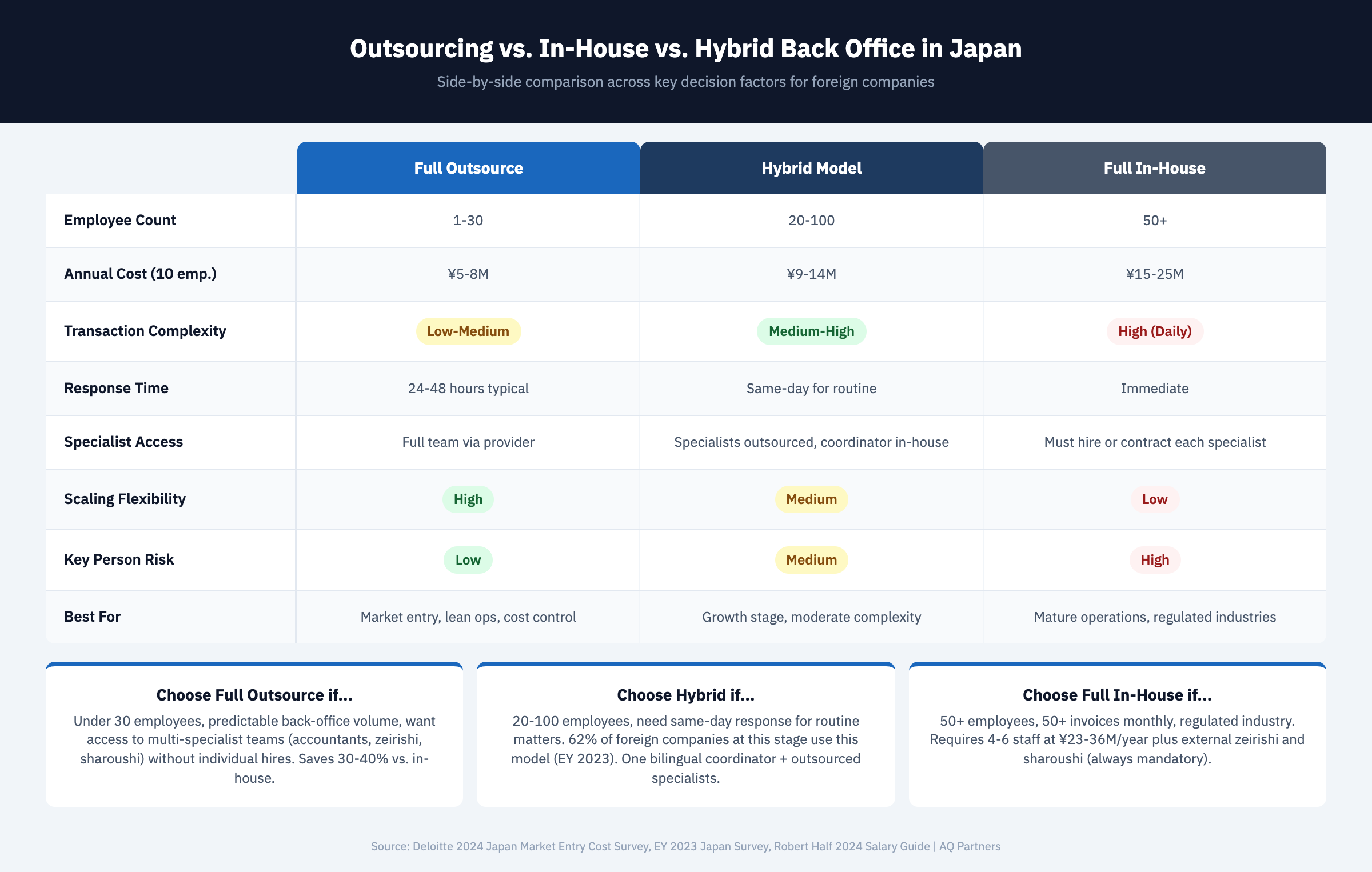

Decision Framework: Choosing the Right Model

The optimal back-office model depends on four variables — company size, transaction complexity, growth trajectory, and the availability of bilingual talent in your industry and location.

| Factor | Full Outsource | Hybrid | Full In-House |

|---|---|---|---|

| Employee Count | 1-30 | 20-100 | 50+ |

| Annual Cost (10 employees) | ¥5-8M | ¥9-14M | ¥15-25M |

| Transaction Complexity | Low-medium | Medium-high | High (daily decisions) |

| Response Time | 24-48 hours typical | Same-day for routine | Immediate |

| Specialist Access | Full team via provider | Specialists outsourced, coordinator in-house | Must hire or contract each specialist |

| Scaling Flexibility | High — adjust scope with provider | Medium — add in-house or expand scope | Low — hiring takes 3-6 months |

| Key Person Risk | Low — provider has team depth | Medium — coordinator departure disruptive | High — specialized roles hard to backfill |

| Best For | Market entry, lean ops, cost control | Growth stage, moderate complexity | Mature operations, regulated industries |

A critical factor that many companies overlook is key person risk. In-house back-office teams in Japan — particularly at smaller subsidiaries — often rely on one or two individuals who hold all institutional knowledge of the company's compliance obligations, government contacts, and filing history. When these individuals leave (and Japan's job market has seen increasing turnover, with MHLW reporting the 2023 overall separation rate at 15.4%), the company faces a knowledge vacuum that can take months to fill. Outsourced providers mitigate this risk through team-based service delivery, documented processes, and institutional continuity.

Companies evaluating how back-office complexity impacts speed and cost should factor in the model choice as a primary cost driver. The right model at the wrong company stage creates either unnecessary expense (premature in-house hiring) or operational bottlenecks (continued full outsourcing beyond its optimal scale).

Selecting an Outsourced Provider: What to Evaluate

Choosing the right outsourced back-office provider in Japan requires evaluating six criteria — bilingual capability, licensing coverage, service scope, technology platform, scalability, and experience with foreign-affiliated companies.

Bilingual capability is non-negotiable. The provider must communicate with your team in English while conducting all government interactions in Japanese. This means genuine bilingual professionals, not translation services layered on top of Japanese-only staff. Test this during the evaluation process by assessing whether the provider can explain complex concepts like the year-end adjustment or social insurance standard remuneration review in clear English.

Licensing coverage determines what the provider can legally deliver. Verify that the provider has licensed zeirishi professionals for tax work and access to sharoushi professionals for social insurance advisory. Some providers integrate these licensed professionals in-house; others coordinate with external specialists. Both models work, but the coordination model requires verifying that the handoff processes are seamless.

Service scope should match your needs without forcing you to manage multiple vendors. Integrated providers who cover accounting, tax coordination, payroll, HR administration, and corporate secretarial work reduce the coordination burden on your team. According to PwC's Japan corporate tax summary, the complexity of Japan's multi-layered tax system alone justifies engaging a provider with broad compliance expertise.

Technology platform matters for data accessibility and HQ reporting. Leading providers use Japanese cloud accounting platforms like freee or MoneyForward that provide English-language dashboards while maintaining J-GAAP compliant books. Verify that the provider's system can generate financial reports in the format your headquarters requires — whether that is IFRS consolidation packages, US GAAP trial balances, or custom management reports.

The provider selection process should also assess the firm's experience with your specific entity structure, whether that is a KK, GK, or branch office. Each structure creates different back-office requirements, and a provider experienced with your entity type will onboard faster and avoid early-stage mistakes.

Transition Planning: Moving Between Models

Transitioning between back-office models in Japan requires 3-6 months of preparation — moving too fast risks compliance gaps, data loss, and disrupted employee services during the transition period.

The most common transition is from full outsourcing to hybrid, typically triggered when a company reaches 20-30 employees and decides to bring a coordinator in-house. This transition involves:

- Month 1-2: Define which functions remain outsourced and which the coordinator will handle. Document all current workflows, filing deadlines, and government contact points.

- Month 2-3: Hire the coordinator and begin a parallel-running period where both the coordinator and outsourced provider handle functions simultaneously.

- Month 3-4: Gradually shift daily operations to the coordinator while maintaining outsourced provider access for specialist functions and backup.

- Month 4-6: Fully transition to the hybrid model with clear escalation paths and service level agreements with the outsourced provider for retained functions.

The reverse transition — from in-house to outsourced — is more difficult and more common than companies expect. Japan's strong employment protections mean that reducing in-house back-office staff requires careful handling. Reassignment to other roles is preferable to termination, and any separation must meet the "objectively reasonable and socially acceptable" standard under the Labor Contract Act. Companies making this transition need legal counsel to manage the employment aspects while simultaneously onboarding the new outsourced provider.

Regardless of direction, timing the transition to avoid peak compliance periods is critical. Avoid transitioning during January (withholding tax summaries), May-June (corporate tax filing season for March FY-end companies), or July (social insurance annual review). The September-November window typically offers the least compliance disruption for transitions.

Frequently Asked Questions

Is it possible to fully outsource everything and have zero staff in Japan?

Functionally yes, but with limitations. Some banking operations, seal management, and government office interactions may require physical presence. Companies can address this through an outsourced provider who offers representative services, or by using an Employer of Record (EOR) arrangement. However, a company with its own legal entity in Japan typically benefits from at least one local point of contact, even if that person handles no back-office functions directly.

How do we ensure quality when outsourcing back-office work?

Establish clear service level agreements (SLAs) covering response times, filing accuracy, and reporting deadlines. Request monthly reconciliation reports and quarterly compliance reviews. The most effective quality assurance comes from maintaining enough internal understanding of Japan's compliance requirements to ask informed questions — a finance leader at headquarters who understands the basics of Japanese corporate tax and social insurance can hold providers accountable far more effectively than one who delegates blindly.

What happens if our outsourced provider makes a compliance error?

Liability for compliance errors generally rests with the company, not the provider, unless the engagement contract specifies otherwise. However, reputable providers carry professional liability insurance and will take corrective action at their own cost. For tax-related errors, the licensed zeirishi who signed the return bears professional liability under the Certified Public Tax Accountant Act. This is one reason why ensuring your provider uses properly licensed professionals — rather than unlicensed staff performing quasi-tax work — is critical.

The outsourcing decision shapes your Japan operation's cost structure, compliance reliability, and operational flexibility for years. Getting it right from the start is significantly easier than correcting course later. AQ Partners provides integrated back-office outsourcing services — accounting, tax coordination, payroll, HR administration, and corporate secretarial — specifically designed for foreign companies operating in Japan. Contact us for a consultation to evaluate the right model for your company's size and growth trajectory.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.