Bookkeeping Errors That Create Compliance Risk

Key Takeaways

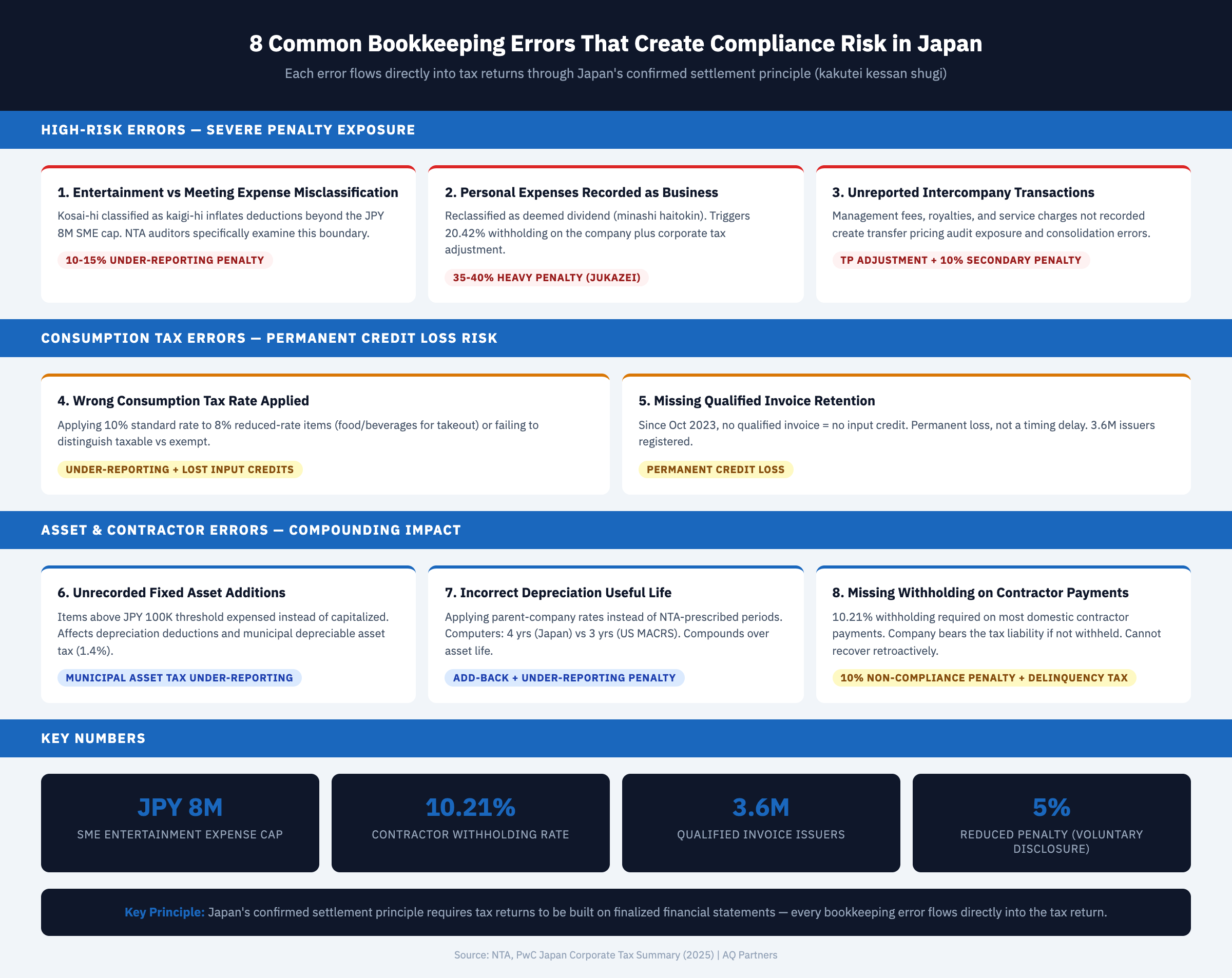

- Misclassified expenses are the most common bookkeeping error in Japan — and the most consequential for tax filings — entertainment expenses (kosai-hi) misclassified as meeting expenses (kaigi-hi) inflate tax deductions beyond the JPY 8 million SME cap, triggering under-reporting penalties of 10-15% on the additional tax owed upon NTA audit.

- Unreported intercompany transactions create both consolidation errors and transfer pricing audit risk — Japan's NTA actively scrutinizes related-party transactions, and companies with unrecorded management fees, royalties, or service charges face potential transfer pricing adjustments plus a secondary penalty of up to 10% of the adjustment amount.

- Incorrect consumption tax treatment — especially under the qualified invoice system — directly reduces recoverable input credits — since October 2023, claiming input credits without a properly formatted qualified invoice from a registered issuer results in permanent credit loss, not just a timing delay. According to the NTA, approximately 3.6 million businesses registered as qualified invoice issuers in the first year.

- Failure to track depreciable assets produces compounding errors across both income tax and municipal asset tax — unrecorded fixed asset additions, incorrect useful life assignments, and missing depreciation calculations affect corporate tax depreciation deductions and the separate municipal depreciable asset tax (1.4% of assessed value).

- Ignoring withholding tax on contractor and freelancer payments triggers immediate penalties — Japan requires 10.21% withholding on most domestic contractor payments for services. Failure to withhold shifts the tax liability to the paying company, with a 10% non-compliance penalty on top of the unremitted withholding amount.

How Bookkeeping Errors Create Compliance Risk in Japan

Bookkeeping errors in Japan compliance create downstream tax filing problems because Japan's confirmed settlement principle (kakutei kessan shugi) requires corporate tax returns to be built directly on finalized financial statements — meaning every bookkeeping mistake flows automatically into the tax return and becomes visible during NTA examination.

Unlike jurisdictions where bookkeeping errors can be corrected through tax return adjustments without revisiting the financial statements, Japan's tax-book linkage means errors must be corrected at the source. A misclassified expense in the general ledger produces an incorrect line item on the financial statements, which produces an incorrect deduction on the corporate tax return. Each error creates a chain of consequences that extends through consumption tax, withholding tax, and potentially municipal tax filings. This post covers the specific errors foreign companies most frequently make — and how each one cascades into broader compliance problems.

Misclassified Expenses: Entertainment, Meetings, and Welfare

Expense misclassification is the error NTA auditors find most frequently — and in Japan, the consequences are amplified because specific expense categories carry unique tax treatment that does not exist in most other jurisdictions.

The most damaging misclassification involves entertainment expenses (kosai-hi) and meeting expenses (kaigi-hi). Under the Corporate Tax Act, entertainment expenses face strict deductibility limits: SMEs (capital of JPY 100 million or less) can deduct up to JPY 8 million per year, while larger companies can deduct only 50% of entertainment expenses exceeding that threshold. Meeting expenses, by contrast, are fully deductible. The distinction hinges on specific criteria — meals and events under JPY 5,000 per person with proper documentation qualify as meeting expenses rather than entertainment.

Foreign companies frequently misclassify in both directions. Some categorize legitimate entertainment as meeting expenses to avoid the deductibility cap, creating an under-reporting risk. Others classify deductible meeting expenses as entertainment, unnecessarily limiting their deductions. In either case, the NTA audit process specifically examines this boundary, and auditors are experienced at identifying patterns of misclassification. According to PwC's Japan corporate tax summary, entertainment expense treatment is among the top audit adjustment areas for foreign-affiliated companies.

| Bookkeeping Error | Where It Appears | Tax Filing Impact | Penalty Exposure |

|---|---|---|---|

| Entertainment → meeting expense misclassification | Income statement, corporate tax return | Excess deductions beyond JPY 8M cap | Under-reporting penalty: 10-15% |

| Unreported intercompany transactions | Balance sheet, consolidation package | Transfer pricing adjustment; missing income/expense | TP adjustment + up to 10% secondary penalty |

| Wrong consumption tax rate applied | Consumption tax return, journal entries | Incorrect input/output tax calculation | Under-reporting penalty; lost input credits |

| Missing qualified invoice retention | Consumption tax return | Input credits denied — permanent loss | Additional consumption tax owed |

| Personal expenses recorded as business | Income statement, corporate tax return | Disallowed deductions; treated as deemed dividend | Heavy penalty (35-40%) if deliberate |

| Unrecorded fixed asset additions | Balance sheet, depreciation schedule | Missing depreciation deductions; wrong asset tax base | Municipal asset tax under-reporting |

| Incorrect depreciation useful life | Depreciation schedule, corporate tax return | Over or under-claimed depreciation deductions | Add-back adjustment + under-reporting penalty |

| Missing withholding on contractor payments | Cash disbursements, withholding tax return | Company liable for unwithheld tax | 10% non-compliance penalty + delinquency tax |

Unreported Intercompany Transactions

Failing to record intercompany transactions is one of the highest-risk bookkeeping errors for foreign subsidiaries — it simultaneously creates consolidation discrepancies and transfer pricing audit exposure.

Common unreported intercompany transactions include management fees charged by the parent company, royalty payments for intellectual property use, shared service cost allocations, intercompany loan interest, and inventory transfers. When these transactions are not recorded in the Japan subsidiary's books, the subsidiary's financial statements understate expenses (or overstate income), producing an artificially favorable tax position that the NTA can challenge.

Japan's transfer pricing documentation requirements require companies to demonstrate that intercompany transactions are priced at arm's length. Unreported transactions cannot be demonstrated to be arm's length because they do not appear in the records at all. When the NTA identifies unreported intercompany transactions — often through cross-referencing the parent company's disclosures or information exchange with foreign tax authorities — the resulting adjustment typically includes the full income impact plus a secondary penalty. According to Ministry of Finance statistics, transfer pricing audit adjustments have increased in both frequency and average adjustment size over the past decade.

Consumption Tax Errors and the Qualified Invoice System

Incorrect consumption tax treatment has become significantly more consequential since the qualified invoice system took effect in October 2023 — errors that previously created timing differences now result in permanent credit losses.

The most common consumption tax errors include: applying the standard 10% rate to reduced-rate (8%) items such as food and beverages for takeout, failing to distinguish between taxable and exempt transactions, claiming input credits on invoices from non-registered suppliers, and not retaining qualified invoices with all required elements (seller registration number, tax rate breakdown, and calculated tax amount).

Under the qualified invoice system, input tax credits are only available when the company retains a properly formatted invoice from a registered issuer. If the invoice is missing, improperly formatted, or from a non-registered supplier, the input credit is denied. During a transitional period through 2029, partial credits (80% through September 2026, then 50% through September 2029) are available for purchases from non-registered suppliers, but these transitional provisions require specific bookkeeping treatment to claim.

Mixing Personal and Business Expenses

Recording personal expenses as business deductions is treated with particular severity in Japan — the NTA may reclassify personal expenses as deemed dividends, creating tax liability for both the company and the individual.

This error most commonly occurs in owner-managed subsidiaries or small branches where a single director controls both the company's finances and personal spending. Personal meals, travel, vehicle use, and housing costs recorded as business expenses are disallowed upon audit. Beyond simply denying the deduction, the NTA may treat the amount as a deemed dividend (minashi haitokin) to the director, triggering a 20.42% withholding tax obligation on the company. If the reclassification is determined to be deliberate, the heavy penalty (jukazei) of 35-40% applies to the corporate tax under-reporting.

Prevention requires clear separation of personal and business accounts, documented business purpose for every expense, and consistent application of expense policies. The chart of accounts structure should include sufficient granularity to distinguish between personal and business categories, with review procedures that flag unusual entries for verification.

Fixed Asset Tracking and Depreciation Errors

Depreciation errors compound over the entire useful life of an asset — a single incorrect classification or missed addition can produce years of incorrect tax deductions and municipal asset tax filings.

Common fixed asset errors include: failing to capitalize items above the JPY 100,000 threshold (recording them as immediate expenses instead), applying home-country useful life periods rather than NTA-prescribed periods, using the wrong depreciation method for the asset category, and not recording partial-year depreciation for assets acquired mid-year. Each error affects both corporate income tax deductions and the separate municipal depreciable asset tax (approximately 1.4% of assessed value) filed with local municipalities.

For foreign companies, the most frequent mistake is applying parent-company depreciation policies rather than Japanese tax rules. A U.S. parent may depreciate computers over 3 years under MACRS, but Japan prescribes 4 years. Office furniture might be depreciated over 7 years globally but carries an 8-15 year useful life in Japan. These differences require maintaining parallel depreciation schedules — one for local tax purposes and one for group reporting — with the difference tracked as a deferred tax adjustment. Companies that neglect this parallel tracking lose tax deductions they are entitled to and risk penalties on deductions they are not. Understanding the broader consequences of accounting non-compliance reinforces why asset tracking discipline matters.

Withholding Tax on Contractor and Freelancer Payments

Japan requires withholding tax on most domestic payments to individual contractors and certain professional services — and the paying company, not the recipient, bears the compliance obligation and penalty for failure to withhold.

Payments to domestic individual contractors for services including writing, design, consulting, lectures, and professional services are subject to 10.21% withholding (on amounts up to JPY 1 million; 20.42% on amounts exceeding JPY 1 million). Many foreign companies are unaware of this obligation because their home countries do not impose withholding on domestic contractor payments. The error typically emerges during an NTA audit when the examiner reviews the company's accounts payable records and identifies contractor payments made without withholding.

When withholding has not been applied, the paying company becomes liable for the unwithheld tax amount plus a 10% non-compliance penalty (funofu kazei). Delinquency tax (entaizei) of 2.4-8.7% per annum compounds on top from the original due date. The company cannot recover the unwithheld amount from the contractor retroactively in most practical situations, making this error an outright cost increase. According to the NTA, withholding tax compliance on contractor payments is a standard examination item for foreign-affiliated companies. Establishing proper procedures through monthly bookkeeping processes ensures withholding is applied and remitted correctly from the outset.

Frequently Asked Questions

What is the difference between entertainment expenses and meeting expenses in Japan?

Entertainment expenses (kosai-hi) include meals, gifts, events, and hospitality provided to external parties such as clients and business partners. Meeting expenses (kaigi-hi) cover meals and refreshments provided during business meetings, limited to JPY 5,000 per person with documentation of attendees, date, location, and business purpose. The distinction matters because entertainment expenses face deductibility caps (JPY 8 million for SMEs) while meeting expenses are fully deductible.

How quickly do bookkeeping errors need to be corrected?

Errors should be corrected as close to the transaction date as possible. For errors discovered before the tax return is filed, corrections can be made through journal adjustments without penalty. For errors discovered after filing, an amended return must be filed. If the NTA discovers the error during an audit before the company files an amendment, the under-reporting penalty applies automatically. Companies maintaining monthly bookkeeping discipline catch and correct errors before they reach the tax return.

Are there any safe harbors for bookkeeping errors in Japan?

Japan does not have a formal "safe harbor" for bookkeeping errors. However, the voluntary disclosure system provides penalty reduction incentives. If a company discovers and corrects an error by filing an amended return before receiving an NTA audit notification, the under-reporting penalty is reduced to 5% (from 10-15%). This creates a strong incentive for proactive error identification through regular internal reviews of bookkeeping accuracy.

Preventing bookkeeping errors requires Japan-specific knowledge, systematic processes, and regular oversight. AQ Partners provides bookkeeping services designed to catch and prevent the errors described above, protecting your Japan entity from downstream compliance risk. Contact us to strengthen your bookkeeping accuracy.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.