Japan Accounting Basics for Foreign Companies

Key Takeaways

- Japan requires all companies to maintain double-entry bookkeeping and statutory books under the Companies Act — the journal (shiwake-cho) and general ledger (sokanjo-motcho) are mandatory regardless of company size, and must be retained for 10 years from the closing date of the fiscal year in which they were created.

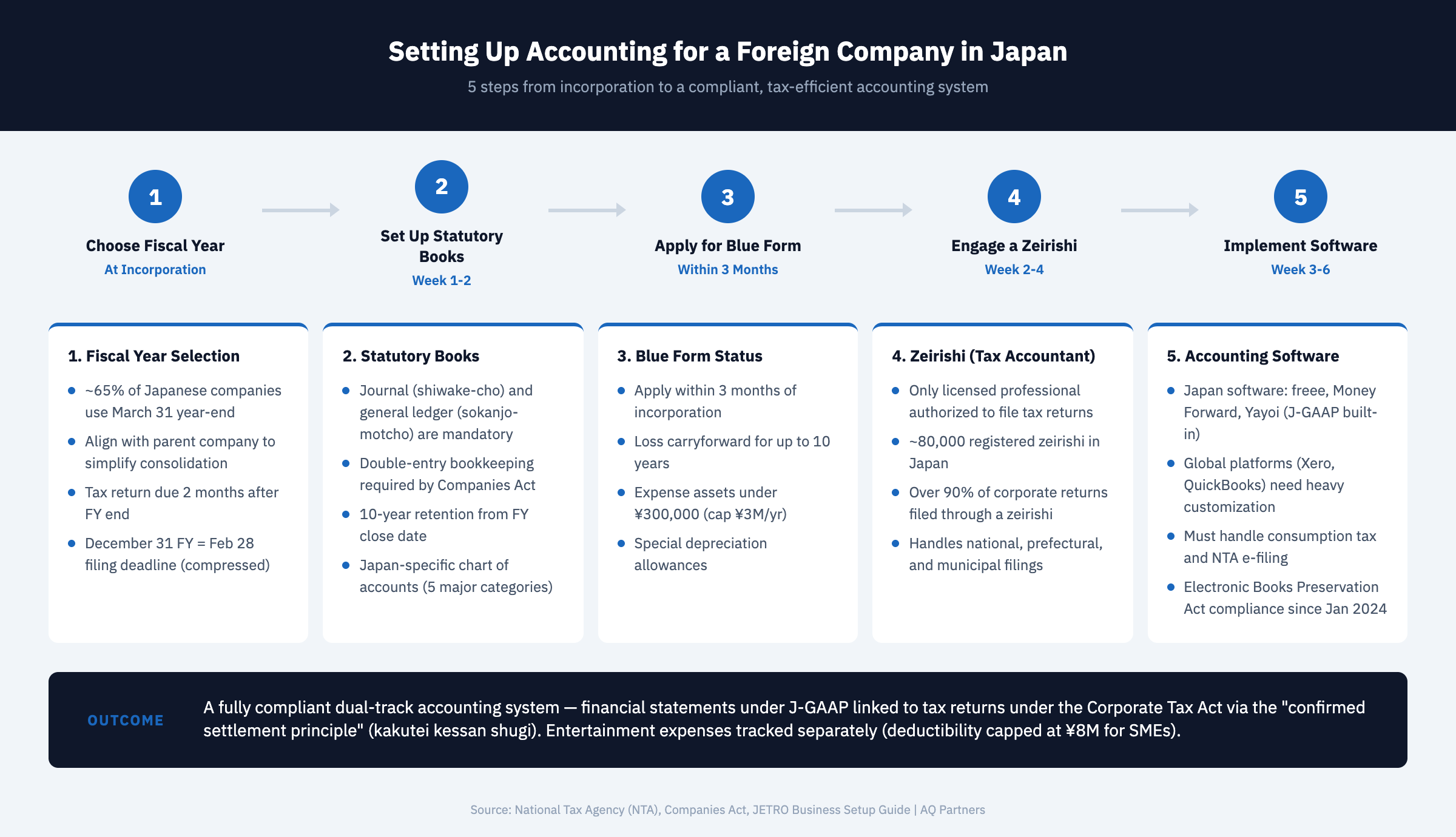

- Fiscal years in Japan are flexible but March 31 dominates — approximately 65% of Japanese corporations close their books on March 31, according to the National Tax Agency. Foreign subsidiaries may choose any 12-month period, but aligning with the parent company's fiscal year simplifies consolidation.

- Tax accounting and financial accounting are separate systems that must be reconciled — Japan maintains a "confirmed settlement principle" (kakutei kessan shugi) where tax returns must be based on finalized financial statements, but tax law overrides GAAP on specific deductions and timing differences.

- A licensed tax accountant (zeirishi) is effectively required for corporate tax compliance — while not legally mandated, the complexity of Japan's tax code means that over 90% of corporate tax returns are filed through a zeirishi, according to JETRO's business setup guide.

- Blue Form (aoiro shinkoku) filing status unlocks critical tax benefits but requires disciplined bookkeeping — benefits include loss carryforward for 10 years, special depreciation allowances, and SME expensing thresholds up to JPY 300,000 per asset.

What Japan Accounting Basics Mean for Foreign Companies

Japan accounting basics encompass the fundamental bookkeeping obligations, statutory reporting requirements, and tax compliance framework that every company operating in Japan must follow from day one. For a foreign company establishing a subsidiary or branch office, understanding these basics is not optional — it is the foundation on which every other compliance obligation rests.

Japan's accounting system draws from the Companies Act (kaisha-ho), the Corporate Tax Act (hojin-zei ho), and Japanese Generally Accepted Accounting Principles (J-GAAP). These three layers interact in ways that differ meaningfully from most Western jurisdictions. The financial statements you prepare for shareholders must follow the Companies Act and J-GAAP, while the tax returns you file with the National Tax Agency follow a parallel set of rules that sometimes produce different numbers for the same transaction. This dual-track system — financial accounting versus tax accounting — is one of the most important concepts for foreign operators to grasp early.

Choosing and Setting Up Your Fiscal Year

Your fiscal year in Japan can be any 12-month period you choose, and this decision should be made strategically before incorporation is finalized.

Unlike countries such as Australia or the UK that mandate specific fiscal year ends for tax purposes, Japan allows companies to select any closing date. However, the practical landscape is heavily skewed: approximately 65% of Japanese corporations use an April 1 to March 31 fiscal year, according to NTA statistics. This alignment with the Japanese government's own fiscal year simplifies interactions with regulators, banks, and business partners.

For foreign subsidiaries, the most common approach is to align the Japanese entity's fiscal year with the parent company's reporting period. A U.S. parent closing on December 31, for example, would typically set its Japanese subsidiary to the same calendar year. This eliminates the need for interim consolidation adjustments and reduces the reporting burden on headquarters. However, be aware that a December 31 fiscal year means your corporate tax return is due by February 28 — just two months after year-end — which creates a compressed timeline for closing books, preparing financial statements, and filing returns.

| Fiscal Year End | Tax Filing Deadline | Provisional Tax Payment | Common Users |

|---|---|---|---|

| March 31 | May 31 | November 30 | ~65% of Japanese companies, government-aligned |

| December 31 | February 28/29 | August 31 | U.S./EU parent alignment, calendar year reporters |

| June 30 | August 31 | February 28/29 | Some Australian parent companies |

| September 30 | November 30 | May 31 | Some European and Asian parent companies |

| January 31 | March 31 | September 30 | Rare; some retail businesses |

| Any custom date | 2 months after FY end | 8 months after FY start | Permitted but uncommon |

Statutory Books and the Chart of Accounts

Japanese law requires every company to maintain specific accounting records — the journal and general ledger are non-negotiable, and the chart of accounts must accommodate Japan-specific categories that do not exist in most Western systems.

Under the Companies Act, corporations must maintain a journal (shiwake-cho) recording every transaction in chronological order, and a general ledger (sokanjo-motcho) organizing those transactions by account. These statutory books must be retained for 10 years. The Corporate Tax Act adds its own retention requirements: transaction-related documents such as invoices, receipts, and contracts must be kept for 7 years, extended to 10 years for companies carrying forward tax losses.

The chart of accounts in Japan follows a structure that will look unfamiliar to most foreign finance teams. Japanese accounts are typically organized into five major categories: assets (shisan), liabilities (fusai), net assets (junshisan), revenue (shueki), and expenses (hiyo). Within these categories, Japan uses specific account names mandated by convention and tax reporting — for example, "entertainment expenses" (kosai-hi) receive special tax treatment and must be tracked separately, as the Corporate Tax Act limits deductibility to JPY 8 million per year for SMEs and disallows 50% of entertainment expenses exceeding JPY 8 million for larger companies.

Tax Accounting vs. Financial Accounting

Japan operates a dual-track system where financial statements follow J-GAAP or IFRS for reporting, while tax returns follow the Corporate Tax Act — and the two frequently produce different numbers for the same economic event.

The "confirmed settlement principle" (kakutei kessan shugi) is central to understanding this relationship. Corporate tax returns in Japan must be based on the company's finalized financial statements. You cannot file a tax return without first closing your books under J-GAAP. However, tax law then requires specific adjustments: certain expenses that are valid under GAAP may not be deductible for tax purposes, and some deductions available under tax law may not be recognized in financial statements.

Common areas where tax and financial accounting diverge include depreciation methods and useful life periods, entertainment expense deductibility limits, provisions for doubtful accounts, and the timing of revenue recognition. According to PwC's Japan corporate tax summary, these book-tax differences must be tracked on detailed schedules attached to the corporate tax return — a process that requires Japan-specific expertise and is a primary reason foreign companies engage professional tax advisors.

The Role of the Zeirishi (Licensed Tax Accountant)

A zeirishi is Japan's licensed tax professional — and while hiring one is technically optional, the complexity of Japan's tax system makes professional tax support a practical necessity for foreign companies.

Japan's Certified Public Tax Accountant Act (zeirishi-ho) establishes the zeirishi as the only professional authorized to prepare and file tax returns on behalf of clients. Unlike some countries where any accountant or bookkeeper can handle tax filings, Japan restricts this function to licensed practitioners who have passed a rigorous national examination or met equivalent qualification criteria. According to the Japan Federation of Certified Public Tax Accountants (JFCPTA), there are approximately 80,000 registered zeirishi in Japan.

For foreign companies, the zeirishi serves multiple critical functions: preparing and filing corporate tax returns (national and local), advising on tax-efficient structuring, representing the company during tax audits, and ensuring compliance with consumption tax, withholding tax, and depreciable asset tax obligations. The zeirishi also handles the provisional tax payment calculations due at the midpoint of each fiscal year. Engaging a qualified zeirishi from the outset — ideally one experienced with foreign-owned entities — prevents costly compliance gaps that compound over time.

Blue Form Filing Status: The Foundation of Tax Efficiency

Blue Form (aoiro shinkoku) tax return status provides substantial tax benefits that every foreign company in Japan should secure — but it requires an application filed before the first fiscal year end and ongoing compliance with bookkeeping standards.

Blue Form status must be applied for within 3 months of incorporation (or by the end of the first fiscal year, whichever comes first). Once approved, the company gains access to benefits including: loss carryforward for up to 10 years, special depreciation allowances, the ability for SMEs to immediately expense assets under JPY 300,000 (with an annual cap of JPY 3 million), and deductions for provisions for doubtful accounts. According to NTA guidelines, maintaining Blue Form status requires proper bookkeeping on a double-entry basis with organized record retention.

Loss of Blue Form status — which can result from inadequate bookkeeping or failure to file returns on time — is one of the most damaging compliance failures a company can experience in Japan. The consequences of poor accounting maintenance extend well beyond the loss of specific deductions, affecting the company's overall tax efficiency and credibility with tax authorities for years to come.

What to Set Up on Day One

The first 90 days after incorporation determine whether your Japan entity operates smoothly or struggles with compounding compliance gaps — prioritize these accounting setup steps immediately.

First, select and implement accounting software appropriate for Japan. Japanese accounting software such as freee, Money Forward, or Yayoi is purpose-built for J-GAAP compliance, consumption tax handling, and NTA e-filing. Global platforms like Xero or QuickBooks can work but require significant customization to handle Japan-specific requirements.

Second, establish your chart of accounts with Japan-specific line items. Third, file the Blue Form application with your jurisdictional tax office. Fourth, engage a zeirishi and clarify the division of responsibilities between your internal team (or outsourced bookkeeper) and the tax accountant. Fifth, set up your document retention system — both physical and electronic — in compliance with the Electronic Bookkeeping Preservation Act, which has undergone significant reforms making electronic storage easier but also mandatory in certain circumstances since January 2024.

For companies navigating these decisions alongside broader Japan market entry planning, understanding how accounting obligations fit within the complete corporate tax filing and compliance framework prevents surprises down the road.

Setting up accounting correctly from day one is the single most impactful compliance decision a foreign company makes in Japan. AQ Partners helps foreign companies establish compliant accounting systems, engage qualified tax professionals, and build the operational foundation for long-term success in the Japanese market. Contact us to discuss your Japan accounting setup.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.