Payroll Compliance Risks Foreign Companies Miss

Key Takeaways

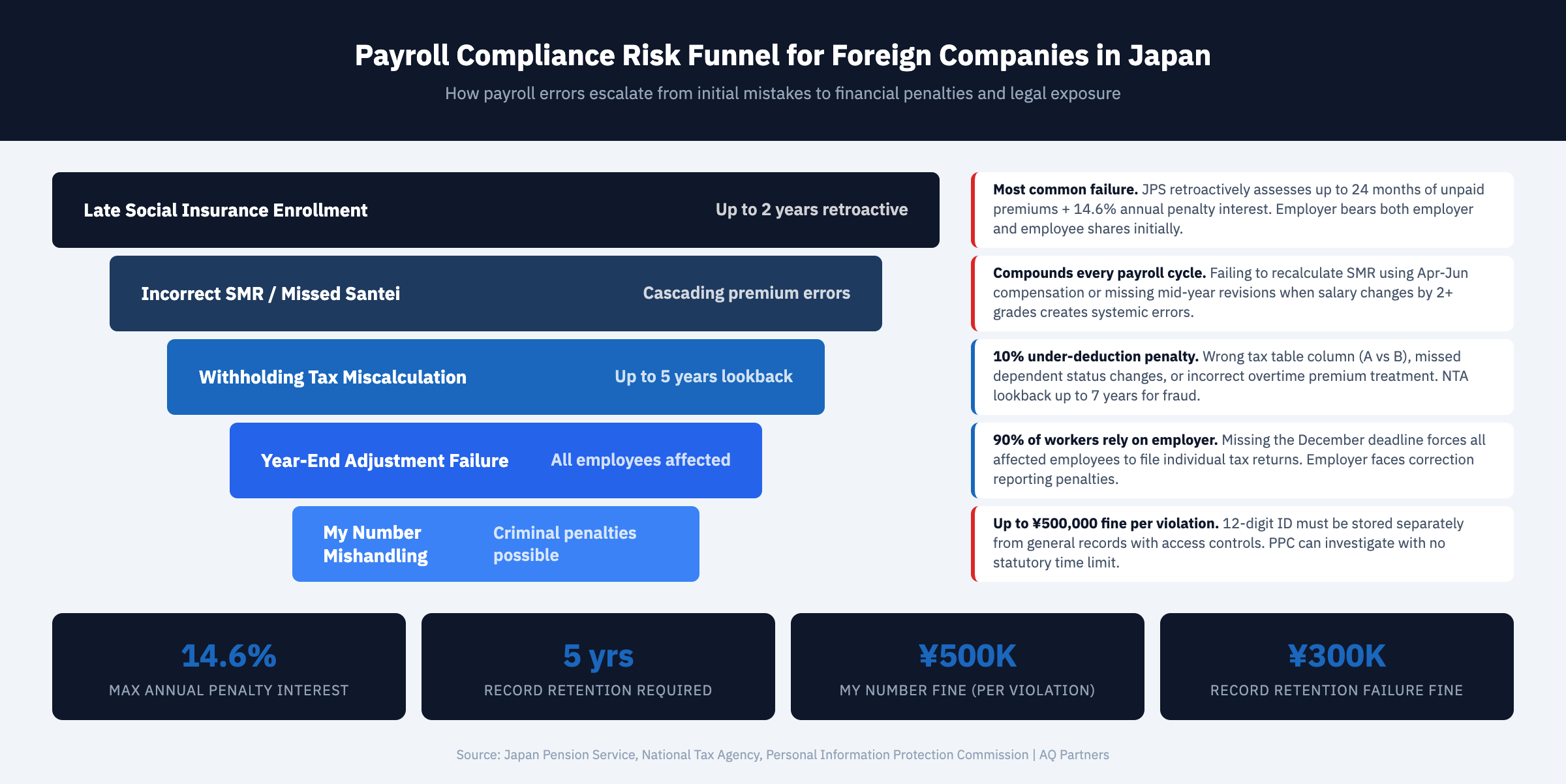

- Late social insurance enrollment is the most common payroll compliance failure among foreign companies in Japan — the Japan Pension Service can retroactively assess up to two years of unpaid premiums plus penalties when companies delay enrollment. According to the Japan Pension Service, all employees working 30 or more hours per week must be enrolled from their first day of employment.

- Incorrect standard monthly remuneration (hyojun getsugaku hoshu) leads to systemic premium errors — failing to perform the annual September revision (santei) based on April-June compensation, or missing mid-year revisions when salary changes by two or more grades, compounds errors across every subsequent payroll cycle. The Japan Pension Service conducts audits specifically targeting SMR miscalculations.

- Year-end adjustment (nenmatsu chosei) errors or missed deadlines create tax discrepancies for every employee — employers who fail to complete year-end adjustment by the December payroll force all affected employees to file individual tax returns and may face penalties from the tax office. Approximately 90% of Japanese salaried workers rely on employer-processed nenmatsu chosei for tax compliance.

- My Number (individual number) mishandling carries both compliance penalties and data breach risks — employers must collect, securely store, and properly use My Number for tax and social insurance filings. The Personal Information Protection Commission can impose administrative orders and penalties of up to ¥500,000 for improper My Number handling under the Act on the Use of Numbers.

- Payroll record retention failures become critical during labor inspections or tax audits — employers must retain wage ledgers, attendance records, and payroll calculation documents for five years under the Labor Standards Act. Missing records shift the burden of proof to the employer in wage disputes, often resulting in unfavorable outcomes.

Why Payroll Compliance Deserves Separate Attention from General Labor Law

Payroll compliance risks in Japan are the specific regulatory failures related to wage calculation, tax withholding, social insurance premium management, and payroll record keeping — distinct from broader labor law issues such as working hours, harassment, or dismissal procedures. Foreign companies often conflate payroll compliance with general HR compliance, leading to blind spots in areas where financial penalties are both quantifiable and retroactive.

While Japan labor compliance risks cover the full spectrum of employment law, this article focuses narrowly on the payroll-specific failures that trigger financial penalties: social insurance enrollment gaps, withholding miscalculations, reporting deadline failures, and data handling violations. These risks are particularly acute for foreign companies because payroll errors in Japan typically compound over time — a single misconfigured social insurance grade affects every payroll cycle until corrected, and corrections often trigger retroactive assessments.

Social Insurance Enrollment Failures and Late Registration Penalties

Failing to enroll employees in social insurance from their employment start date is the single most financially consequential payroll compliance error — the Japan Pension Service can retroactively assess up to 24 months of unpaid premiums for both employer and employee shares.

Foreign companies frequently underestimate the scope of social insurance obligations. Every employee working 30 or more hours per week (or three-quarters of the standard working hours at that workplace) must be enrolled in health insurance and employees' pension from day one. Since October 2022, companies with 101 or more employees must also enroll part-time workers who work 20+ hours per week and earn ¥88,000 or more monthly — this threshold dropped further to companies with 51+ employees in October 2024.

The consequences of non-enrollment extend beyond back-premiums. Employees who should have been enrolled but were not may have gaps in their pension records, affecting future benefit calculations. Health insurance gaps leave employees (and their dependents) without coverage, potentially resulting in employer liability for medical costs. The Japan Pension Service has intensified enforcement, conducting on-site audits and cross-referencing enrollment data with tax withholding reports to identify discrepancies. According to PwC's Japan tax summary, social insurance costs represent approximately 15-16% of gross salary for employers, making retroactive assessments substantial.

| Payroll Compliance Risk | Penalty / Consequence | Detection Method | Lookback Period |

|---|---|---|---|

| Late social insurance enrollment | Retroactive premiums + 14.6% annual penalty interest | JPS audit, tax cross-reference | Up to 2 years |

| Incorrect SMR / missed santei revision | Premium shortfall recovery + interest | Annual JPS audit | Up to 2 years |

| Withholding tax miscalculation | 10% under-deduction penalty + delinquency interest | NTA tax audit | Up to 5 years (7 for fraud) |

| Missed year-end adjustment deadline | Employee tax filing burden + employer correction reporting | Tax office review of withholding summaries | Current year + correction filing |

| My Number mishandling | Up to ¥500,000 fine; criminal penalties possible | PPC investigation, data breach report | No statutory limit |

| Payroll record retention failure | ¥300,000 fine; adverse inference in disputes | Labor inspection, employee complaint | 5-year retention requirement |

| Late withholding tax remittance | 10% non-deposit penalty + delinquency interest | NTA automated matching | Up to 5 years |

| Bonus reporting failure | Premium reassessment + administrative penalty | JPS cross-check with tax filings | Up to 2 years |

Standard Monthly Remuneration (SMR) Errors and Their Cascading Impact

Miscalculating or failing to update the standard monthly remuneration (hyojun getsugaku hoshu) creates a cascading error that affects health insurance premiums, pension contributions, and employment insurance calculations across every payroll cycle until corrected.

The SMR is not simply the employee's monthly salary — it is a standardized grade determined by averaging the employee's compensation (including allowances and overtime) over the three months from April through June. This annual "santei" process results in a new SMR effective from September. Foreign companies frequently make errors by using base salary alone rather than total compensation, excluding taxable allowances, or failing to perform the santei process altogether.

A mid-year revision (zuiji kaitei) must also be filed when an employee's fixed compensation changes by an amount that would shift them two or more SMR grades. Companies that implement pay raises or restructure allowances without filing the corresponding SMR revision will underpay premiums until the next santei cycle — and face retroactive corrections when the discrepancy is discovered. For a comprehensive overview of how payroll works in Japan, including the role of SMR in the gross-to-net calculation, see our companion guide.

Withholding Tax Errors and Year-End Adjustment Pitfalls

Income tax withholding errors accumulate across every payroll cycle and are reconciled — or exposed — during the year-end adjustment process, making accurate monthly withholding and timely nenmatsu chosei equally critical.

Common withholding errors include: applying the wrong tax table column (Column A for employees who submitted a dependency declaration versus Column B for those who did not), failing to account for changes in dependent status mid-year, incorrectly treating tax-exempt allowances as taxable, and miscalculating overtime premium amounts. The National Tax Agency prescribes specific withholding tables that must be applied correctly each month.

Year-end adjustment failures are particularly problematic. Employers must collect employee deduction declarations (insurance premiums, housing loan certificates, dependent information) and process the adjustment with the December or January payroll. Companies that miss this deadline must report the failure to the tax office and may face penalties. Affected employees are forced to file individual tax returns — an unusual burden in Japan where approximately 90% of salaried workers settle their entire tax obligation through employer-processed nenmatsu chosei.

My Number Compliance and Data Security Requirements

My Number (individual number) compliance requires employers to collect, store, and use each employee's 12-digit identification number exclusively for tax and social insurance purposes — with strict data protection requirements enforced by the Personal Information Protection Commission.

Foreign companies must collect My Number from employees and their dependents for use on tax withholding reports, social insurance filings, and related government submissions. The data must be stored separately from general employee records with access controls limiting visibility to authorized personnel only. When an employee departs and the retention period expires, the company must securely destroy the My Number records.

The Act on the Use of Numbers to Identify a Specific Individual (commonly called the My Number Act) imposes penalties of up to ¥500,000 for improper handling and potential criminal penalties for intentional misuse or unauthorized disclosure. The Personal Information Protection Commission has authority to conduct investigations and issue administrative orders. Foreign companies accustomed to less stringent personal data handling practices in other jurisdictions must implement specific My Number management protocols — including designated storage systems, access logs, and disposal procedures.

Payroll Record Retention and Documentation Risks

Japanese labor law mandates that employers retain wage ledgers, attendance records, and payroll calculation documents for a minimum of five years — and missing records create a presumption against the employer in any wage dispute or labor inspection.

The Labor Standards Act (Article 109) requires employers to maintain a "wage ledger" (chingin dai cho) for each employee documenting: name, gender, salary calculation method, salary calculation period, number of working days, working hours, overtime/holiday/late-night work hours, basic pay, and each allowance. The retention period was extended from three to five years effective April 2020, with a current transitional provision permitting three-year retention while the five-year standard phases in fully.

During labor inspections, the Labor Standards Inspection Office will request these records. Foreign companies that maintain payroll records only in their home-country systems — or that fail to keep Japanese-format records — face significant risk. In wage disputes before the labor tribunal, incomplete employer records lead to adverse inferences, meaning the employee's claimed hours and compensation will be presumed accurate. Companies using Japanese payroll software benefit from automated record generation that meets these requirements. For comprehensive guidance on integrating payroll compliance into your broader HR strategy, see our Japan HR compliance strategies guide.

Frequently Asked Questions

How far back can the Japan Pension Service assess retroactive social insurance premiums?

The Japan Pension Service can retroactively assess up to two years of unpaid social insurance premiums. This includes both the employer and employee shares, plus delinquency interest calculated at up to 14.6% annually on overdue amounts. The assessment period runs from the date the employee should have been enrolled, and the employer bears responsibility for both shares initially — though they may deduct the employee's share from future wages under certain conditions.

What happens if we miss the year-end adjustment deadline?

If the employer fails to complete year-end adjustment by the deadline (typically processed with December payroll, with withholding certificates due to the tax office by January 31), affected employees must file individual tax returns (kakutei shinkoku) by March 15 to reconcile their income tax. The employer may face a non-compliance penalty from the tax office and must still submit corrected withholding summary reports. This situation is disruptive for employees who are unaccustomed to filing returns and creates reputational risk for the employer.

Can we store My Number in our global HR system?

Storing My Number in global HR systems is permissible only if the system meets Japan's data protection requirements: access must be restricted to authorized personnel handling tax and social insurance filings, the data must be stored separately from general employee information (logically or physically), access logs must be maintained, and cross-border transfer must comply with the Act on Protection of Personal Information. Many foreign companies choose to store My Number exclusively in their Japanese payroll software or with their payroll service provider to reduce compliance risk.

Payroll compliance in Japan requires systematic attention to enrollment deadlines, calculation accuracy, and record keeping. For foreign companies managing these obligations alongside broader operational complexity, AQ Partners provides integrated payroll compliance management that addresses each of these risk areas. Contact us to review your current payroll compliance posture.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.