Japan Payroll Compliance: Social Insurance & Year-End Adjustment Guide

Japan payroll compliance is among the most technically demanding employer obligations in Asia. Companies operating a Japanese entity must calculate and file social insurance contributions every month, complete a full year-end income tax adjustment process for every employee, maintain My Number records under strict privacy controls, and apply residence tax deductions that arrive each year by municipal notice. Each obligation has its own filing system, its own deadlines, and its own set of government forms — and all of them interact within the same monthly payroll run. This guide explains each requirement in operational detail and defines exactly what payroll software must support to keep a Japan payroll operation compliant.

For a complete overview of the Japan payroll monthly cycle and annual calendar, see our Japan payroll operational guide.

Key Takeaways

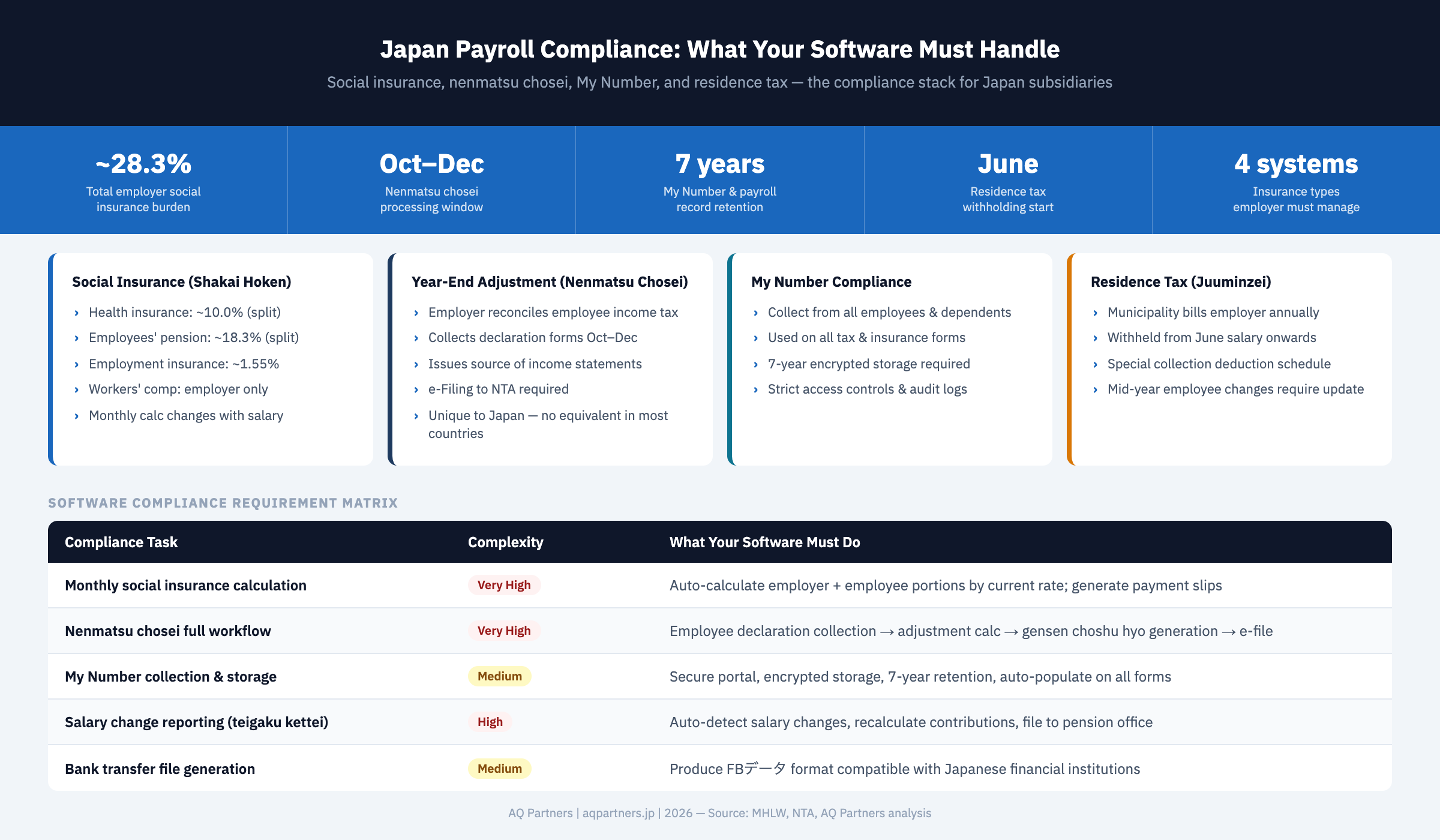

- Social insurance enrollment is mandatory for all full-time employees — Japan's shakai hoken system requires employers to enroll eligible employees and remit both employer and employee contributions monthly, with rates reviewed and updated annually by the Ministry of Health, Labour and Welfare (MHLW).

- Nenmatsu chosei shifts the tax-return burden to the employer — Unlike most countries, Japan requires employers — not individuals — to perform the annual income tax reconciliation for each employee, collecting declaration forms, calculating adjustments, and issuing legally required withholding statements by January.

- My Number compliance is non-negotiable — Employers must collect, store, and accurately apply Individual Numbers for every employee and their dependents, with a 7-year retention requirement and strict security controls mandated by the My Number Act.

- Residence tax deductions arrive by municipal notice and must be applied from June — Each employee's juuminzei amount is assessed by their home municipality and delivered to the employer annually; payroll software must ingest those schedules and apply the correct monthly deductions for 12 months.

- Domestic platforms are the lowest-friction choice — SmartHR, freee HR, and MoneyForward Cloud Payroll support these workflows natively; global HRIS platforms typically require substantial Japan-specific localization before they can handle the full compliance stack.

Japan's Social Insurance System (Shakai Hoken)

Employers must enroll all full-time employees in Japan's shakai hoken system and remit contributions monthly — approximately 10% for health insurance, 18.3% for pension, and 1.55% for employment insurance — with calculations tied to each employee's standardized monthly remuneration bracket and subject to annual rate updates.

Shakai hoken (社会保険) comprises three primary programs: health insurance (kenkou hoken), employees' pension insurance (kousei nenkin hoken), and employment insurance (koyou hoken). Enrollment is mandatory for all full-time employees and for part-time workers who meet minimum hours thresholds — rules that expanded significantly in 2022. The employer handles both enrollment and ongoing contribution administration, splitting the premium cost with employees for health and pension insurance while bearing a larger share of employment insurance.

Health insurance contributions run at approximately 10% of each employee's standardized monthly remuneration, split roughly equally between employer and employee. The exact rate depends on the health insurance association — Kyokai Kenpo for most SMEs, or a company-specific health insurance society for larger employers — and it varies by prefecture. Employees' pension insurance is levied at 18.3% of standardized monthly remuneration, split equally at 9.15% each, and the rate is nationally uniform. Employment insurance is set at approximately 1.55% of monthly wages for general industries in 2025, with the employer contributing a larger share than the employee. All three rates are reviewed annually by the MHLW; updates typically take effect in April.

Monthly contribution amounts are based on each employee's "standard monthly remuneration" (hyojun hoshu geppu), a tiered figure derived from average salary and expressed in brackets from the 1st to the 32nd grade. This figure is formally reviewed through two processes. The annual review (teigaku kettei, 定時決定) runs each July, is based on salary paid in April, May, and June, and sets each employee's bracket from September through the following August. If an employee's salary changes significantly mid-year — typically by two or more bracket grades — a mid-year revision (teiji kettei, 随時改定) must be filed with the Japan Pension Service, resetting the bracket prospectively. Both processes require submission of forms, increasingly via the e-Nenkin Connect electronic filing portal.

What payroll software must do: auto-calculate monthly contributions using current rate tables and each employee's standard monthly remuneration bracket; apply the correct prefecture- and association-specific health insurance rate; update rate tables automatically each April when the MHLW announces revisions; track salary changes and trigger the teiji kettei workflow when bracket shift conditions are met; generate payment slips for monthly contributions; and support e-filing submissions to the Japan Pension Service via e-Nenkin Connect. Software that requires manual bracket lookups or does not automate the teigaku kettei annual cycle introduces material compliance risk at any meaningful headcount. The Ministry of Health, Labour and Welfare (MHLW) publishes English-language employer guidance on social insurance enrollment and contribution obligations.

Year-End Tax Adjustment (Nenmatsu Chosei)

Nenmatsu chosei is Japan's employer-side annual income tax reconciliation — the functional equivalent of an individual tax return, performed by the employer on behalf of every employee, running October through December with withholding statements due by January 31.

In most countries, employees file their own annual income tax returns. Japan's system is different. For the majority of salaried workers, the employer performs the full annual income tax reconciliation — collecting declaration forms, recalculating the year's total tax liability, comparing it against cumulative withholding already paid, and adjusting the December or January payroll accordingly. This process is nenmatsu chosei (年末調整), and it is a mandatory employer obligation under the Income Tax Act. Most Japanese employees never file a personal tax return because their employer has already settled their tax position through this process.

The timeline runs from October through January. In October and November, employers distribute and collect declaration forms from employees. The most important is the 扶養控除等申告書 (fuyou koujyo-tou shinkokusho), the dependent deduction declaration, which captures dependents, household circumstances, insurance premium deductions, housing loan interest, and other items that affect the employee's final tax liability. Once forms are collected, the payroll system recalculates each employee's annual income tax against Japan's graduated tax brackets and withholding tables (gensen choshuu zeigaku hyo), which are updated annually by the National Tax Agency. The adjustment — either a refund to the employee or an additional deduction — is reflected in the December or January payroll run.

The output of nenmatsu chosei is the gensen choshu hyo (源泉徴収票), the withholding tax statement issued to every employee by January 31. This document summarizes annual salary, bonus payments, declared deductions, and final income tax withheld. Employees use it to apply for mortgages, submit personal tax returns when required, and verify income for administrative purposes. The employer must also submit aggregated withholding data to municipalities (for residence tax assessment) and, for employees above certain income thresholds, to the National Tax Agency directly. Official guidance on the nenmatsu chosei process and required forms is published by the National Tax Agency (NTA).

What payroll software must do: provide a structured workflow for collecting employee declaration data via a digital self-service portal or structured paper process; auto-import and validate declaration data; integrate annual NTA withholding tables; auto-calculate the year-end tax adjustment per employee; apply the adjustment to the December or January payroll; generate legally compliant gensen choshu hyo PDFs for employee distribution; produce NTA-compatible XML for e-filing; and maintain an audit trail of all declarations and calculations. Platforms that lack a full nenmatsu chosei workflow force HR teams into manual spreadsheet processes that are both time-consuming and error-prone. For a broader overview of how payroll tooling fits Japan's compliance stack, see the AQ Partners Japan payroll software guide.

My Number (Individual Number) Compliance

Employers must collect and store My Numbers for all employees and their dependents, use them across tax forms, social insurance applications, and withholding statements, retain records for 7 years, and implement access controls and audit logging that meet the security requirements of Japan's My Number Act.

My Number (マイナンバー) is Japan's Individual Number system, introduced in 2016 under the Act on the Use of Numbers to Identify a Specific Individual in Administrative Procedures. Every resident of Japan — including foreign nationals — holds a 12-digit Individual Number used across tax, social insurance, and other administrative processes. For employers, My Number compliance is mandatory and ongoing: Individual Numbers must be collected for every employee and for their dependents who appear on nenmatsu chosei declaration forms.

The uses of My Number in a payroll context are extensive. Individual Numbers must appear on withholding tax statements (gensen choshu hyo), on social insurance enrollment forms submitted to the pension office, on annual payment records submitted to the NTA, and on various forms submitted to municipalities for residence tax purposes. My Numbers flow through the entire payroll compliance cycle — from social insurance enrollment when a new employee joins, through each month's processing run, and into the annual nenmatsu chosei documentation. The PwC Japan Tax Summaries provide useful background on how the My Number system intersects with corporate tax and employer reporting obligations.

Retention requirements are strict. My Numbers and documents on which they appear must be retained for the period for which they are required for administrative purposes — for payroll-related documents, this is generally 7 years. Equally important is the obligation to destroy Individual Numbers promptly once their purpose is served: employers may not retain My Numbers beyond the legally permissible period. Access to My Number data must be limited to personnel with a demonstrable business need, access logs must be maintained and auditable, and data must be protected against unauthorized disclosure. A payroll system that stores My Numbers in unencrypted spreadsheets or shared document folders is not compliant with these requirements regardless of any other capabilities it offers.

What payroll software must do: provide a secure, auditable channel for employees to submit their Individual Numbers; store Individual Numbers in encrypted form with role-based access controls restricted to authorized users; maintain a full audit log of who accessed Individual Number records and when; automatically populate My Numbers on all required output documents — withholding statements, social insurance forms, NTA payment records — without manual re-entry; and flag records for deletion once the retention period has passed. For more on how Japan's compliance requirements affect global HR operations, see our post on Japan HR compliance strategies for global teams.

Residence Tax (Juuminzei) Withholding

Each employee's residence tax liability is assessed by their home municipality and delivered to the employer by annual notice; the employer withholds the specified amount in 12 monthly installments beginning in June, with deduction amounts fixed per employee for the year.

Juuminzei (住民税), or residence tax, is a local income tax levied by prefectures and municipalities on the prior year's income. It is assessed by the municipality where the employee lived on January 1 of the current year — which is why the employer's January withholding tax statements and NTA payment records are consequential: they flow directly into each municipality's assessment of the employee's juuminzei for the coming year.

The standard collection method for salaried employees is "special collection" (tokubetsu choshu), in which the employer withholds the annual juuminzei amount in 12 equal monthly installments from June through May of the following year. Each year in May, municipalities send employers a juuminzei payment notice (特別徴収税額通知書) specifying the exact monthly deduction amount for each employee. These amounts vary by employee based on their home municipality, income, and applicable deductions — meaning a company with employees in multiple municipalities receives multiple sets of notices, each with employee-specific deduction schedules. When an employee leaves mid-year, the employer must either transfer the remaining installments to the new employer or notify the municipality so the employee can pay directly. The JETRO Business Setup Guide provides useful context on the broader administrative environment employers navigate in Japan, including residence tax obligations.

What payroll software must do: ingest or allow manual entry of the annual juuminzei deduction amounts from municipality notices for each employee; apply the correct monthly deduction automatically from June onward; handle mid-year changes when an employee changes municipalities or leaves employment; and generate payment slips for each municipality. The deduction amounts themselves are determined by the municipality, so the software's role is scheduling and application rather than calculation — but it must do so across every employee's individual municipality schedule simultaneously.

What Your Payroll Software Must Handle

The table below maps each major Japan payroll compliance task to its manual complexity and the specific software capability required. Any platform used to run payroll for a Japan entity should be assessed against all ten requirements before deployment.

| Compliance Task | Manual Complexity | Software Requirement |

|---|---|---|

| Monthly social insurance calculation | High | Auto-calculate by salary tier using current rate tables; apply correct prefecture and association rates per employee |

| Annual contribution rate update | Medium | Annual rate table updates applied automatically at the MHLW-mandated effective date with no manual input required |

| Salary change reporting (teigaku kettei / teiji kettei) | High | Teigaku kettei automation each July; mid-year teiji kettei bracket-change detection and e-Nenkin form generation |

| Nenmatsu chosei workflow | Very High | Full workflow: employee declaration form collection → deduction calculation → payroll adjustment → withholding statement generation → e-filing to NTA |

| My Number collection and storage | Medium | Secure employee collection portal; encrypted storage with role-based access controls and full audit logging of all access events |

| Source of income statement generation (gensen choshu hyo) | Medium | Auto-generate NTA-compliant PDF for employee distribution and XML for e-filing; My Number auto-populated on all output |

| Employment insurance rate updates | Medium | Annual rate table loaded by industry category; employer and employee shares calculated separately and applied correctly each April |

| Residence tax (juuminzei) deduction | Low | Annual deduction schedule import from municipality notice; automatic monthly withholding from June; mid-year adjustment processing on employee departure |

| e-Filing to NTA and pension office | High | API-connected filing to e-Nenkin Connect (Japan Pension Service) and eLTAX / e-Tax (NTA) for all required submissions |

| Attendance data integration | High | Native or API integration with kinmu kanri (attendance management) system; auto-import of hours, overtime, and leave data to payroll calculation |

Which Platforms Handle These Best

Japan's domestic payroll platforms have a structural advantage: they were built specifically around the requirements described in this guide, which means nenmatsu chosei, social insurance automation, My Number management, and e-filing are core features rather than localization add-ons.

SmartHR is the market leader for mid-to-large Japanese companies and offers particularly strong social insurance and My Number workflows. Its API is well-documented for integration with external attendance management systems, and it supports the full teigaku kettei and teiji kettei automation cycle alongside a complete nenmatsu chosei employee portal and e-filing capability.

freee HR (freee 人事労務) handles the full payroll and nenmatsu chosei workflow within the freee suite, making it a practical choice for companies already using freee for accounting. Its integration between payroll, HR, and attendance management reduces reconciliation overhead and keeps the compliance stack under a single platform.

MoneyForward Cloud Payroll offers deep integration across the MoneyForward Cloud suite — payroll, accounting, and expense management — and supports automated e-filing for both social insurance changes and year-end withholding submissions. For companies managing both payroll and bookkeeping in Japan, the combined MoneyForward stack reduces manual data transfer between systems.

For a detailed side-by-side comparison of these three platforms — including pricing, language support, and suitability for foreign-owned entities — see our post on the best payroll software in Japan: SmartHR, freee, and MoneyForward compared. If you are weighing a global HRIS platform against a domestic solution, our analysis of global versus domestic payroll software for Japan walks through the decision framework in detail.

How AQ Partners Can Help

AQ Partners provides back-office services for foreign companies operating in Japan, including payroll setup, social insurance enrollment, nenmatsu chosei management, My Number compliance, and ongoing payroll operations support. If your Japanese entity is running payroll on a platform that was not designed for Japan's requirements — or if you are establishing payroll for a new Japan entity and need guidance on software selection and configuration — our team can assess your current setup, close compliance gaps, and build the operational infrastructure to stay compliant as Japan's regulatory requirements evolve.

We work with the full range of platforms used by foreign-owned entities in Japan, from SmartHR and freee to MoneyForward Cloud Payroll and global HRIS localization projects, and we maintain direct relationships with Japanese labor and social insurance professionals (社会保険労務士, shakai hoken roumushi) who can validate your payroll configuration against current MHLW and NTA requirements.

Is your payroll software compliant with Japan's requirements? Contact AQ Partners →

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.