Workers' Accident Insurance in Japan (Rousai): Coverage, Rates & Claims

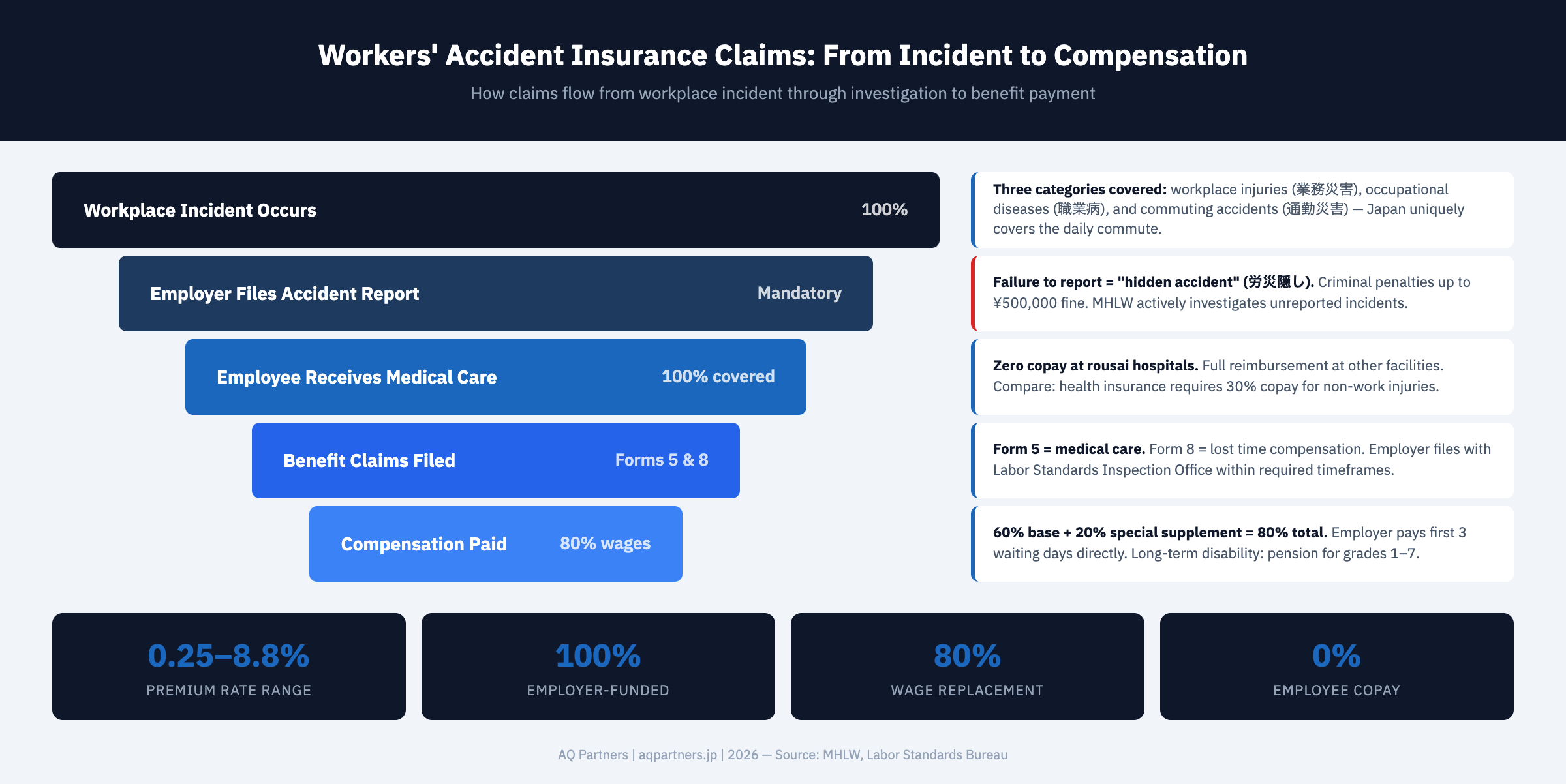

Workers' accident compensation insurance in Japan (労災保険, rousai hoken) covers medical expenses, lost wages, disability compensation, and survivor benefits for all employees injured on the job, diagnosed with an occupational disease, or involved in a commuting accident. Every worker is covered from their first day regardless of employment type, working hours, or nationality—making it the broadest-coverage social insurance program in Japan. The premium is paid entirely by the employer at industry-specific rates ranging from 0.25% to 8.8% of total payroll. Unlike health insurance and pension, workers' accident insurance has no individual enrollment process—once the company is registered for labor insurance, every employee is automatically covered.

Key Takeaways

- Every employee is covered from day one with no enrollment required—unlike health insurance and pension, workers' accident insurance requires no individual qualification notification for each employee. Once the company files a Labor Insurance Establishment Report, all current and future employees are automatically covered.

- Premiums are 100% employer-funded at industry-specific rates—rates range from 0.25% (finance, IT, business services) to 8.8% (coal mining) of total payroll, with most office-based foreign companies paying 0.3% or less. No portion is deducted from employee wages.

- Coverage extends to work injuries, occupational diseases, and commuting accidents—Japan's rousai system covers the commute between home and workplace as a protected activity, providing full medical and wage replacement benefits for commuting injuries that would not be covered in many other countries.

- Medical expenses are covered at 100% with no copay—employees receiving treatment for work-related injuries or diseases pay zero out-of-pocket costs at designated rousai hospitals or receive full reimbursement at non-designated facilities, compared to the 30% copay under health insurance.

- Wage replacement pays 80% of the average daily wage during absence—the Lost Time Compensation Benefit provides 60% of the average daily wage plus a 20% Special Supplement, totaling 80% for each day the employee cannot work due to a covered injury or disease.

Scope of Coverage

Workers' accident insurance covers three categories of events: workplace injuries, occupational diseases, and commuting accidents. Each category has specific criteria for determining whether an incident qualifies for coverage.

Workplace Injuries (業務災害)

An injury or illness qualifies as a workplace accident when it occurs during the course of employment and is caused by the employment activity. This includes injuries sustained while performing assigned duties, accidents occurring on company premises during work hours, and injuries during business trips or work-related travel. The connection between the work activity and the injury must be established—an employee injured while engaged in purely personal activities on company premises may not be covered.

Occupational Diseases (職業病)

Japan maintains a comprehensive list of recognized occupational diseases covering conditions caused by chemical exposure, physical hazards, biological agents, and work-related stress. Mental health conditions including depression and anxiety disorders can qualify as occupational diseases if they result from excessive work hours (typically over 100 hours of overtime per month) or workplace harassment. According to the Ministry of Health, Labour and Welfare, claims for mental health-related occupational diseases have increased significantly, with over 2,300 claims filed annually in recent years and approximately 700 approved.

Commuting Accidents (通勤災害)

Japan uniquely extends workers' accident insurance to cover injuries sustained during the commute between home and workplace. The commute must follow a reasonable route and method—detours for personal errands generally suspend coverage, though brief stops at convenience stores or banks along the route are typically permitted. The commuting accident provision also covers the commute between two workplaces for employees holding multiple jobs.

Premium Rates by Industry

Workers' accident insurance premium rates are set by the Ministry of Health, Labour and Welfare based on the historical accident frequency and severity of each industry classification. Rates are reviewed every three years.

| Industry Classification | Premium Rate | Typical Companies |

|---|---|---|

| Finance, Insurance, Real Estate | 0.25% | Banks, insurance companies, investment firms, real estate agencies |

| Information Services, Communications | 0.25% | IT companies, software development, telecom providers |

| Wholesale, Retail, Restaurant | 0.3% | Trading companies, retail chains, food service |

| Other Business Services | 0.3% | Consulting, staffing, professional services, advertising |

| Manufacturing (general machinery) | 0.5% | Electronics assembly, automotive parts, precision instruments |

| Transportation | 0.4–0.9% | Logistics, trucking, shipping, airline ground operations |

| Construction | 0.9–6.2% | General contractors, civil engineering, electrical work |

| Forestry | 5.2% | Logging, forest management, timber processing |

| Coal Mining | 8.8% | Underground coal extraction operations |

Most foreign companies operating in Japan—particularly those in IT, consulting, finance, and professional services—fall into the lowest rate categories at 0.25–0.3%. For a company with annual payroll of ¥100 million, the annual workers' accident insurance premium at 0.3% would be ¥300,000. The Merit Rating System (メリット制) adjusts individual company rates up or down by up to 40% based on the company's own claims history, incentivizing workplace safety. Companies with 100 or more employees (or meeting certain premium thresholds) are subject to merit rating adjustments.

Benefits and Compensation

Workers' accident insurance provides seven categories of benefits, all funded entirely by employer premiums with no copay from the injured employee.

Medical Care Benefits (療養補償給付)

All medical expenses related to a work injury or occupational disease are covered at 100%—the employee pays nothing. Treatment at designated rousai hospitals (労災指定病院) is provided directly without charge. At non-designated facilities, the employee pays upfront and is fully reimbursed. This is significantly more generous than health insurance, which requires a 30% copay.

Lost Time Compensation (休業補償給付)

When an employee cannot work due to a covered injury or disease, the Lost Time Compensation Benefit provides 60% of the average daily wage starting from the fourth day of absence. A Special Supplement (休業特別支給金) adds another 20%, bringing the effective replacement rate to 80% of daily wages. The employer is responsible for paying 60% of wages for the first three days (the waiting period) directly.

Disability Compensation (障害補償給付)

Employees left with permanent disabilities after treatment receive either a disability pension (for grades 1–7, the most severe) or a lump-sum disability payment (grades 8–14). A grade 1 disability (e.g., complete loss of both eyes or both arms) provides a pension of 313 days' worth of average daily wages per year, plus a one-time special supplement of ¥3,420,000.

Survivor Benefits (遺族補償給付)

If an employee dies from a work-related cause, eligible family members receive a survivor pension or lump-sum payment. A survivor with no other dependents receives a pension equivalent to 153 days' wages per year, with higher amounts for survivors with dependent children. A funeral expense benefit (葬祭料) of approximately ¥315,000 plus 30 days' wages is also provided.

Claims Process for Employers

When a workplace accident occurs, the employer must follow a specific claims procedure to ensure the employee receives timely benefits.

- Immediate response: Provide first aid and arrange medical transport. Direct the employee to a designated rousai hospital if possible.

- Notify the Labor Standards Inspection Office: File a Worker Accident Report (労働者死傷病報告) with the local Labor Standards Inspection Office. For injuries requiring four or more days of absence, the report must be filed without delay. For injuries requiring one to three days, a quarterly summary report is sufficient.

- File benefit claims: The employee (or employer on behalf of the employee) files the appropriate benefit claim form with the Labor Standards Inspection Office or directly with the rousai hospital. Medical care claims (Form 5) and lost time claims (Form 8) are the most common.

- Cooperate with investigation: The Labor Standards Inspection Office may investigate the accident circumstances to verify the claim. The employer must provide access to the workplace and relevant records.

Failure to report a workplace accident is a violation of the Industrial Safety and Health Act. “Hidden accidents” (労災隠し, rousai kakushi)—where employers pressure employees not to file claims or fail to report incidents—can result in fines of up to ¥500,000 and criminal prosecution. The MHLW actively investigates hidden accident cases, and foreign companies should ensure all workplace incidents are properly documented and reported.

Special Considerations for Foreign Companies

Foreign companies establishing operations in Japan should be aware of several workers' accident insurance provisions that differ from systems in many home countries.

- Commuting coverage is automatic: Unlike most countries, Japan covers commuting accidents under workers' accident insurance. This means employee injuries during train commutes, bicycle rides, or walking to work may generate employer claims history and affect merit-rated premiums.

- Mental health claims are increasing: Japan recognizes work-related mental health conditions as compensable occupational diseases. Excessive overtime (karoshi criteria: 80–100+ hours/month), workplace bullying, and harassment can trigger claims that result in significant compensation obligations.

- No private insurance substitute: Workers' accident insurance is mandatory and cannot be replaced by private employer liability insurance. Companies may carry supplemental private coverage, but the statutory rousai insurance must be maintained.

- Overseas assignments: Employees temporarily assigned overseas from a Japan-based company can be covered through a Special Enrollment (特別加入) for overseas workers, extending rousai coverage to work performed outside Japan.

Workers' accident insurance operates in conjunction with employment insurance as part of Japan's labor insurance (労働保険) framework, and both are managed through the Labor Standards Inspection Office and Hello Work. Together with health insurance and pension, these programs form the complete social insurance obligation for every employer in Japan.

Workers' accident insurance carries the lowest premium cost among Japan's social insurance programs but the highest potential exposure when serious incidents occur. Establishing proper reporting procedures and maintaining workplace safety standards protects both employees and the company's compliance record. AQ Partners manages labor insurance registration, premium calculations, annual updates, and claims coordination for foreign companies operating in Japan. Contact us at hello@aqpartners.jp.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.