Tax Loss Carryforward Rules in Japan: NOL Strategy

Tax loss carryforward (繰越欠損金, kurikoshi kessонkin) is a provision under Japan's Corporation Tax Act that allows companies to carry net operating losses (NOLs) from one fiscal year forward to offset taxable income in future years. For foreign subsidiaries entering Japan—where initial setup costs often produce multi-year losses—understanding and maximizing NOL carryforward is one of the most impactful tax planning strategies available.

Key Takeaways

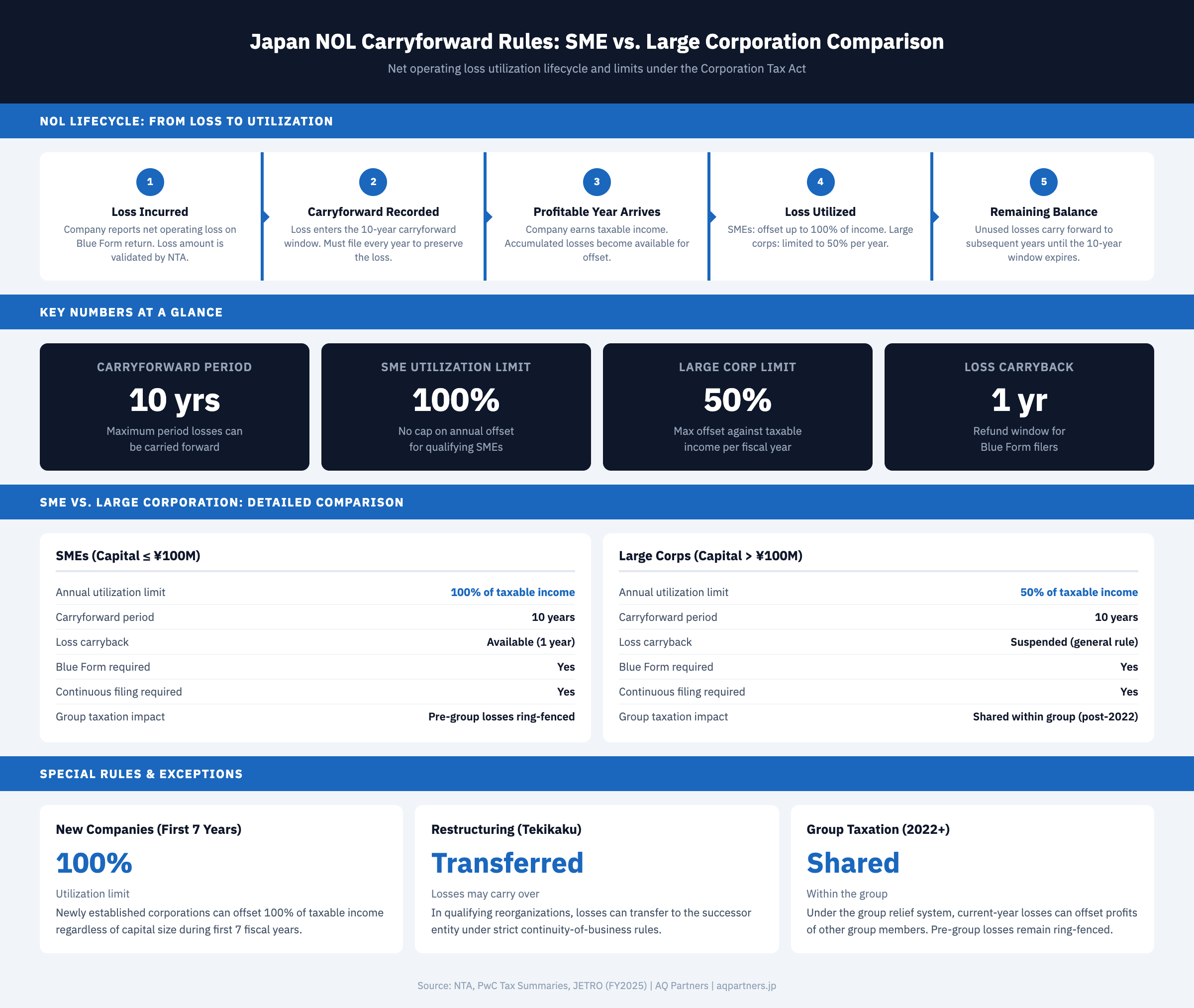

- Japan allows corporations to carry forward net operating losses for up to 10 years, applicable to both national and local tax bases.

- SMEs (capital ≤ ¥100 million) can offset 100% of taxable income with carried-forward losses; large corporations are capped at 50%.

- Only companies filing Blue Form (aoiro) tax returns qualify for loss carryforward and carryback provisions.

- Loss carryback allows SME Blue Form filers to claim a one-year refund against the prior year's tax paid.

- Foreign subsidiaries should plan their capitalization structure, fiscal year timing, and Blue Form application before the first return to maximize NOL benefits.

How Tax Loss Carryforward Works in Japan

Under Japan's Corporation Tax Act (Articles 57–58), when a company's deductible expenses exceed its gross income in a fiscal year, the resulting net operating loss can be carried forward to reduce taxable income in subsequent profitable years. This mechanism applies to both the national corporate tax base and the local enterprise tax base, making it a dual-layer benefit.

The system works on a first-in, first-out (FIFO) basis: the oldest losses must be utilized before more recent ones. A company that incurred losses in Year 1 and Year 3, for example, must exhaust the Year 1 loss completely before applying the Year 3 loss against income.

According to PwC's Japan tax summary, this carryforward provision applies to all categories of net operating losses, including ordinary business losses, capital losses, and losses from asset dispositions—provided they are properly reported on a Blue Form return.

To maintain eligibility, the company must file a corporate tax return for every fiscal year without interruption, even during loss years. A single missed filing can forfeit the entire accumulated loss balance.

Carryforward Period and Utilization Limits

The carryforward period and annual utilization cap are the two most critical variables in NOL planning. Japan's rules differ significantly based on company size, defined by capitalization:

| Rule | SMEs (Capital ≤ ¥100M) | Large Corps (Capital > ¥100M) |

|---|---|---|

| Carryforward period | 10 years | 10 years |

| Annual utilization limit | 100% of taxable income | 50% of taxable income |

| Loss carryback (refund) | Available (1 year) | Suspended (general rule) |

| Blue Form required | Yes | Yes |

| Continuous filing required | Yes | Yes |

| New company exception (first 7 yrs) | 100% (already full) | 100% (overrides 50% cap) |

| Group taxation (post-2022) | Pre-group losses ring-fenced | Shared within group |

The 50% limitation for large corporations was introduced in 2012 and has remained in effect since. Before that change, all corporations could offset 100% of income—a point worth noting when reviewing older tax guidance. The National Tax Agency provides the statutory basis for these rules in its English-language guidance.

For a foreign subsidiary capitalized at over ¥100 million, the 50% cap means it will always pay some tax in profitable years, even if it has substantial accumulated losses. This makes capitalization planning—whether to set capital at or below the ¥100 million threshold—a critical decision at the time of incorporation.

Loss Carryback: The One-Year Refund Option

While carryforward is the more commonly used mechanism, Japan also provides a loss carryback option that allows qualifying companies to apply a current-year loss against the previous year's taxable income and receive a refund of taxes already paid.

How carryback works: If a company paid ¥10 million in corporate tax in Year 1 and then incurred a ¥30 million loss in Year 2, it can apply the loss against Year 1's taxable income and receive a refund of up to ¥10 million. Any remaining loss (¥20 million in this case) carries forward under the standard 10-year rule.

Key conditions for loss carryback:

- The company must be filing a Blue Form return for both the loss year and the preceding year.

- Only SMEs (capital ≤ ¥100 million) are generally eligible. The carryback provision has been suspended for large corporations since 1992, though temporary exceptions have been made during economic crises (such as during COVID-19).

- The carryback refund claim must be filed within the regular filing deadline for the loss year (typically two months after fiscal year-end).

- The refund covers national corporate tax only—local taxes are not eligible for carryback.

For companies that have already been profitable and then face a downturn, the carryback option provides immediate cash flow relief rather than waiting for future profits to absorb the loss.

Blue Form Requirement for Loss Utilization

The Blue Form tax return (青色申告, aoiro shinkoku) is the gateway to virtually all NOL-related provisions in Japan. Without Blue Form status, a corporation cannot carry forward losses, claim carryback refunds, or access several other tax benefits including accelerated depreciation and special reserves.

To obtain Blue Form approval, a company must submit an application to the jurisdictional tax office:

- New companies: Within 3 months of incorporation or by the end of the first fiscal year, whichever comes first.

- Existing companies: By the day before the start of the fiscal year for which approval is sought.

Blue Form approval requires the company to maintain proper accounting books and records in accordance with generally accepted accounting standards. The NTA may revoke Blue Form status if records are found to be unreliable or if the company fails to comply with reporting requirements.

For foreign companies establishing a Japan subsidiary, the Blue Form application should be one of the very first post-incorporation filings—alongside the various opening notifications to the tax office, prefectural office, and municipal office. Missing the deadline means the first fiscal year's losses may not qualify for carryforward. Learn more about the full Blue Form process in our guide to Blue Form tax return benefits and requirements.

Special Rules for New and Restructuring Companies

Japan provides enhanced NOL treatment for certain categories of companies:

Newly Established Corporations

For the first seven fiscal years after incorporation, all corporations—regardless of capital size—can utilize carried-forward losses against 100% of taxable income. This is a critical benefit for large-capital subsidiaries that would otherwise be subject to the 50% limitation.

This seven-year window means a foreign company that incorporates a Japan KK with capital above ¥100 million still gets full loss utilization during its startup phase, when losses are most likely to occur. According to JETRO's investment guide, this provision is specifically designed to reduce barriers for new market entrants.

Corporate Restructurings (Tekikaku Reorganizations)

When a corporation undergoes a qualifying reorganization (適格組織再編, tekikaku soshiki saihen)—such as a merger, corporate split, or share exchange—the accumulated losses of the predecessor entity may transfer to the successor, subject to strict conditions:

- The reorganization must meet the tekikaku (qualifying) criteria, including continuity of business enterprise and continuity of shareholders.

- For mergers, the surviving company generally inherits the losses of the absorbed company.

- Anti-abuse rules restrict loss transfer when the primary purpose of the reorganization is deemed to be tax avoidance.

- Losses incurred before the reorganization may be subject to usage restrictions in the first five years post-reorganization.

Interaction with Group Taxation

Japan replaced its consolidated taxation system with a new group relief system (グループ通算制度, guruupu tsuusan seido) effective April 2022. This change significantly affects how NOLs are treated within corporate groups:

| Aspect | Old Consolidated System | New Group Relief System (2022+) |

|---|---|---|

| Loss sharing | Consolidated at parent level | Individual entity filing with group offset |

| Current-year losses | Offset within consolidated group | Offset against profits of other group members |

| Pre-group losses | Forfeited upon joining | Ring-fenced (usable only against own income) |

| Filing method | Single consolidated return | Individual returns with adjustments |

| Utilization cap (large corp) | 50% of consolidated income | 50% at individual entity level |

| Opt-in requirement | Irrevocable election | Automatic for 100%-owned subsidiaries |

The key change under the group relief system is that pre-group losses are no longer forfeited when a subsidiary joins the group—they are ring-fenced and can only be used against that entity's own income. This is a significant improvement for foreign companies acquiring Japan entities with accumulated losses. The PwC group taxation overview provides additional detail on this transition.

Strategic NOL Planning for Foreign Subsidiaries

Foreign companies entering Japan typically face two to four years of operating losses before reaching profitability. Effective NOL planning during this period can reduce the corporate income tax burden significantly once the business becomes profitable. Here are the core strategies:

1. Capitalize at or Below ¥100 Million

By keeping stated capital at ¥100 million or below, the subsidiary qualifies as an SME for tax purposes, gaining access to 100% loss utilization (no 50% cap), loss carryback eligibility, and reduced tax rates on the first ¥8 million of income. Many foreign companies use a combination of low stated capital plus capital surplus (capital reserve) to fund operations while staying under the threshold.

2. File Blue Form Immediately

Submit the Blue Form application within three months of incorporation. This is non-negotiable. Without it, all startup losses are permanently lost for carryforward purposes.

3. Time the Fiscal Year Strategically

Choose a fiscal year-end that maximizes the carryforward window. If substantial setup costs will be incurred in the first few months, a shorter initial fiscal year may lock in losses earlier and start the 10-year clock. Review the Japan tax filing schedule for important deadlines.

4. File Every Year Without Exception

Even when reporting zero income or continued losses, the annual corporate tax return must be filed on time. A missed year breaks the continuity requirement and can forfeit all accumulated losses.

5. Document Losses Thoroughly

The NTA may audit carryforward balances when they are applied against income. Maintain detailed supporting documentation for the loss year, including all schedules, ledgers, and workpapers. Proper documentation is especially important for tax depreciation claims that contribute to the loss amount.

6. Consider Group Structure Timing

If the Japan subsidiary will eventually join a group taxation arrangement, consider the timing carefully. Losses accumulated before joining the group will be ring-fenced under the new system, which is better than the old consolidated system (where they were forfeited) but still limits flexibility.

For companies navigating Japan's corporate tax system for the first time, our comprehensive tax filing and compliance guide covers the full filing process, from registration through annual returns.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.