Monthly Bookkeeping & Tax Compliance in Japan

Key Takeaways

- Monthly bookkeeping in Japan follows a structured close cycle that feeds directly into tax compliance — companies must record all transactions, reconcile bank accounts, process payroll journal entries, and prepare management reports within 10-15 business days of month-end to maintain the data quality required for accurate tax filings.

- Provisional corporate tax payments due at the 6-month mark require reliable mid-year financials — companies with prior-year corporate tax liability exceeding JPY 200,000 must make a provisional payment (chukan shinpo) equal to 50% of the prior year's tax or based on interim financial statements, according to the National Tax Agency.

- Consumption tax quarterly reporting preparation must happen monthly to avoid year-end scrambles — companies with prior-year consumption tax liability above JPY 4.8 million must file quarterly, and those above JPY 48 million must file monthly. Monthly tracking of input and output tax ensures accurate interim filings.

- Withholding tax on employee salaries must be remitted by the 10th of the following month — late remittance triggers a 10% non-compliance penalty. Companies with fewer than 10 employees can apply for semi-annual remittance (noki no tokurei), reducing the frequency to January and July payments.

- Monthly discipline prevents year-end crisis — companies that close monthly spend 60-70% less time on annual close — according to JETRO's business operations guide, foreign companies that maintain monthly bookkeeping discipline report significantly smoother tax filing seasons and fewer audit issues.

Why Monthly Bookkeeping Matters for Tax Compliance in Japan

Monthly bookkeeping in Japan is the operational rhythm that connects daily transaction recording to the country's extensive tax compliance obligations — including corporate tax provisional payments, consumption tax interim filings, withholding tax remittances, and social insurance contributions that all operate on monthly or quarterly cycles.

For foreign companies accustomed to minimal mid-year reporting, Japan's compliance calendar is intensive. Tax obligations do not wait until year-end: withholding tax is due monthly, consumption tax may be due quarterly or monthly, and provisional corporate tax is due at the fiscal year's midpoint. Each of these obligations depends on accurate, up-to-date books. Companies that defer bookkeeping to quarterly or annual batches find themselves unable to meet these interim deadlines accurately, triggering penalties and compounding errors that become expensive to correct. This post explains what your accountant or bookkeeping provider actually does every month — and why each step matters for compliance.

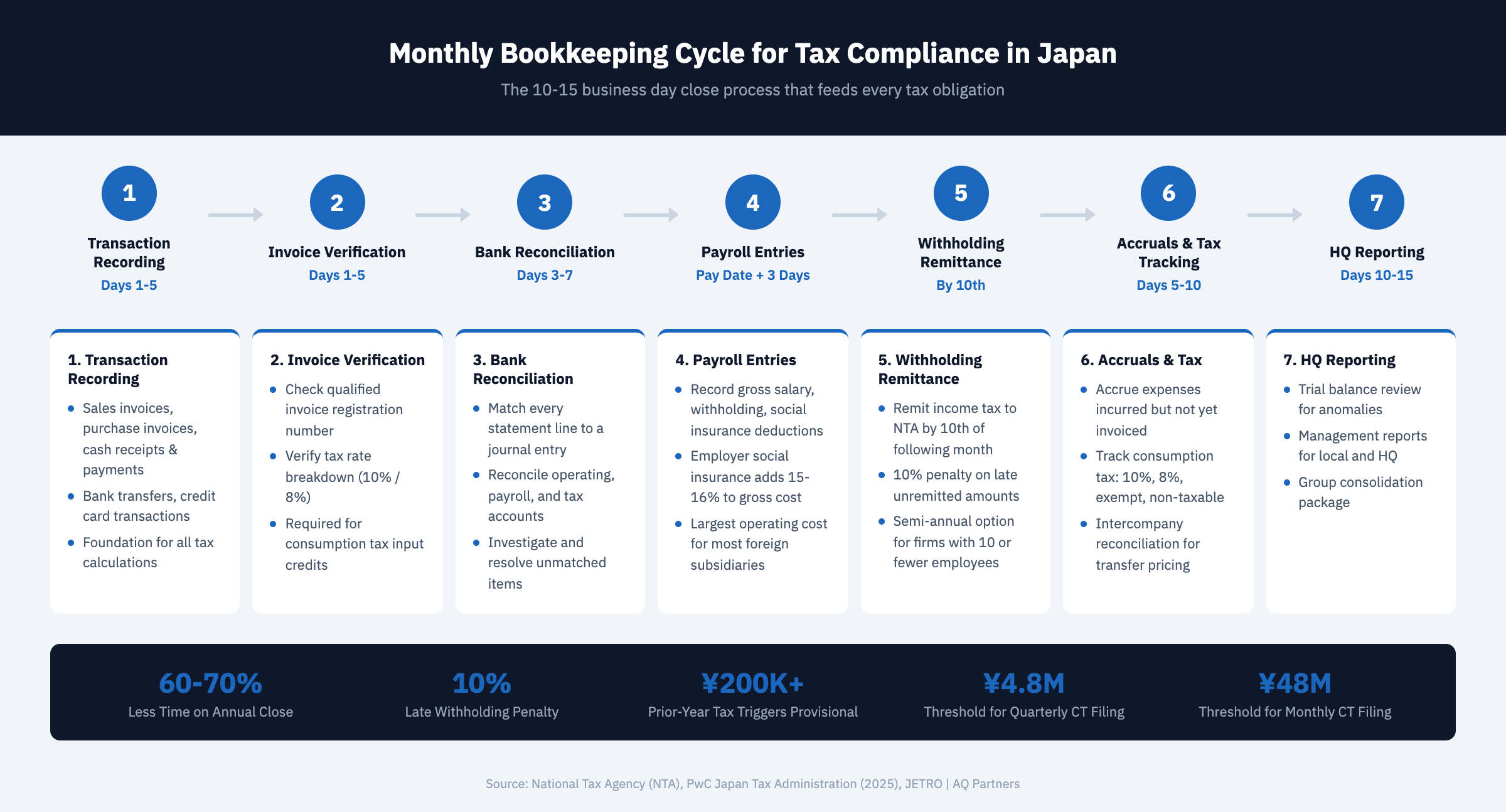

The Monthly Close Process: Steps and Timeline

A well-structured monthly close in Japan follows a 10-15 business day cycle after month-end, covering transaction recording, reconciliation, accruals, and reporting — each step building on the previous one.

The monthly close begins with ensuring all transactions for the period have been recorded in the journal. This includes sales invoices issued, purchase invoices received, cash receipts and payments, bank transfers, credit card transactions, and payroll entries. In Japan, the qualified invoice system adds a verification step: every purchase invoice must be checked for the seller's registration number, proper tax rate breakdown, and consumption tax calculation before recording.

Bank reconciliation follows — matching every bank statement transaction to a corresponding journal entry. Japanese companies typically maintain multiple bank accounts (main operating, payroll, tax payment), and each must be reconciled individually. Unreconciled items are investigated and resolved before the close is finalized.

Accrual entries capture expenses incurred but not yet invoiced (utility estimates, professional fees) and revenue earned but not yet billed. These accruals ensure that each month's financial results reflect economic reality rather than cash timing. Finally, the general ledger trial balance is reviewed for anomalies, and management reports are prepared for both local management and headquarters reporting.

| Monthly Task | Typical Timeline | Tax/Compliance Connection | Consequence of Delay |

|---|---|---|---|

| Transaction recording | Days 1-5 | Foundation for all tax calculations | Inaccurate interim tax filings |

| Invoice verification (qualified invoice check) | Days 1-5 | Consumption tax input credit eligibility | Lost input tax credits; potential audit adjustments |

| Bank reconciliation | Days 3-7 | Cash position accuracy; fraud detection | Undetected errors compound over months |

| Payroll journal entries | Payroll date + 3 days | Withholding tax, social insurance deductions | Late withholding tax remittance penalty (10%) |

| Withholding tax remittance | By 10th of following month | Income tax withholding compliance | 10% penalty on unremitted amount |

| Social insurance premium remittance | End of following month | Health insurance, pension contributions | Penalties and potential coverage gaps for employees |

| Accrual adjustments | Days 5-10 | Accurate period-end financials for management | Misleading financial reports to HQ |

| Intercompany reconciliation | Days 7-12 | Transfer pricing documentation; consolidation | Consolidation errors; TP audit risk |

| Consumption tax tracking | Days 5-10 | Quarterly/monthly consumption tax filings | Inaccurate interim consumption tax returns |

| Management reporting to HQ | Days 10-15 | Group consolidation, budget monitoring | Delayed or inaccurate consolidation packages |

Provisional Tax Payments and Mid-Year Calculations

Provisional corporate tax payments (chukan shinpo) require reliable mid-year financial data — companies without monthly bookkeeping discipline cannot accurately calculate these obligations.

Companies whose prior-year corporate tax liability exceeded JPY 200,000 must make a provisional payment within 2 months of the 6-month anniversary of their fiscal year start. The default calculation method simply takes 50% of the prior year's final tax liability. However, companies can elect to file an interim return based on actual results for the first six months, which may produce a lower payment if current-year performance is weaker than the prior year.

Electing the interim-return method requires a proper six-month close — complete financial statements for the first half of the fiscal year. Companies that have not maintained monthly bookkeeping cannot produce these interim financials on the tight deadline (2 months after the six-month mark), forcing them to use the prior-year method even when actual results would produce a lower payment. This represents a direct cash flow cost of poor bookkeeping discipline. According to PwC's Japan tax administration summary, the difference between prior-year and actual-basis provisional payments can be significant for companies experiencing revenue volatility.

Consumption Tax: Monthly Tracking for Quarterly and Monthly Filers

Consumption tax filing frequency depends on prior-year liability — and companies filing quarterly or monthly need monthly bookkeeping to produce accurate interim returns.

Japan's consumption tax filing frequency is determined by the prior year's consumption tax liability. Companies with liability up to JPY 4.8 million file annually. Those between JPY 4.8 million and JPY 48 million file quarterly (three interim returns plus the annual final return). Companies exceeding JPY 48 million file monthly (eleven interim returns plus the annual final). Each interim return requires accurate calculation of output tax collected and input tax credits claimed during the period.

Monthly consumption tax tracking involves categorizing every transaction by tax treatment: standard rate (10%), reduced rate (8%), exempt, non-taxable, and transactions with non-registered invoice suppliers. The bookkeeping requirements for Japan include verifying every input invoice against the qualified invoice system standards. Errors in monthly consumption tax tracking compound through quarterly and annual filings, and the NTA's increasingly sophisticated cross-referencing between buyer and seller returns means discrepancies are flagged systematically.

Payroll Entries, Withholding Tax, and Social Insurance

Payroll processing generates some of the most compliance-sensitive journal entries in Japanese bookkeeping — connecting salary payments to withholding tax remittance deadlines and social insurance contribution schedules.

Each payroll cycle requires journal entries recording gross salary expense, employee income tax withholding, employee social insurance deductions (health insurance, pension, employment insurance), and net salary payments. The employer's matching social insurance contributions must be recorded separately as company expenses. Withholding tax collected from employees must be remitted to the tax office by the 10th of the following month — missing this deadline triggers a 10% non-compliance penalty on the unremitted amount.

Social insurance premiums are determined annually based on the employee's April-June compensation (the "standard monthly remuneration" or hyojun getsu gaku hoshu), with adjustments for significant salary changes. Monthly journal entries must reflect the current premium rates and any mid-year adjustments. The employer's share of social insurance typically adds 15-16% to the gross salary cost, a figure that must be accurately accrued for reliable monthly financial reporting. Proper payroll bookkeeping is essential for accurate corporate income tax calculations, as salary-related expenses constitute the largest operating cost for most service-oriented foreign subsidiaries in Japan.

Intercompany Transactions and Transfer Pricing Documentation

Monthly recording of intercompany transactions prevents the accumulation of unreconciled balances that create both consolidation errors and transfer pricing audit risk.

Foreign subsidiaries in Japan frequently transact with their parent company and fellow subsidiaries — management fees, royalties, shared service allocations, intercompany loans, and inventory transfers. Each of these transactions must be recorded monthly with supporting documentation that demonstrates arm's-length pricing. Monthly intercompany reconciliation confirms that both parties have recorded the same transaction at the same amount in the same period, preventing the balance discrepancies that trigger audit inquiries.

Japan's transfer pricing rules require companies with consolidated revenue exceeding JPY 100 billion to prepare Country-by-Country Reports (CbCR), and those with transactions exceeding JPY 5 billion to maintain local files. Even companies below these thresholds benefit from maintaining contemporaneous documentation, as the NTA can request transfer pricing explanations during any corporate tax audit. Monthly recording with proper documentation — rather than year-end batch recording — creates the contemporaneous evidence that best supports arm's-length pricing arguments.

How Monthly Discipline Prevents Year-End Crisis

Companies that maintain monthly bookkeeping discipline typically complete their annual close in 2-3 weeks, while those relying on annual batch processing face 2-3 months of concentrated effort — often resulting in late filings and penalties.

Japan's corporate tax return is due within 2 months of the fiscal year end. A company closing on March 31 must file by May 31. This timeline leaves minimal room for companies that need to reconstruct a full year of transactions during the close period. Monthly closers enter this period with 11 months already closed and reconciled — they need only finalize December entries, prepare year-end adjustments, and compile the tax return. Annual batch processors must reconstruct 12 months of transactions, reconcile bank accounts for the full year, chase missing invoices, and resolve accumulated discrepancies under deadline pressure.

The quality difference is equally significant. Tax returns prepared from monthly-closed books benefit from issues being identified and resolved close to the transaction date, when context and documentation are readily available. Returns prepared from batch-processed annual books inherit every unresolved discrepancy accumulated over 12 months, with limited ability to investigate transactions from the distant past. The common bookkeeping errors that create downstream compliance risk are far more likely to persist in annual-batch environments than in monthly-close operations.

Monthly bookkeeping is the operational foundation that makes every other compliance obligation in Japan manageable. AQ Partners provides disciplined monthly bookkeeping services that keep your Japan entity's books current, accurate, and ready for every tax deadline. Contact us to establish a reliable monthly close process for your Japan operations.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.