Compliance Failure in Japan: Penalties & Risks

Key Takeaways

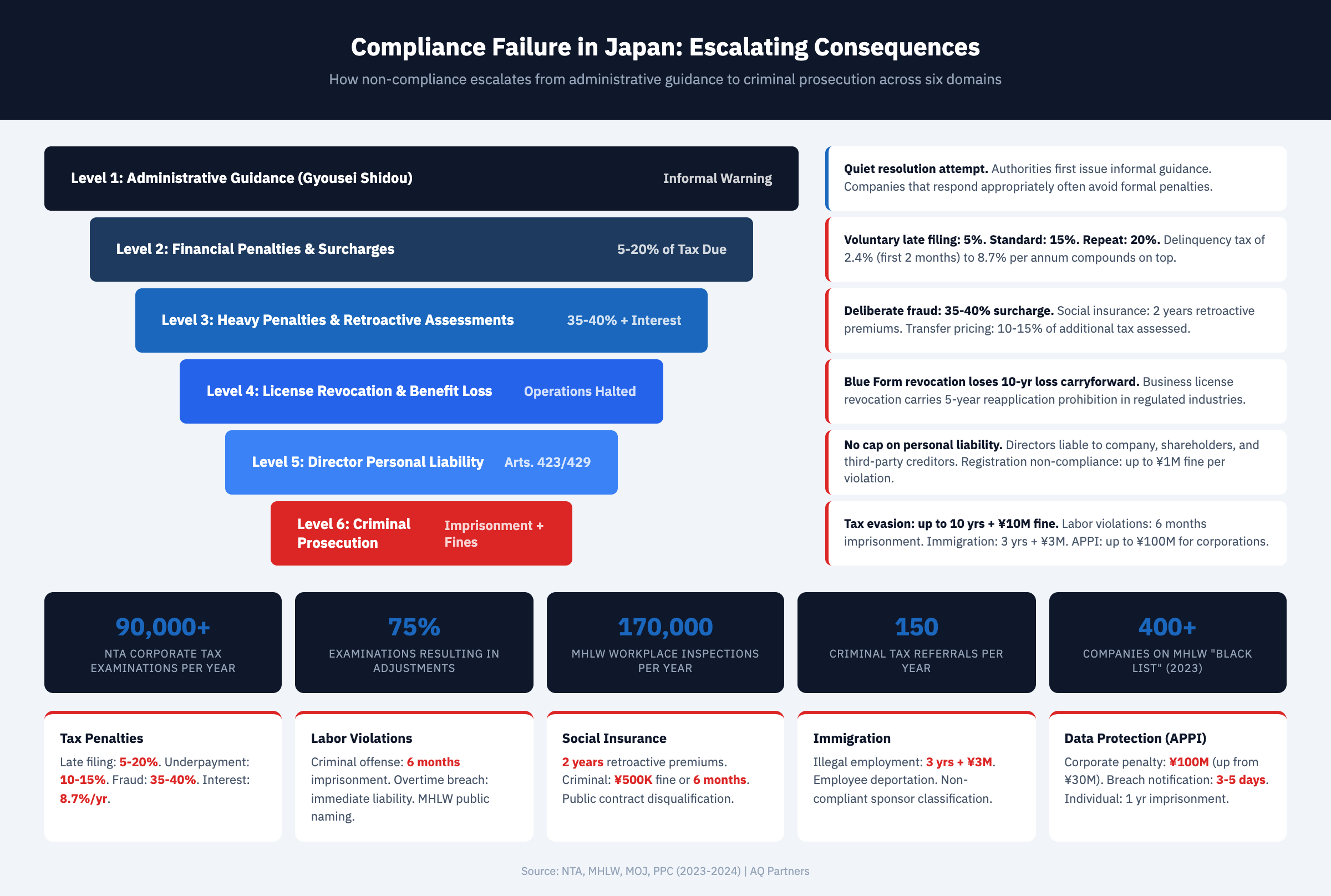

- Tax compliance failures in Japan trigger escalating penalties from 5% to 40% of tax owed — voluntary late filing within one month incurs a 5% surcharge, standard late filing 15%, repeat offenses 20%, and deliberate fraud 35–40%. The NTA also imposes daily interest charges at approximately 8.7% per annum on unpaid balances (NTA Penalty Schedule, 2024).

- Directors face personal liability for compliance failures under the Companies Act — Articles 423 and 429 hold directors liable for damages caused by negligent failure to supervise the company's legal obligations. Courts have ordered individual directors to pay millions of yen in damages to creditors and the company for compliance oversights.

- Labor law violations can result in criminal prosecution of company officers — the Labor Standards Act prescribes penalties of up to six months' imprisonment or fines of 300,000 yen per offense for violations of overtime limits, wage payment rules, or minimum working conditions. Repeat violations or systemic non-compliance escalate to public naming on the MHLW's "Black Company" list.

- Social insurance non-enrollment exposes companies to two years of retroactive premium assessments — the Japan Pension Service can demand back-premiums for both employer and employee shares, plus penalties. Criminal sanctions under the Health Insurance Act include up to six months' imprisonment or fines of 500,000 yen (Health Insurance Act, Article 208).

- Business license revocation halts operations entirely — companies found operating without required permits face immediate cease-and-desist orders, criminal penalties, and potential deregistration. In regulated industries such as construction, financial services, and staffing, license revocation carries a mandatory five-year waiting period before reapplication is permitted.

Understanding Compliance Failure Consequences in Japan

Compliance failure in Japan refers to the situation where a company operating within Japanese jurisdiction fails to meet one or more of its legal, regulatory, or administrative obligations — whether through oversight, misunderstanding, or deliberate non-compliance. The consequences range from financial penalties and administrative sanctions to criminal prosecution of individual directors, business suspension, and reputational damage that can undermine market position for years.

Japan's regulatory enforcement approach differs from many Western jurisdictions in important ways. Authorities tend to pursue quiet resolution through administrative guidance (gyousei shidou) as a first step, but escalate decisively when companies fail to respond. The National Tax Agency (NTA) conducts over 90,000 corporate tax examinations annually, with approximately 75% resulting in some form of adjustment. The MHLW's Labour Standards Inspection Office performs approximately 170,000 workplace inspections per year (MHLW Annual Report, 2023). Foreign companies receive no special leniency — ignorance of Japanese regulations is not a recognized defense.

This guide details the specific consequences of compliance failure across each major regulatory domain, helping foreign companies understand the real financial and operational risks of gaps in their compliance programs. For a complete overview of what compliance obligations exist, see our guide to compliance obligations for companies in Japan. For a practical approach to preventing these failures, see our guide on building a sustainable compliance framework.

Tax Compliance Failure: Penalties, Interest, and Criminal Prosecution

Tax non-compliance in Japan triggers a tiered penalty system that escalates based on the severity, nature, and recurrence of the violation — from modest surcharges for minor delays to criminal prosecution for deliberate evasion.

| Violation Type | Penalty Rate / Amount | Additional Consequences |

|---|---|---|

| Voluntary late filing (within 1 month) | 5% of tax due | Interest accrues from original due date at ~2.4% for first 2 months |

| Standard late filing (after 1 month) | 15% of tax due | Interest at ~8.7% per annum on outstanding balance |

| Repeat late filing (within 5 years of prior penalty) | 20% of tax due | Triggers increased examination frequency |

| Underpayment (standard) | 10% of additional tax assessed | Applied when NTA examination reveals underreported income |

| Significant underpayment | 15% on portion exceeding 10M yen or 10% of original tax | Higher rate on amount above threshold; intensified future scrutiny |

| Deliberate fraud / evasion | 35–40% of evaded tax | Criminal prosecution; up to 10M yen fine and/or 10 years imprisonment |

| Withholding tax failure | 10% of tax that should have been withheld | Employer bears full liability regardless of employee cooperation |

| Transfer pricing non-compliance | 10–15% of additional tax assessed | Retroactive documentation given less credibility; increased CbCR scrutiny |

| Blue Form revocation | Loss of all Blue Form benefits | Eliminates 10-year loss carryforward; no recovery for previously unused losses |

| Consumption tax late filing | 15–20% penalty plus interest | No extension available; the most rigid deadline in Japan's tax system |

The NTA refers approximately 150 cases annually for criminal prosecution (NTA Annual Report, 2024), targeting companies and individuals involved in deliberate concealment of income, fabricated deductions, or systematic evasion schemes. Criminal tax cases carry a statute of limitations of seven years — longer than the standard three years for civil reassessment. According to PwC's Worldwide Tax Summaries, the combined financial impact of penalties, interest, and additional tax can increase the original tax liability by 50% or more in severe cases.

Blue Form revocation deserves particular emphasis. This administrative action — triggered by significant accounting irregularities, deliberate evasion, or chronic late filing — eliminates a company's access to 10-year loss carryforward, special depreciation provisions, and enhanced deductions. For startups and growth-stage companies that have accumulated losses, revocation can convert years of tax-free operation into immediate taxable exposure. For more detail on the tax penalty structure, see our tax filing and compliance guide.

Labor and Employment Law Violations

Labor law violations in Japan carry criminal penalties directed at company officers personally, making them among the most consequential compliance failures for foreign company management.

The Labor Standards Act treats most violations as criminal offenses, not merely administrative matters. Failure to pay overtime premiums at the prescribed rates (25% for regular overtime, 35% for holiday work, 50% for late-night overtime) constitutes a criminal offense under Article 119, carrying up to six months' imprisonment or fines of 300,000 yen. The 2019 work-style reform imposed hard caps on overtime hours — companies exceeding the limits of 100 hours per month or 720 hours per year face immediate criminal liability.

The MHLW publishes an annual "Black Company" list (roudou kijun kankeimeirei shi ihan kigyou) naming companies found to have committed significant labor law violations. Appearing on this publicly accessible list causes substantial reputational damage, affecting both customer relationships and talent recruitment. In 2023, the MHLW listed over 400 companies on the public violations database, with penalties ranging from administrative guidance to criminal referral.

Wrongful Dismissal and Unfair Labor Practices

Japan's employment protection framework makes dismissal of regular employees extremely difficult. Courts apply the "doctrine of abusive dismissal" (kaiko ken ranyou no housoku) under Article 16 of the Labor Contract Act, requiring employers to demonstrate both objectively reasonable grounds and social appropriateness. Failed dismissals typically result in reinstatement orders with full back pay — which can accumulate to millions of yen if litigation extends over several years. Foreign companies accustomed to at-will employment often underestimate this risk. For a deeper analysis, see our guide on Japan labor compliance risks.

Social Insurance Non-Compliance

Failure to enroll employees in Japan's mandatory social insurance programs triggers retroactive premium assessments, criminal penalties, and potential disqualification from public contracts and government programs.

The Japan Pension Service has intensified enforcement, cross-referencing tax withholding records against social insurance enrollment data to identify non-enrolled companies. When non-enrollment is discovered, the Pension Service assesses retroactive premiums for up to two years — covering both employer and employee shares. Companies must pay the full amount and then attempt to recover the employee's share through salary deductions, which requires employee consent.

Criminal penalties under the Health Insurance Act (Article 208) include up to six months' imprisonment or fines of 500,000 yen for willful failure to enroll employees. Companies bidding on government contracts may also be disqualified, as public procurement increasingly requires proof of social insurance compliance.

Director Liability and Corporate Governance Failures

Japan's Companies Act imposes personal liability on directors for compliance failures — making director exposure one of the most significant but often underestimated risks for foreign company officers.

Under Article 423 of the Companies Act, directors are liable to the company for damages resulting from their failure to perform duties with due care. Under Article 429, directors face liability to third parties (including creditors and employees) for damages caused by gross negligence or willful misconduct. Japanese courts interpret these provisions broadly — a director who fails to implement adequate compliance systems or ignores warning signs can be held personally liable.

Registration non-compliance carries its own penalties. Failure to file changes to the commercial register within the 14-day statutory period triggers fines of up to 1 million yen per violation under Article 976. Chronic failure to maintain accurate registration can lead to compulsory dissolution proceedings initiated by the Legal Affairs Bureau. For companies structured as branches of foreign entities, the parent company bears unlimited liability for the branch's compliance failures in Japan — meaning overseas directors can be exposed to Japanese regulatory enforcement.

Immigration, Data Protection, and Licensing Violations

Immigration, data protection, and licensing violations each carry distinct penalties — but share a common characteristic: they can halt business operations entirely, not just impose financial costs.

Immigration Violations

Companies that knowingly employ workers engaged in activities outside their permitted visa status face penalties of up to three years' imprisonment or fines of 3 million yen under the Immigration Control and Refugee Recognition Act. Even unintentional violations — such as reassigning a visa holder to duties not covered by their status — can result in the employee's deportation and the company's classification as a non-compliant sponsor, which makes future visa applications significantly more difficult. Since 2019, the Immigration Services Agency has increased scrutiny of companies employing workers under the Specified Skilled Worker categories, conducting regular audits and requiring detailed activity reports.

APPI Data Protection Violations

Violations of the Act on Protection of Personal Information carry penalties of up to 100 million yen for corporations since the 2022 amendments — a significant increase from the previous 30 million yen cap. Individual offenders face up to one year of imprisonment or fines of 1 million yen. The Personal Information Protection Commission can issue public administrative orders, and non-compliance with a PPC order constitutes a separate criminal offense. Data breach incidents require notification to the PPC and affected individuals within 3–5 days of discovery, with failure to notify treated as an aggravating factor.

Business License Violations

Operating without a required industry license is a criminal offense in most regulated sectors. Construction companies operating without a license face fines of up to 3 million yen and a mandatory five-year prohibition from reapplication. Financial services companies operating without FSA registration face criminal prosecution. Temporary staffing agencies (hakengyo) operating without MHLW registration face fines and criminal penalties. License revocation — triggered by compliance violations within the regulated activity — carries the same five-year reapplication prohibition, effectively forcing the company to exit the market segment entirely.

Reputational and Operational Impact

Beyond legal penalties, compliance failures inflict reputational and operational damage that can undermine a foreign company's position in the Japanese market for years — affecting hiring, partnerships, and customer trust.

Japan's business culture places exceptional weight on trust and reliability. Compliance failures become permanently discoverable through the MHLW's public violations database, NTA press releases on criminal tax cases, and media coverage. According to JETRO's 2024 Survey on Business Conditions of Foreign-Affiliated Companies, 38% of respondents cited regulatory compliance as their primary operational concern.

Operational disruption compounds the reputational impact. Tax examinations consume weeks of management time. Labour Standards investigations may require immediate operational changes — such as halting overtime — that disrupt production. Immigration violations can result in loss of key employees through deportation. License revocation forces immediate cessation of regulated activities, potentially eliminating entire revenue streams.

The cumulative cost of non-compliance almost always exceeds the cost of maintaining proper compliance systems. For practical guidance on building the systems that prevent these outcomes, see our guide on building a sustainable compliance framework for Japan operations. For the complete picture of what obligations exist, see our comprehensive guide to compliance obligations in Japan.

Frequently Asked Questions

Can directors of a Japanese subsidiary be held personally liable for compliance failures?

Yes. Under Articles 423 and 429 of the Companies Act, directors face personal liability for damages resulting from negligent failure to supervise the company's legal obligations. This includes failure to implement compliance systems, failure to act on known issues, and inadequate delegation of compliance responsibilities. Japanese courts have interpreted these duties broadly, and individual directors have been ordered to pay damages to both the company and third parties (including creditors and employees). Directors of branch offices should note that the parent company — and by extension, its officers — bears unlimited liability for the branch's obligations in Japan.

What happens if a foreign company is late on its first tax filing in Japan?

A first-time late filing incurs a penalty of 15% of the tax due, reduced to 5% if the company voluntarily files within one month and pays the full tax amount. Late payment interest begins accruing from the original due date at approximately 2.4% for the first two months, rising to approximately 8.7% thereafter. The more critical risk for new companies is missing the Blue Form application deadline (three months after incorporation), which permanently forfeits loss carryforward benefits for the first fiscal year. Consumption tax permits no extension and triggers automatic penalties upon any delay.

How does Japan's "Black Company" list affect foreign businesses?

The MHLW publishes a public database of companies found to have committed significant labor law violations. Being listed causes immediate reputational damage: prospective employees, business partners, and clients can discover the listing through public searches. The list includes the company name, violation details, and the enforcing office. Listings remain publicly accessible for approximately one year after publication. For foreign companies trying to recruit Japanese talent, appearing on the list substantially increases hiring difficulty in an already competitive labor market.

Compliance failures in Japan carry consequences that compound across domains — a tax examination may reveal social insurance non-enrollment, which triggers a Pension Service investigation, which uncovers unreported employment that raises immigration concerns. Preventing this cascade requires a coordinated compliance approach across all regulatory areas. AQ Partners provides integrated back office services covering accounting, tax coordination, payroll, HR administration, and compliance support — designed specifically to prevent the gaps that lead to enforcement actions. Contact us at hello@aqpartners.jp to discuss how we can protect your Japan operations.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.