Corporate Governance Requirements for Japan Entities

Key Takeaways

What Corporate Governance Means for Foreign-Owned Entities in Japan

Corporate governance in Japan refers to the legal framework of rules, structures, and processes that govern how a company is directed and controlled — specifically the obligations imposed by the Companies Act (Kaisha-ho) on directors, shareholders, and auditors of Japanese business entities. For foreign companies operating a subsidiary in Japan, corporate governance determines what meetings you must hold, what officers you must appoint, what documents you must file, and what records you must keep.

The practical reality differs dramatically depending on entity type and size. A publicly listed Japanese company faces extensive requirements including independent directors, audit committees, and detailed disclosures under Japan Exchange Group's Corporate Governance Code. A small foreign-owned KK with a single corporate shareholder faces a fraction of those obligations. This guide focuses on the governance requirements that actually apply to a typical foreign subsidiary.

Non-compliance carries real consequences. According to the Ministry of Justice's official English translation of the Companies Act, penalties for failing to register required changes can reach ¥1 million. Getting governance right from the start protects both the entity and its officers.

KK vs. GK: How Entity Type Determines Governance Structure

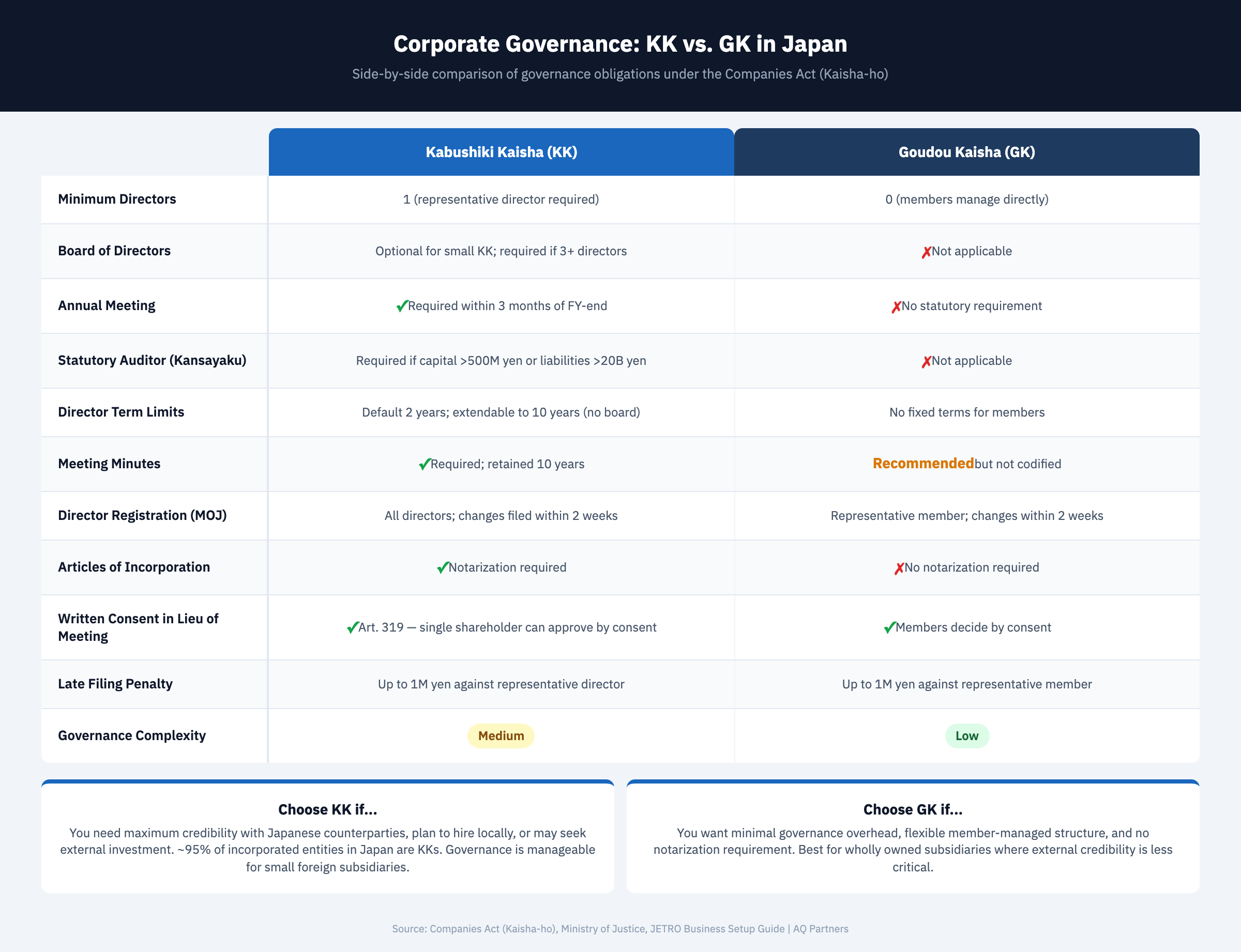

The choice between a Kabushiki Kaisha (KK) and a Goudou Kaisha (GK) fundamentally shapes governance obligations — KKs follow a shareholder-director model with mandatory meetings and filings, while GKs operate under a flexible member-managed structure with minimal statutory governance.

Governance FeatureKabushiki Kaisha (KK)Goudou Kaisha (GK)Minimum Directors1 (representative director required)0 (members manage directly)Board of DirectorsOptional for small KK; required if 3+ directors electedNot applicableShareholder/Member MeetingsAnnual meeting legally required within 3 months of fiscal year-endNo statutory meeting requirement; members decide by consentStatutory Auditor (Kansayaku)Required for "large companies" (capital >¥500M or liabilities >¥20B)Not applicableDirector Term LimitsDefault 2 years; extendable to 10 years for non-board KKsNo fixed terms for membersMinutes/RecordsShareholder and board meeting minutes required; retained 10 yearsMember consent records recommended but not strictly codifiedDirector Registration (MOJ)All directors registered; changes filed within 2 weeksRepresentative member registered; changes filed within 2 weeksArticles of IncorporationNotarization required at incorporationNo notarization required

For most foreign companies, the choice between KK and GK depends on factors beyond governance — including credibility with Japanese business partners. KKs represent approximately 95% of all incorporated entities in Japan, and foreign parent companies frequently choose the KK structure for its familiarity to Japanese counterparties.

Board of Directors and Director Appointment Requirements

A small KK needs only one director and no formal board — the "board" requirement applies only when a KK elects three or more directors, at which point a board of directors (torishimariyaku-kai) becomes mandatory.

The parent company, acting as sole shareholder, passes a resolution appointing directors. This resolution must be documented in meeting minutes, and directors must be registered with the Legal Affairs Bureau (homukyoku) within 2 weeks under Companies Act Article 915. Director terms default to 2 years, but KKs without a board can extend terms to 10 years through their articles of incorporation. According to JETRO's business setup guidance, this 10-year extension is one of the most frequently used simplification options for small KKs.

Every KK must designate at least one representative director (daihyo torishimariyaku), who holds authority to act on behalf of the company, sign contracts, and represent it legally. For a single-director KK, that director automatically becomes the representative director. Since the 2015 Companies Act revision, a non-resident can serve as sole representative director — though maintaining a Japan-resident director remains practically advantageous for day-to-day filings and banking relationships.

Shareholder Meetings and Minutes Requirements

Every KK must convene an annual shareholders' meeting within 3 months of its fiscal year-end — a non-negotiable requirement under Companies Act Article 296, regardless of company size or shareholder count.

For a wholly owned subsidiary, the annual meeting agenda covers: approval of financial statements, appointment or reappointment of directors (when terms expire), and profit distribution decisions. Companies Act Article 319 permits single-shareholder companies to approve proposals via written consent instead of a physical meeting. Even so, the company must prepare a document deemed equivalent to minutes and retain it for 10 years.

Extraordinary shareholders' meetings may be convened when decisions exceed directors' authority — including amendments to articles of incorporation (requiring a two-thirds supermajority under Article 309), capital changes, mergers, and director removal. Meeting notices must be sent at least 2 weeks before a board-KK meeting, or 1 week before a non-board KK meeting. Single-shareholder companies can waive notice entirely.

Meeting minutes must include: date and location, matters discussed and outcomes, names of attendees, and the chairperson's name. Under Article 369, a director who does not voice an objection in board meeting minutes is presumed to have agreed — making accurate minute-taking a matter of personal liability protection. Beyond minutes, companies must maintain a shareholder registry, preserve accounting books for 10 years, and make financial statements available for inspection. All governance filings require the company's registered seal — the corporate inkan system intersects directly with governance compliance.

Statutory Auditor (Kansayaku): When Required and What They Do

A statutory auditor (kansayaku) is required only for "large companies" — KKs with stated capital exceeding ¥500 million or total liabilities exceeding ¥20 billion, per Companies Act Article 328. The vast majority of foreign-owned subsidiaries fall well below these thresholds.

When required, the kansayaku reviews directors' execution of duties, audits financial statements, attends board meetings, and reports findings to shareholders. The term of office is 4 years. For large KKs, the Companies Act further requires an accounting auditor (kaikei kansanin) — a CPA or audit firm — and a kansayaku board for large companies with a formal board of directors. According to PwC's analysis of Japan's corporate governance framework, approximately 3,800 listed companies maintain kansayaku boards or have transitioned to the "company with audit and supervisory committee" structure introduced in the 2015 amendment.

For a small foreign-owned KK: unless your stated capital exceeds ¥500 million or liabilities exceed ¥20 billion, you do not need a kansayaku, accounting auditor, or audit committee.

Registered Director Changes and MOJ Filing Procedures

Any change in a KK's directors must be registered with the Legal Affairs Bureau within 2 weeks of the effective date under Companies Act Article 915 — failure to file can result in a fine of up to ¥1 million against the representative director.

Required documents include: a commercial registration application form, shareholder meeting minutes evidencing the resolution, a letter of acceptance from the incoming director, the incoming representative director's personal seal certificate (inkan shomei-sho), and the company's registered seal impression. Registration fees are ¥30,000 per filing (or ¥10,000 via the Ministry of Justice's online registry system).

Filing EventDeadlineFiling FeeKey DocumentsNew Director Appointment2 weeks from resolution¥30,000 (¥10,000 online)Shareholder minutes, acceptance letter, seal certificateDirector Resignation2 weeks from effective date¥30,000 (¥10,000 online)Resignation letter, board or shareholder minutesRepresentative Director Change2 weeks from resolution¥30,000 (¥10,000 online)Shareholder minutes, new rep's seal certificate and registrationDirector Term Expiry & Reappointment2 weeks from reappointment¥30,000 (¥10,000 online)Shareholder minutes, acceptance letterArticles of Incorporation Amendment2 weeks from special resolution¥30,000Special resolution minutes (two-thirds majority)Head Office Relocation (Same Jurisdiction)2 weeks from effective date¥30,000Board or shareholder minutes, new address proofHead Office Relocation (Different Jurisdiction)2 weeks from effective date¥60,000 (¥30,000 x 2)Board or shareholder minutes, new address proofCapital Increase2 weeks from payment¥30,000 or 0.7% of increase (whichever greater)Shareholder minutes, payment certificate, capital calculation docs

A common scenario involves replacing the Japan-based representative director. This requires a shareholder resolution, resignation letter from the outgoing director, acceptance letter from the incoming director, the new director's seal certificate, and filing within 2 weeks. When directors reside overseas, coordinating these documents across time zones adds practical complexity that companies should plan for in advance.

Practical Governance Reality for Small Foreign Subsidiaries

For a typical foreign-owned KK with one to three directors and a single corporate shareholder, the annual governance cycle is predictable and manageable — far removed from the compliance demands placed on listed companies.

What is legally required versus what is recommended best practice deserves clear distinction. The Companies Act requires: annual shareholder meetings, proper minutes, director registration, and financial statement preparation. It does not require: internal audit functions (unless classified as a large company), independent directors (unless listed), corporate governance reports (unless listed), or sustainability disclosures. The Japan Exchange Group's Corporate Governance Code applies exclusively to listed companies and has no bearing on private foreign subsidiaries.

Foreign parent companies frequently impose their own governance standards through internal policies. A U.S. parent subject to SOX compliance may require internal controls beyond what the Companies Act demands. European parents may apply ESG reporting standards. These internal requirements create additional governance work companies should anticipate when budgeting for Japan operations. For guidance on structuring your entity to minimize governance complexity, see our overview of entity structuring strategy for Japan market entry, and review the post-incorporation filing requirements that begin immediately after registration.

Frequently Asked Questions

Does a small foreign-owned KK need a statutory auditor?

No. Under Companies Act Article 328, a kansayaku is required only for KKs with stated capital exceeding ¥500 million or total liabilities exceeding ¥20 billion. A typical foreign-owned subsidiary with capital of ¥5 million to ¥50 million is exempt.

Can a KK hold its annual meeting by written consent?

Yes. Companies Act Article 319 allows shareholders to approve proposals without a physical meeting when all shareholders consent in writing. The company must still prepare minutes-equivalent documentation and retain it for 10 years. This is the standard approach for single-shareholder foreign subsidiaries.

What happens if director registration is filed late?

The representative director faces a potential fine of up to ¥1 million under Companies Act Article 976. An unregistered director change also causes practical complications — the commercial registry will not reflect the current officer, affecting bank signatories, tax filings, and contract execution.

How long can director terms be extended?

A KK without a board of directors can extend terms to 10 years through its articles of incorporation under Companies Act Article 332. KKs with a formal board are limited to the standard 2-year term. Most small foreign-owned KKs adopt the 10-year term to minimize reappointment costs.

Navigating corporate governance for a Japanese subsidiary does not need to be complicated, but it does require attention to deadlines, documentation, and registration filings. AQ Partners helps foreign companies manage their ongoing corporate administration in Japan — from annual meeting documentation to director registration filings. Explore our Japan market entry guide or contact us to discuss your governance needs.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.