How Payroll Works in Japan: Foreign Employer Guide

Key Takeaways

- Japanese payroll follows a gross-to-net calculation deducting income tax, social insurance premiums, and residence tax — employers must withhold and remit these amounts monthly to the National Tax Agency, Japan Pension Service, and municipal governments respectively. A typical employee's total deductions range from 25% to 35% of gross salary.

- Social insurance comprises four mandatory programs: health insurance, employees' pension, employment insurance, and workers' accident compensation insurance — employer contributions for social insurance total approximately 15-16% of salary, roughly matching the employee's share. According to the Japan Pension Service, the combined employer-employee pension contribution rate stands at 18.3% of standard monthly remuneration.

- Income tax withholding (gensen choshu) uses progressive rates from 5% to 45% — employers must calculate monthly withholding using NTA-published tax tables based on salary amount, number of dependents, and whether the employee has submitted a dependency deduction declaration (marufu). Year-end adjustment (nenmatsu chosei) reconciles actual liability.

- Residence tax (juminzei) operates on a one-year lag and is collected via special collection — employers deduct monthly installments from June through May based on the prior calendar year's income. The standard combined rate is approximately 10% (prefectural 4% + municipal 6%).

- Bonuses (shoyo) are subject to separate social insurance and income tax withholding calculations — social insurance premiums on bonuses are capped at a cumulative annual total of ¥5.73 million for health insurance and ¥1.5 million per payment for pension. Bonus withholding tax rates differ from monthly salary tables.

What Is Japanese Payroll and How Does It Differ from Other Countries?

Japanese payroll is the process of calculating employee compensation, withholding mandatory taxes and social insurance contributions, and remitting those amounts to the appropriate government agencies on behalf of employees. For foreign employers establishing operations in Japan, the system differs substantially from payroll in most Western countries in both complexity and employer obligation.

Unlike systems where employees may be largely responsible for their own tax filings, Japan places the withholding and remittance burden squarely on employers. The employer acts as a tax collection agent (gensen choshu gimushya) from the first day of hiring. According to PwC's Japan individual tax summary, employers must withhold income tax at source on every salary payment and remit it to the tax office by the 10th of the following month. Social insurance enrollment, residence tax collection, and annual reconciliation are all employer-driven processes that operate on distinct timelines and reporting cycles.

How Does Gross-to-Net Calculation Work?

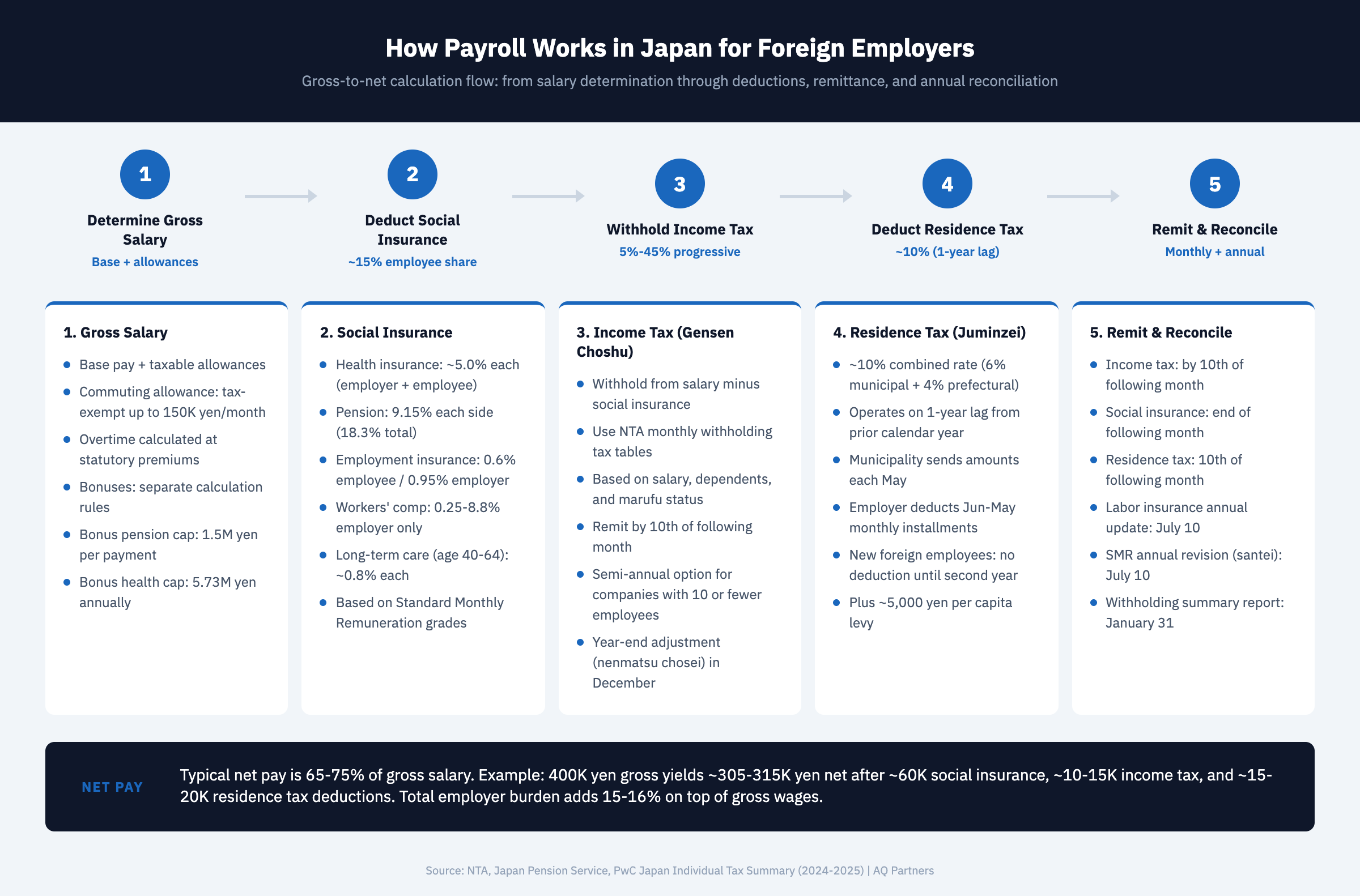

The gross-to-net calculation in Japan involves deducting social insurance premiums, income tax, and residence tax from an employee's gross monthly salary — typically resulting in net pay of 65-75% of the gross amount.

The calculation follows a specific sequence. First, determine the employee's gross salary, including base pay and taxable allowances such as commuting allowance (up to the tax-exempt threshold of ¥150,000 per month for public transit), overtime pay, and role-based allowances. Second, subtract social insurance premiums — health insurance, pension, employment insurance, and long-term care insurance (for employees aged 40-64). Third, apply income tax withholding to the post-social-insurance amount using the NTA's monthly withholding tax tables. Fourth, subtract residence tax (special collection amount).

| Deduction Category | Employee Share | Employer Share | Basis |

|---|---|---|---|

| Health Insurance (Kyokai Kenpo) | ~5.0% | ~5.0% | Standard Monthly Remuneration (SMR) |

| Long-Term Care Insurance (age 40-64) | ~0.8% | ~0.8% | Standard Monthly Remuneration |

| Employees' Pension (Kosei Nenkin) | 9.15% | 9.15% | Standard Monthly Remuneration |

| Employment Insurance (Koyo Hoken) | 0.6% | 0.95% | Total monthly wages |

| Workers' Accident Compensation | 0% | 0.25-8.8% | Total wages (rate varies by industry) |

| Income Tax (Gensen Choshu) | 5-45% (progressive) | N/A (withholding agent) | Salary minus social insurance |

| Residence Tax (Juminzei) | ~10% | N/A (special collection) | Prior year's taxable income |

| Total Approximate Burden | 25-35% | 15-16% | Varies by salary level |

A practical illustration: an employee earning a gross monthly salary of ¥400,000 would see approximately ¥60,000 deducted for social insurance (health, pension, employment insurance combined), ¥10,000-15,000 for income tax, and ¥15,000-20,000 for residence tax — resulting in net pay of roughly ¥305,000-¥315,000.

What Is Income Tax Withholding (Gensen Choshu)?

Gensen choshu is Japan's source-deduction system requiring employers to calculate and withhold income tax from each salary payment, then remit the withheld amount to the tax office by the 10th of the following month.

The withholding amount depends on three factors: the employee's monthly salary after social insurance deductions, the number of claimed dependents, and whether the employee has submitted a withholding exemption certificate (kyuyo shotoku no fuyo kojo to shinkoku sho, commonly called "marufu"). The National Tax Agency publishes monthly withholding tax tables that employers must use to determine the correct deduction amount.

Monthly withholding is an approximation. Because deductions like life insurance premiums, mortgage interest credits, and spousal dependency status may change during the year, the cumulative withholdings rarely match the employee's actual annual tax liability. This mismatch is resolved through the year-end adjustment (nenmatsu chosei), typically processed with the December payroll. The employer recalculates the employee's annual income tax, applies all eligible deductions, and either refunds the over-withheld amount or collects the shortfall. For most salaried employees in Japan, nenmatsu chosei eliminates the need to file an individual tax return.

Companies with 10 or fewer employees can apply for semi-annual remittance, paying withheld taxes twice a year (July 10 and January 20) rather than monthly — a useful simplification for small foreign subsidiaries.

How Does Social Insurance Work for Employers?

Social insurance in Japan consists of four mandatory programs that employers must enroll in and contribute to — health insurance, employees' pension, employment insurance, and workers' accident compensation insurance — with combined employer costs typically adding 15-16% on top of gross salary.

Health insurance and pension contributions are calculated on the basis of "standard monthly remuneration" (hyojun getsugaku hoshu, or SMR) — a standardized salary grade system rather than actual monthly pay. The Japan Pension Service maintains 50 grades for pension and 50 grades for health insurance. An employee's SMR is determined upon enrollment and recalculated annually through the "algorithm revision" (santei) process every September, based on the average of April through June compensation. If salary changes significantly mid-year (two or more grades), a mid-year revision (zuiji kaitei) may be triggered.

Employment insurance covers unemployment benefits, childcare leave benefits, and vocational training. The rate is split unevenly — employees pay 0.6% while employers pay 0.95% (general industry rate as of fiscal 2024). Workers' accident compensation insurance is funded entirely by the employer, with rates varying from 0.25% for low-risk office work to 8.8% for mining and construction industries.

Foreign companies must be aware that social insurance enrollment is mandatory from the first day of employment for all employees working 30 or more hours per week (or three-quarters of the standard hours at that workplace). Companies that fail to enroll employees face retroactive premium assessments for up to two years. For a comprehensive overview of Japan HR compliance strategies, including social insurance requirements across your workforce, see our pillar guide.

How Does Residence Tax (Juminzei) Special Collection Work?

Residence tax operates on a one-year lag — employers deduct monthly installments from employee salaries between June and May based on each employee's taxable income from the prior calendar year, as calculated by the employee's municipality.

Unlike income tax, which employers calculate themselves, residence tax amounts are determined and communicated by municipal governments. Each May, the municipality sends the employer a special collection tax notification listing the monthly deduction amount for each employee for the upcoming June-to-May cycle. The standard combined rate is approximately 10% of taxable income (6% municipal tax + 4% prefectural tax), plus a per capita levy of approximately ¥5,000.

For newly hired foreign employees who were not in Japan during the prior calendar year, there is no residence tax to deduct initially. Their first residence tax obligation begins in June following a full calendar year of Japan residency. This lag can create confusion for employees who expect consistent deductions from their first paycheck. When employees transfer between companies or leave Japan, the employer must notify the municipality and handle any remaining balance through final salary deductions or direct payment instructions.

How Are Bonuses Processed in Japanese Payroll?

Bonuses (shoyo or shokibarai) in Japan are subject to social insurance premiums and income tax withholding under separate calculation rules from monthly salary — and the majority of Japanese employers pay bonuses twice per year, typically in June and December.

For social insurance, bonus premiums use the same percentage rates as monthly salary but apply to the actual bonus amount (rounded down to the nearest ¥1,000) rather than the standard monthly remuneration grade. The Japan Pension Service caps the pension-eligible bonus amount at ¥1.5 million per payment, while health insurance applies a cumulative annual cap of ¥5.73 million. Bonuses exceeding these caps are not subject to the respective premium calculations.

Income tax withholding on bonuses follows a distinct method. The employer determines the withholding rate by referencing the employee's prior month's salary (after social insurance deductions) and the number of dependents against a special bonus withholding rate table. This rate is then applied to the full bonus amount minus bonus social insurance deductions. Employers must report all bonus payments to the Japan Pension Service within 5 days of payment using a "notification of bonus payment" form. For detailed guidance on payroll software that automates these calculations, see our payroll software guide for Japan.

What Are Payslip and Record-Keeping Requirements?

Japanese labor law requires employers to provide employees with a detailed payslip (kyuyo meisai) for every payment and to maintain payroll records for a minimum of five years — covering all wage calculations, deductions, and payment dates.

Each payslip must itemize: gross salary, each allowance component, each social insurance deduction by type, income tax withheld, residence tax deducted, and net pay. The Labor Standards Act mandates that employers keep a "wage ledger" (chingin dai cho) for each employee. Effective April 2020, the retention period for payroll records was extended from three years to five years (with a transitional measure currently in effect). These records must be available for inspection by the Labor Standards Inspection Office at any time.

Employers must also issue withholding tax certificates (gensen choshu hyo) to each employee by January 31 following the calendar year end. These certificates summarize total compensation paid, total income tax withheld, and social insurance premiums deducted during the year. One copy goes to the employee, and another is submitted to the tax office. For foreign employers managing payroll compliance alongside broader operational obligations, understanding how these requirements fit into the overall payroll compliance framework is essential.

| Payroll Obligation | Frequency | Deadline | Submitted To |

|---|---|---|---|

| Income tax withholding remittance | Monthly | 10th of following month | Tax Office (NTA) |

| Social insurance premium remittance | Monthly | End of following month | Japan Pension Service |

| Residence tax special collection remittance | Monthly | 10th of following month | Municipal Government |

| Labor insurance annual update (rodo hoken nendo koushin) | Annual | July 10 | Labor Bureau |

| Social insurance standard remuneration revision (santei) | Annual | July 10 | Japan Pension Service |

| Year-end adjustment (nenmatsu chosei) | Annual | With December payroll | Processed internally; certificates to Tax Office by Jan 31 |

| Withholding tax summary report (houkoku sho) | Annual | January 31 | Tax Office + Municipality |

| Bonus payment notification | Per bonus | Within 5 days of payment | Japan Pension Service |

Frequently Asked Questions

Do foreign employers need to run payroll differently from Japanese companies?

No — the payroll mechanics are identical regardless of whether the employer is a foreign-owned subsidiary or a domestic Japanese company. The same withholding obligations, social insurance enrollment requirements, and reporting deadlines apply. However, foreign employers frequently face additional complexity in areas such as managing expatriate tax situations, coordinating with social security totalization agreements (Japan has agreements with over 20 countries), and navigating processes in Japanese-language systems. Many foreign employers choose to outsource payroll to a specialized provider to manage these complexities.

What happens during year-end adjustment (nenmatsu chosei)?

Year-end adjustment is an employer-performed reconciliation, typically processed with December payroll, that recalculates each employee's actual annual income tax liability and compares it against cumulative monthly withholdings. The employer collects declaration forms from employees listing deductions such as life insurance premiums, earthquake insurance, dependent family members, and mortgage interest credits. The difference is refunded to or collected from the employee. Approximately 90% of salaried employees in Japan settle their full income tax obligations through this process without filing an individual return.

Is the commuting allowance taxable?

Commuting allowances (tsukin teate) are tax-exempt up to ¥150,000 per month for public transportation. Amounts exceeding this threshold are treated as taxable income. However, commuting allowances are included in the calculation base for social insurance premiums regardless of tax treatment. This distinction means the commuting allowance affects social insurance costs but not income tax withholding (within the exemption limit).

Managing payroll in Japan requires attention to multiple government agencies, distinct calculation methodologies, and strict deadlines. For foreign employers seeking to establish compliant payroll operations without building in-house expertise, AQ Partners provides end-to-end payroll administration as part of our Japan back-office services. Contact us to discuss your payroll setup requirements.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.