Japan Payroll for Foreign Employees

Key Takeaways

- Residency status determines everything about how foreign employees are taxed in Japan — residents are taxed on worldwide income using the same progressive rates as Japanese employees; non-residents are taxed only on Japan-sourced income at a flat 20.42%, with no inhabitant tax and no year-end adjustment.

- Japan has tax treaties with 80+ countries — foreign employees from treaty countries may qualify for reduced withholding or short-stay exemptions, but the benefit only applies if the employee submits the correct treaty relief application to the employer before payroll is processed.

- Social insurance is mandatory for most foreign employees on long-term work visas — the same rules that apply to Japanese employees apply to foreign nationals, with exemptions available only where a bilateral totalization agreement applies and the employee holds a certificate of coverage from their home country.

- All foreign residents must have a My Number — employers are required to collect, verify, and retain My Number for every foreign employee within a reasonable period of hire; the number is used on all tax filings, social insurance applications, and year-end adjustment documents.

- Departing foreign employees trigger a specific final payroll process — including settlement of outstanding salary, withholding tax on the final payment, residence tax coordination, and the option to claim a pension lump-sum withdrawal (dattai-ichiji-kin) within two years of leaving Japan.

Japan payroll for foreign employees is not simply a variation on standard Japan payroll — it introduces a distinct set of residency determinations, tax treaty obligations, social insurance exemptions, and departure procedures that do not apply to domestic hires. For foreign companies bringing international staff to Japan, or for Japan entities hiring from overseas, understanding these rules before the first pay cycle is essential. Errors in residency classification, treaty relief application, or My Number collection can create compliance exposure across multiple regulatory authorities simultaneously. This post covers the complete payroll framework for foreign employees in Japan, from initial residency determination through to final settlement on departure. For the full payroll compliance context, see our Japan payroll guide.

Residency Status: How Japan Taxes Foreign Employees

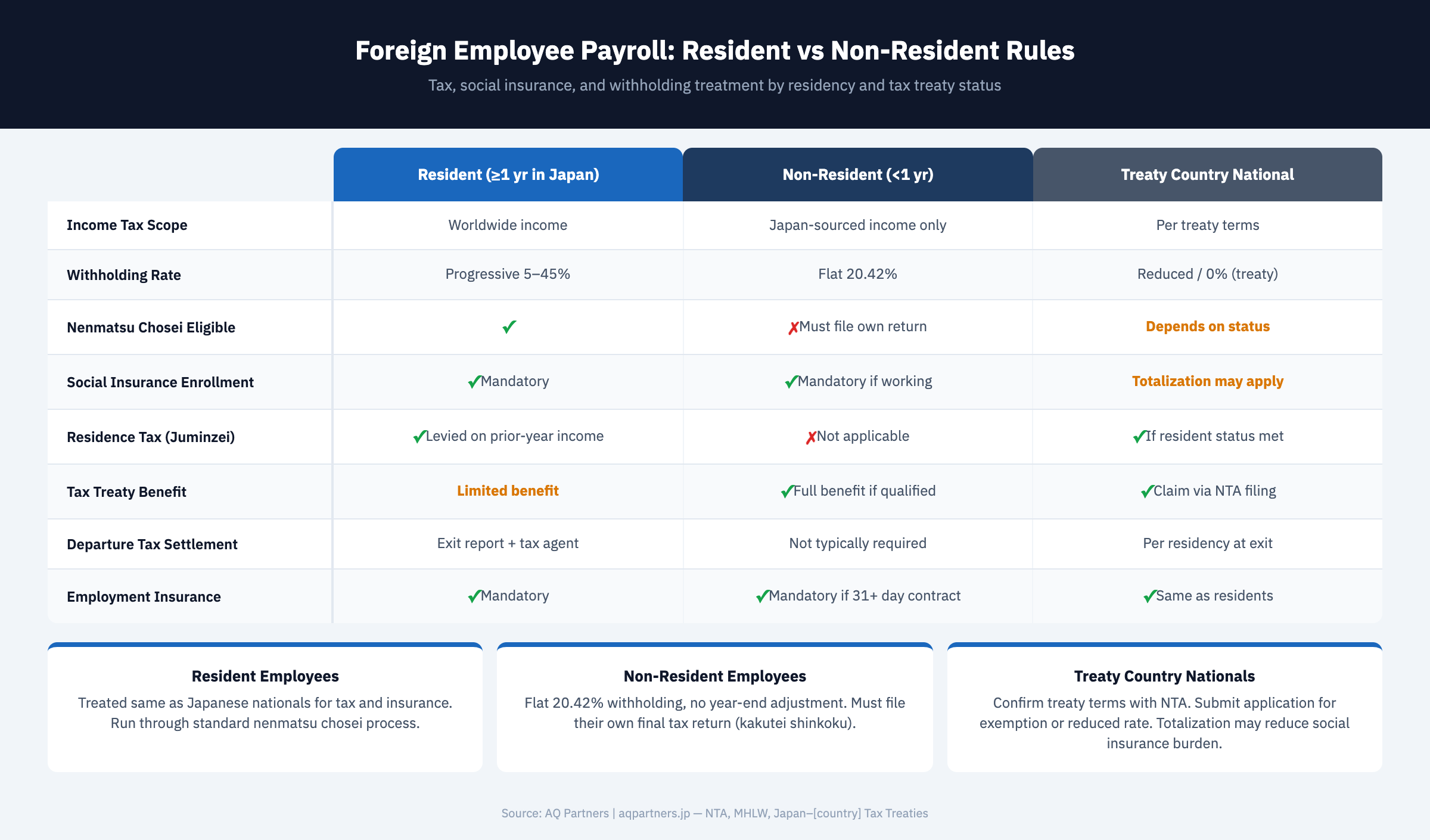

Japan distinguishes two tax statuses for foreign employees — resident and non-resident — and the distinction determines not only the withholding rate but the entire method of payroll tax calculation. Most foreign employees on long-term work visas qualify as residents within their first year in Japan.

Under Japan's income tax law, a resident is defined as an individual who has a domicile in Japan, or who has maintained a residence in Japan for one year or more. A non-resident is an individual who does not meet either of those conditions — typically a short-term business visitor or a foreign national who has been in Japan for fewer than 12 months with no intention of establishing permanent residence.

The payroll implications of this distinction are significant. Resident foreign employees are taxed on their worldwide income using Japan's standard progressive income tax schedule — the same rates that apply to Japanese employees. This means their payroll withholding follows the same monthly calculation tables, the same dependency deduction rules, and the same year-end adjustment (nenmatsu chosei) process. Non-resident foreign employees, by contrast, are taxed only on Japan-sourced income, at a flat rate of 20.42% (including the 2.1% reconstruction surtax). No inhabitant tax applies to non-residents. No nenmatsu chosei is performed. The withholding is final — there is no annual reconciliation.

For employers, the determination of residency status must be made at the point of hire, not retrospectively. If a foreign employee enters Japan on a long-term work visa — engineer, specialist in humanities, intracompany transferee, or similar — they will typically qualify as a resident within 12 months of arrival, at which point the withholding rate and calculation method must be updated. Employers should track the date of arrival and residency status for each foreign employee and review the status at the 12-month mark. Failure to update withholding when status changes from non-resident to resident creates a payroll error that will surface at year-end adjustment or, if the employee files a personal tax return, in a correction request from the National Tax Agency (NTA).

For salary structure considerations that interact with residency status — including the treatment of housing allowances and cost-of-living adjustments for expatriate employees — see our post on Japan salary structure, allowances, and bonuses.

Income Tax Withholding for Foreign Employees

Resident foreign employees are subject to the same progressive withholding tax schedule as Japanese employees; non-resident foreign employees are subject to a flat 20.42% withholding on all Japan-sourced income, with no inhabitant tax and no year-end adjustment. The employer must determine which regime applies at the point of hire and update it when residency status changes.

For resident foreign employees, income tax withholding follows Japan's standard monthly withholding tax tables published by the NTA. National income tax rates range from 5% on income up to ¥1.95 million to 45% on income above ¥40 million. Inhabitant tax — a flat 10% levied by the local municipality — applies in addition, though it is collected with a one-year lag based on the prior year's income. The combined effective rate for high earners can reach 55% including the reconstruction surtax. The year-end adjustment (nenmatsu chosei) is mandatory for resident employees, reconciling the aggregate of monthly withholdings against the employee's actual annual tax liability.

For non-resident foreign employees, withholding is straightforward in calculation but requires careful identification of what constitutes Japan-sourced income. All income attributable to services performed in Japan is Japan-sourced and subject to the 20.42% flat withholding. Income for services performed outside Japan is not Japan-sourced and is not subject to withholding by the Japan employer. Where an employee works partly in Japan and partly abroad, the employer must apportion the income correctly and withhold only on the Japan portion. No nenmatsu chosei is performed for non-resident employees. No inhabitant tax deduction is made from payroll.

If a foreign employee's residency status changes during the employment period — for example, if they pass the 12-month threshold and become a resident — the employer must switch from the non-resident flat-rate withholding to the resident progressive schedule from the month in which the status change takes effect. Any under- or over-withholding from prior months during non-resident status is not subject to retroactive adjustment by the employer; the employee may need to file a personal tax return to settle any remaining liability.

Tax Treaties: Reducing Double Taxation

Japan has tax treaties with more than 80 countries. Treaty benefits — including reduced withholding rates and short-stay exemptions — do not apply automatically; the employee must submit a treaty relief application to the employer, and the employer must retain and submit the application to the tax office. Without a valid application on file, full withholding applies even where the income would otherwise be exempt.

Japan's network of income tax treaties is extensive. Key treaty partners include the United States, United Kingdom, Australia, Canada, Germany, France, Netherlands, Switzerland, Singapore, South Korea, and China, among many others. The specific benefits available under each treaty vary, but two categories are most relevant to payroll.

The first is a reduced withholding rate on employment income. Under certain treaties, the withholding rate on salary paid to non-resident employees may be reduced below the standard 20.42% flat rate. The applicable rate depends on the specific treaty and the nature of the income.

The second is the short-stay business visitor exemption. Most of Japan's tax treaties include a provision — typically structured around the OECD model — that exempts employment income from Japan tax where the individual is present in Japan for fewer than 183 days in the relevant period, the remuneration is paid by or on behalf of an employer who is not a resident of Japan, and the remuneration is not borne by a permanent establishment of the employer in Japan. Where all three conditions are met, the foreign employee's salary may be fully exempt from Japan income tax, and the employer should not withhold on that income.

To claim any treaty benefit, the employee must submit a treaty relief application form (租税条約に関する届出書) to the employer. The employer retains the original and submits a copy to the relevant tax office by the date of the first payment to which the treaty benefit applies. Without this form on file, the employer has no basis to apply reduced withholding or an exemption — even if the employee clearly qualifies. Employers should build a treaty application collection step into their onboarding process for all foreign national hires. The PwC Japan Tax Summaries resource provides useful reference data on treaty rates by country.

Social Insurance for Foreign Employees

Foreign employees on long-term work visas are subject to the same mandatory social insurance enrollment as Japanese employees. Exemptions are available only where a bilateral totalization agreement applies and the employee holds a valid certificate of coverage from their home country social security authority.

| Situation | Social Insurance Treatment | Key Rule |

|---|---|---|

| Foreign employee on work visa (long-term) | Mandatory enrollment | Same as Japanese employees |

| Short-term assignee (<5 years) | Mandatory unless totalization applies | Check bilateral agreement with home country |

| Totalization agreement country (USA, UK, Germany, France, etc.) | May be exempt from Japan pension (kosei nenkin) | Certificate of coverage from home country required before work begins |

| Employee paying into home country pension | Can opt out of Japan kosei nenkin if totalization applies | Certificate A1 or equivalent must be presented to employer and Japan Pension Service |

| Non-resident employee (<1 year) | Enrolled in health insurance; may be exempt from pension | Residency-period dependent; confirm with Japan Pension Service |

| Employee holding multiple visas / working across countries | Complex — each jurisdiction assessed independently | Seek specialist advice; do not assume exemption without confirmation |

| Departing employee (final payroll) | Full settlement; pension lump-sum refund possible | Lump-sum withdrawal (dattai-ichiji-kin) available within 2 years of departure |

| Dependent family members | Health insurance covers dependents | Register dependents within 5 days of enrollment or change |

Social insurance in Japan covers four schemes: health insurance (kenko hoken), employees' pension insurance (kosei nenkin), employment insurance (koyo hoken), and workers' accident compensation insurance (rodo saigai hoken). The first two are administered jointly; the latter two are administered separately under the Ministry of Health, Labour and Welfare (MHLW). All four apply to foreign employees on long-term work visas in the same way they apply to Japanese employees. Employer contributions for health insurance and pension are split 50/50 between employer and employee; employment insurance contributions are split at approximately 6:4 employer to employee ratio. For a full breakdown of social insurance contribution rates and the nenmatsu chosei process, see our post on Japan payroll compliance: social insurance and nenmatsu chosei.

Totalization Agreements — Which Countries Qualify

Japan has totalization agreements with 23 countries as of 2025. These agreements prevent foreign employees from paying pension contributions in both Japan and their home country simultaneously. The key operational requirement is that the employee must obtain a certificate of coverage from their home country social security authority before beginning work in Japan — without it, the Japan pension exemption cannot be applied.

Japan's totalization agreements cover the following countries: United States, United Kingdom, Germany, France, Belgium, Canada, Australia, Netherlands, Czech Republic, Spain, Ireland, Brazil, Switzerland, Hungary, India, Luxembourg, Philippines, Slovak Republic, China, Finland, Sweden, Italy, and Austria. Additional agreements may be signed or take effect after the publication date of this post; the Japan Pension Service maintains the current list.

Under a totalization agreement, a foreign employee who remains enrolled in their home country pension system — typically because they are on a temporary assignment to Japan — is exempt from contributing to Japan's kosei nenkin during the period covered by the certificate. The certificate of coverage (sometimes called a Certificate A1 in EU/EEA contexts, or a specific certificate form under the bilateral agreement with Japan) is issued by the home country social security authority and must be presented to the employer and, in some cases, submitted to the Japan Pension Service office.

Employers must not assume that an employee from a totalization agreement country is automatically exempt. The exemption is conditional on the employee actually holding a valid certificate that covers the period of Japan employment. Without the certificate, the default rule applies: mandatory enrollment in kosei nenkin. Certificates should be collected as part of the onboarding documentation for any inbound assignee from a totalization agreement country. The JETRO Business Setup Guide provides background on employment obligations for foreign companies establishing a Japan presence, including social insurance considerations.

For organizations managing foreign employees across multiple Japan assignments and jurisdictions, a clear tracking system for certificate validity periods is essential. Certificates are typically issued for a defined coverage period — often up to three or five years — and must be renewed if the assignment continues beyond that period.

My Number for Foreign Employees

All foreign residents in Japan who pay tax or receive social insurance must have a My Number. The employer is required to collect My Number from every foreign employee within a reasonable period of hire and use it on all tax filings, social insurance applications, and year-end adjustment documents. Records must be retained for seven years.

My Number (個人番号) is Japan's individual identification number system, introduced in 2016. Every individual registered as a resident of Japan — including foreign nationals — is issued a 12-digit My Number by their local municipality after completing resident registration (jūminhyo toroku). Foreign nationals on long-term visas who register their address at the local ward office receive their My Number notification card at their registered address, typically within two to three weeks of registration.

From a payroll perspective, the employer's obligations around My Number are specific and non-negotiable. The employer must collect the employee's My Number — confirmed against their Individual Number Card or another approved verification document — within a reasonable period of starting employment. "Reasonable period" is not formally defined in the law but is generally interpreted as shortly after the employee receives their notification. The employer must then use the My Number on all tax withholding forms, social insurance enrollment applications, and the year-end adjustment document (源泉徴収票, gensen choshu hyo). Records containing My Number must be retained for seven years and handled in accordance with the Act on the Use of Numbers to Identify a Specific Individual in Administrative Procedures.

A common operational challenge arises when a foreign employee starts work before their My Number has been issued — for example, in the weeks immediately after arriving in Japan and registering their address. In this situation, the employer should proceed with onboarding and payroll processing and collect the My Number as soon as it is available. The My Number cannot be left blank permanently; it must be obtained and added to the relevant documents. Using MoneyForward Cloud Payroll or similar domestic payroll software with built-in My Number collection workflows helps ensure that the collection step is tracked and completed for every employee, including foreign nationals.

When a foreign employee leaves Japan permanently, their My Number becomes inactive for residency and tax purposes. The employer must complete and issue the final gensen choshu hyo using the My Number on record. The employer's copy and associated records must be retained for the full seven-year period even after the employee's departure. My Number must not be shared with third parties or used for any purpose other than those specified in the Act.

Departing Employee Payroll — Final Settlement

When a foreign employee leaves Japan, the final payroll run must cover outstanding salary, unused vacation settlement, pro-rated bonus where applicable, and correct withholding tax on the final payment. Residence tax settlement and the pension lump-sum withdrawal option are additional steps specific to departing foreign nationals.

Final payroll for a departing foreign employee involves several parallel obligations that must be coordinated carefully. The payroll calculation itself must settle all outstanding salary up to the last day of employment, any unused paid annual leave that the employment contract or internal policy requires to be paid out, and any pro-rated bonus that has accrued and is payable under the terms of the employment agreement. Income tax withholding on the final payment follows the same rules as any other monthly payroll run — resident rate for resident employees, 20.42% flat for non-resident employees.

Residence tax (jūminzei) requires a separate step. Residence tax is levied by the local municipality based on the prior year's income and is typically collected through payroll in monthly installments from June of the current year through May of the following year. When an employee leaves Japan mid-year, the remaining balance of their annual residence tax liability is typically collected as a lump sum in the final payroll. The employer should confirm the outstanding amount with the relevant municipality and deduct it from the final payment where the employee has consented to this arrangement.

The pension lump-sum withdrawal (脱退一時金, dattai-ichiji-kin) is available to foreign nationals who leave Japan after having been enrolled in kosei nenkin. Eligible individuals can apply to the Japan Pension Service for a refund of a portion of their pension contributions within two years of leaving Japan. The refund is calculated based on the number of months of enrollment, up to a maximum of 60 months (five years). The employer's role in this process is limited — the employer must issue the final gensen choshu hyo accurately, as the employee will need it when applying to the Japan Pension Service from abroad. The application is submitted directly by the departing employee, not by the employer, but employees should be informed of this option before they leave Japan.

The employer must issue the final 源泉徴収票 (gensen choshu hyo — withholding tax certificate) to the departing employee. This document summarizes the total salary paid and total tax withheld during the employment period and is required both for the employee's personal tax filing (if applicable) and for the pension lump-sum withdrawal application. For teams managing international HR compliance across multiple jurisdictions, see our post on Japan HR compliance strategies for global teams for a broader framework.

How AQ Partners Can Help

AQ Partners provides payroll and back-office services for foreign companies operating in Japan. For organizations employing foreign nationals in Japan — whether inbound assignees, locally-hired foreign employees, or remote workers transitioning to Japan-based roles — we manage the full payroll compliance process: residency status determination, withholding tax setup, treaty relief application coordination, social insurance enrollment and totalization certificate handling, My Number collection, and final settlement payroll for departing employees.

Our services are designed for foreign-owned Japan entities that need payroll compliance handled correctly from day one, without the operational overhead of building in-house Japan payroll expertise for a small or mid-size team.

Need payroll support for foreign employees in Japan? Contact AQ Partners →

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.