Severance Pay & Retirement Allowances in Japan

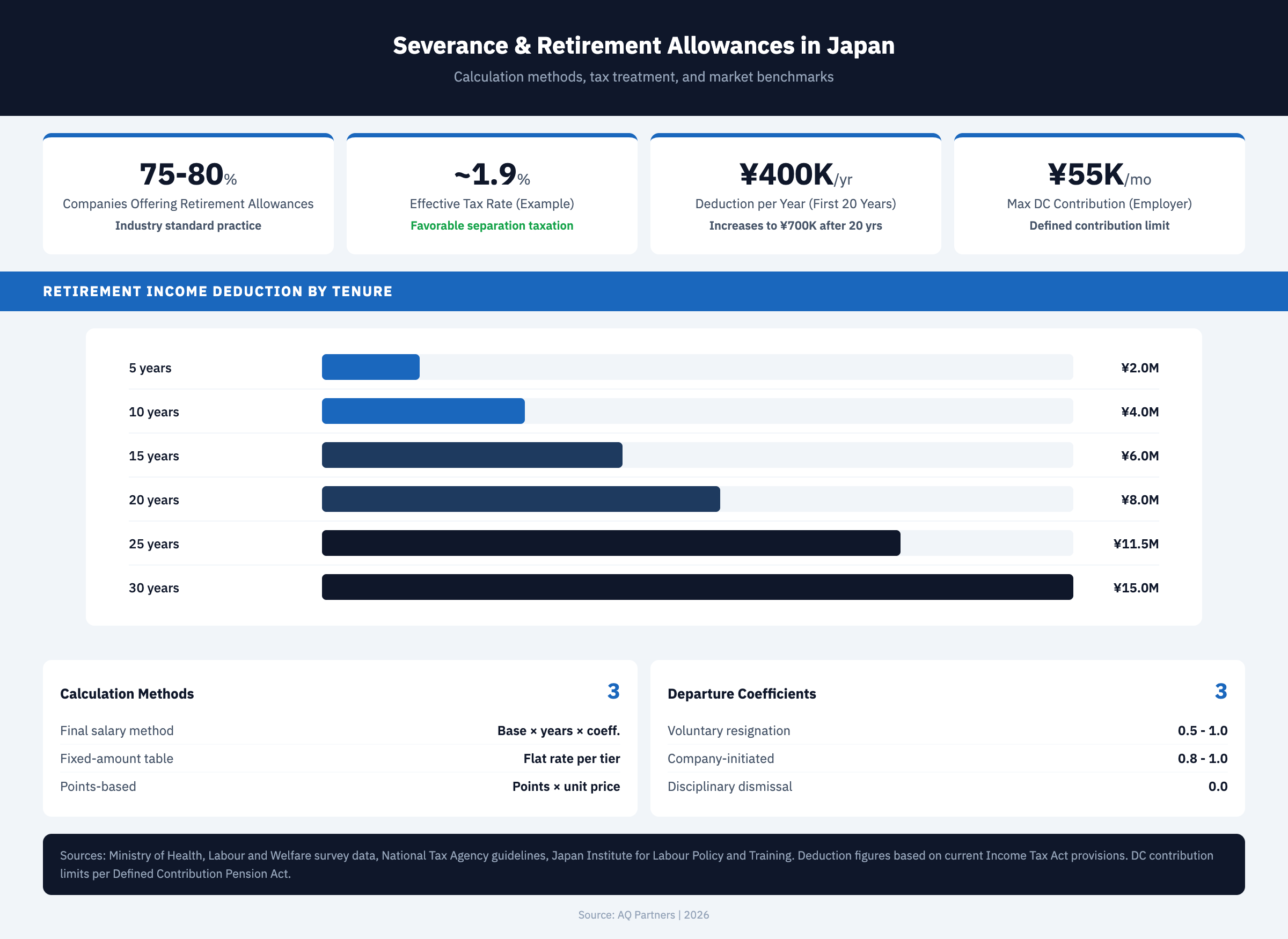

Severance pay and retirement allowances in Japan (退職金, taishokukin) are not legally required, but they remain a deeply embedded market expectation that affects hiring competitiveness, employee retention, and termination negotiations. According to the Ministry of Health, Labour and Welfare's surveys, approximately 75–80% of Japanese companies with 30 or more employees maintain some form of retirement benefit system. For foreign companies establishing operations in Japan, deciding whether to offer retirement allowances—and how to structure them—involves balancing competitive positioning against cost management and understanding the favorable tax treatment that makes these benefits particularly attractive to employees.

Key Takeaways

- Severance pay is not legally mandated but is a market norm—there is no statute requiring Japanese employers to pay severance. However, if an employer's work rules (就業規則), employment contracts, or established custom include a retirement allowance, it becomes a legally binding obligation that cannot be unilaterally reduced without employee consent.

- Typical retirement allowances range from 1 month's salary per year of service to larger amounts—the most common calculation methods yield approximately 1–2 months' base salary per year of service for voluntary resignation, and 1.2–2.5 months per year for company-initiated separation, with the rate increasing for longer tenure.

- Retirement income receives highly favorable tax treatment—retirement allowances qualify for the retirement income deduction (退職所得控除), which provides ¥400,000 per year of service for the first 20 years and ¥700,000 per year thereafter. Only 50% of the amount exceeding the deduction is taxed, significantly reducing the effective tax rate compared to regular income.

- Defined contribution (DC) plans are increasingly replacing traditional lump-sum systems—corporate DC plans (企業型確定拠出年金) allow employers to contribute to individual retirement accounts with capped monthly contributions (¥55,000 for DC-only companies), shifting investment risk to employees while providing tax-advantaged retirement savings.

- In mutual separation negotiations, severance typically runs 3–6 months' salary—when a company negotiates a voluntary departure through 退職勧奨, the settlement package typically includes an enhanced severance payment above the standard retirement allowance, providing financial incentive for the employee to agree to separation.

Retirement Allowance Calculation Methods

Japanese companies use several methods to calculate retirement allowances. The choice of method is specified in the company's work rules and directly affects both the employee's expected benefit and the company's financial liability.

| Calculation Method | Formula | Example (10 years, ¥400K base salary) | Best For |

|---|---|---|---|

| Final salary method (最終給与方式) | Final base salary × years × coefficient | ¥400K × 10 × 1.0 = ¥4,000,000 | Traditional companies, long-tenure cultures |

| Fixed-amount method (定額方式) | Fixed amount per year of service from schedule | ¥300K/year × 10 = ¥3,000,000 | Predictable budgeting, simpler administration |

| Points-based method (ポイント方式) | Accumulated points (tenure + grade + performance) × point value | Varies by accumulated points | Performance-linked, modern companies |

| Separate table method (別テーブル方式) | Lookup from published table by years × departure reason | Table-defined amount | Companies wanting to decouple from salary increases |

Most methods apply a departure reason coefficient that adjusts the payment amount based on whether the employee resigned voluntarily, was dismissed, or reached mandatory retirement age:

| Years of Service | Voluntary Resignation | Company-Initiated | Mandatory Retirement |

|---|---|---|---|

| Less than 3 years | 0.5–0.6 | 0.8–1.0 | 1.0 |

| 3–5 years | 0.6–0.7 | 0.9–1.0 | 1.0 |

| 5–10 years | 0.7–0.8 | 1.0 | 1.0 |

| 10–20 years | 0.8–0.9 | 1.0 | 1.0 |

| 20+ years | 0.9–1.0 | 1.0 | 1.0 |

| Disciplinary dismissal | N/A | 0.0 (typically forfeited) | N/A |

Tax Treatment of Retirement Income

Japan's tax code provides significantly favorable treatment for retirement allowances, making them one of the most tax-efficient forms of compensation. The National Tax Agency taxes retirement income as follows:

Step 1 — Calculate the retirement income deduction (退職所得控除):

- For service of 20 years or less: ¥400,000 × years of service (minimum ¥800,000)

- For service exceeding 20 years: ¥8,000,000 + ¥700,000 × (years of service − 20)

Step 2 — Calculate taxable retirement income:

- (Retirement allowance − retirement income deduction) × 1/2 = taxable retirement income

Example: An employee with 15 years of service receiving ¥8,000,000 in retirement allowance:

- Deduction: ¥400,000 × 15 = ¥6,000,000

- Taxable: (¥8,000,000 − ¥6,000,000) × 1/2 = ¥1,000,000

- Tax: approximately ¥50,000 in income tax + ¥100,000 in resident tax = ~¥150,000

- Effective tax rate: approximately 1.9% on the ¥8,000,000 payment

This compares favorably to regular salary income, which would be taxed at the marginal rate (potentially 20–33% for income in this range). The tax advantage makes retirement allowances an attractive component of total compensation, particularly for employees who understand the differential treatment.

Defined Contribution (DC) Plans

Corporate defined contribution plans (企業型確定拠出年金, kigyōgata kakutei kyoshutsu nenkin) have become increasingly popular as an alternative or supplement to traditional lump-sum retirement allowances. Under a DC plan:

- The employer makes monthly contributions to individual employee accounts (maximum ¥55,000/month for DC-only companies, ¥27,500 if the company also has a defined benefit plan)

- Employees choose from a menu of investment options (typically mutual funds, insurance products, and savings deposits)

- The accumulated balance belongs to the employee and is portable when changing employers

- Employer contributions are tax-deductible as a business expense and are not counted as employee income when contributed

- Investment gains within the account are tax-free until withdrawal

- Withdrawals at retirement age (60+) receive the same favorable retirement income deduction treatment as traditional severance

For foreign companies, DC plans offer several advantages over traditional lump-sum retirement allowances: predictable monthly costs, no unfunded liability accumulation on the balance sheet, portability that makes them attractive to mobile employees, and alignment with parent company retirement benefit philosophies. The trade-off is that employees bear the investment risk and the employer contribution limits are relatively low compared to typical lump-sum payouts at large companies.

Defined Benefit (DB) Plans

Traditional defined benefit plans (確定給付企業年金, kakutei kyūfu kigyō nenkin) promise a specific retirement benefit calculated by formula, with the employer bearing the investment risk and funding obligation. DB plans are more common at large Japanese corporations and are less frequently adopted by foreign companies due to:

- Complex actuarial calculations and annual funding obligations

- Balance sheet liability that can fluctuate with investment returns and interest rates

- Regulatory requirements including annual actuarial reports and minimum funding standards

- Limited flexibility to reduce benefits once established

Severance in Mutual Separation Context

When an employer negotiates a mutual separation agreement, the severance package typically includes both the standard retirement allowance (if the company has one) and an additional settlement payment to incentivize voluntary departure.

| Component | Typical Range | Tax Treatment | Notes |

|---|---|---|---|

| Standard retirement allowance | Per work rules formula | Retirement income (favorable) | Only if work rules provide for it |

| Additional settlement payment | 3–6 months' salary (typical) | Retirement income (favorable) | Incentive for voluntary departure |

| Notice period salary | 1 month (garden leave) | Regular employment income | If employee is released from work during notice period |

| Accrued paid leave payout | Remaining days × daily rate | Regular employment income | Or employee uses leave during notice period |

| Outplacement support | Optional | Company expense (deductible) | Career counseling, job search assistance |

The total package in a mutual separation typically ranges from 3 to 12 months' total compensation depending on the employee's tenure, seniority, and the strength of the employer's legal position regarding dismissal. Employees with longer tenure or stronger wrongful dismissal claims generally command larger packages. The termination rules guide covers the legal framework that shapes these negotiations.

Recommendations for Foreign Companies

- Small companies (under 20 employees): Consider implementing a simple defined contribution plan rather than a traditional retirement allowance. The predictable monthly cost (¥10,000–¥55,000 per employee) is easier to budget than an accumulating lump-sum obligation, and the benefit is attractive to employees.

- Growing companies: If you offer a retirement allowance, use a points-based or fixed-amount method rather than a final-salary method. Final-salary calculations create unpredictable liabilities as employees receive promotions and salary increases.

- All companies: Whatever retirement benefit structure you choose, document it clearly in your work rules. Ambiguity in retirement allowance provisions leads to disputes at the time of separation—precisely when the relationship is most strained.

Retirement benefits are a significant component of total compensation in Japan, and understanding how they are structured, calculated, and taxed is essential for both competitive hiring and smooth employment separations. AQ Partners helps foreign companies design retirement benefit structures, draft work rules provisions, and manage the tax treatment of severance payments. Contact us at hello@aqpartners.jp.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.