Online Banking & Fintech Solutions for Foreign Companies in Japan

Online banking and fintech solutions in Japan have expanded significantly for corporate users, but foreign companies still face a distinctive set of challenges when setting up and managing digital banking. Japanese corporate internet banking systems rely heavily on physical security devices (hardware tokens, IC card readers), require Japanese-language interfaces in many cases, and integrate tightly with domestic tax filing and social insurance payment systems. Understanding which platforms offer English support, API connectivity, and cloud accounting integration can save foreign companies months of operational friction during their first year in Japan.

Key Takeaways

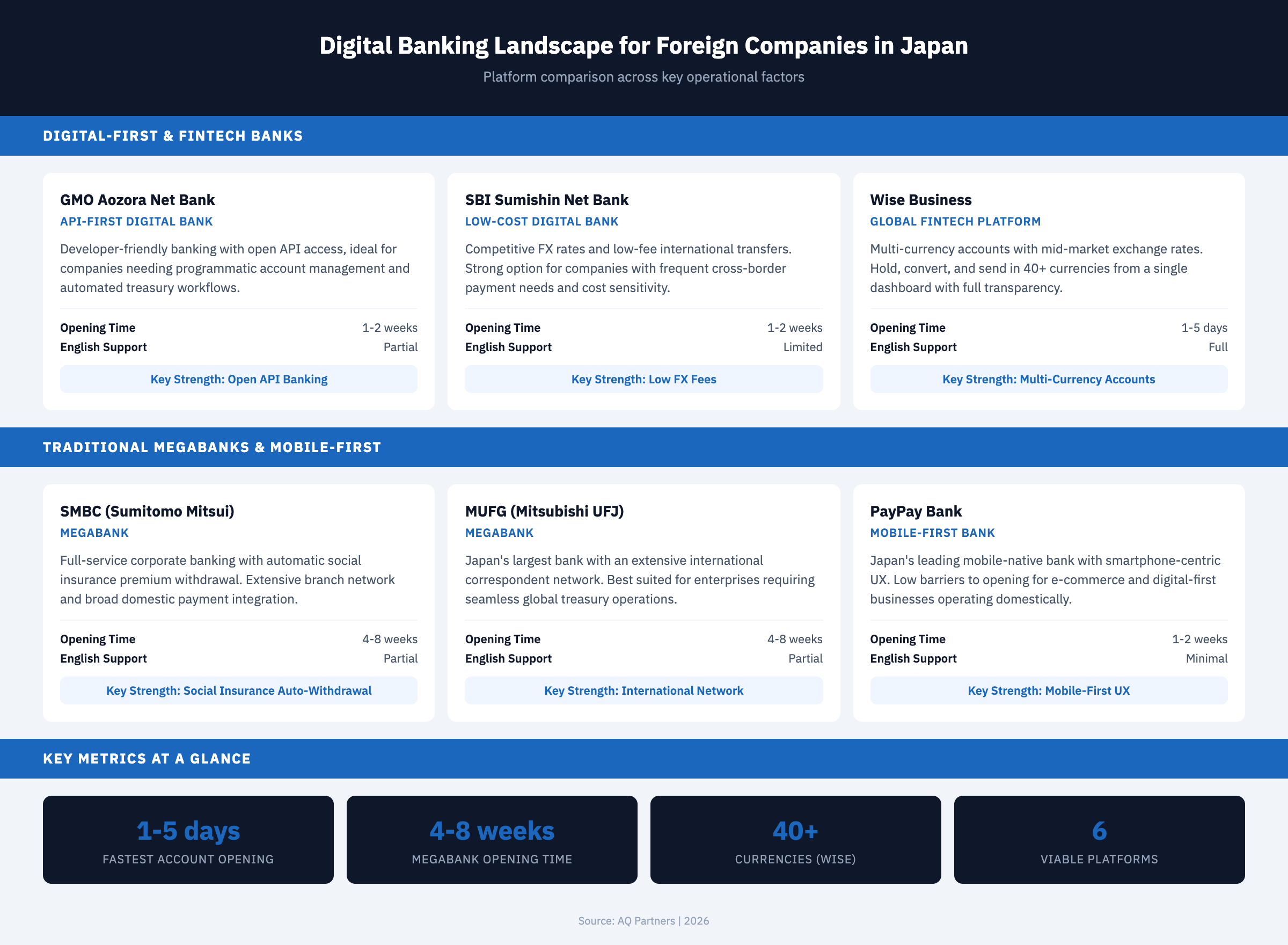

- Digital-first banks approve accounts faster than megabanks—GMO Aozora Net Bank and SBI Sumishin Net Bank can process corporate account applications in 1–2 weeks, compared to 4–8 weeks at traditional megabanks like SMBC, MUFG, and Mizuho.

- Most Japanese internet banking systems require hardware security tokens—corporate accounts at SMBC, MUFG, and Mizuho use IC card readers or dedicated hardware tokens for transaction authorization, which must be physically present at each login and payment approval.

- English-language internet banking remains limited at major banks—SMBC Global Pass and MUFG BizStation offer partial English interfaces, but most transaction screens, tax payment modules, and error messages default to Japanese. Digital banks like GMO Aozora provide fuller English support.

- Cloud accounting integration eliminates manual data entry—freee, Money Forward, and other Japanese cloud accounting platforms connect directly to bank transaction feeds via API or data scraping, automatically importing and categorizing transactions for bookkeeping.

- Tax and social insurance payments can be automated through e-banking—corporate internet banking systems integrate with e-Tax (national tax) and eLTAX (local tax) for electronic tax payments, and support automatic withdrawal (口座振替) for social insurance premiums.

Digital Banking Platforms for Corporate Accounts

Japan's corporate banking landscape includes both traditional megabanks with internet banking add-ons and digital-first banks designed for online operations. For foreign companies, the choice between these platforms affects account opening speed, daily operational efficiency, and long-term integration with Japanese financial infrastructure.

| Platform | Type | English Support | Account Opening | Key Strength |

|---|---|---|---|---|

| GMO Aozora Net Bank | Digital bank | Partial English UI | 1–2 weeks | API banking, low fees, startup-friendly |

| SBI Sumishin Net Bank | Digital bank | Limited | 1–2 weeks | Low transfer fees, FX services |

| PayPay Bank | Digital bank | Minimal | 1–2 weeks | Easy onboarding, mobile-first |

| SMBC (Trunk) | Megabank | SMBC Global Pass (English) | 4–8 weeks | Social insurance auto-withdrawal, credibility |

| MUFG (BizStation) | Megabank | Partial English | 4–8 weeks | International network, trade finance |

| Mizuho (e-Business) | Megabank | Limited | 4–8 weeks | Government banking partner, large corp services |

| Rakuten Bank | Digital bank | Limited | 1–3 weeks | Rakuten ecosystem integration, low fees |

| Wise Business | Fintech (non-bank) | Full English | 1–5 days | Multi-currency, low FX fees (not a full bank) |

The recommended strategy for most foreign companies is a dual-bank approach: open a digital bank account first (GMO Aozora or SBI Sumishin) for immediate operational banking, then apply to a megabank (SMBC or MUFG) for social insurance auto-withdrawal and credibility with Japanese business partners. The detailed comparison of bank features and application requirements is covered in the corporate bank comparison guide.

Internet Banking Security Systems

Japanese corporate internet banking uses multi-layered security that foreign companies often find more restrictive than banking systems in other markets. Understanding these requirements before account activation prevents operational disruptions.

Megabanks typically use a combination of login ID/password, hardware security tokens (ワンタイムパスワード生成器) or IC card readers, and transaction-specific authorization codes. The hardware token must be physically available for each payment approval, meaning remote or distributed teams cannot share banking access as easily as with software-based two-factor authentication.

Digital banks generally use software-based security: smartphone app authentication, SMS one-time passwords, or email verification codes. This makes them more practical for foreign companies with team members who may not always be physically present in the Japan office. GMO Aozora's corporate banking API allows programmatic access to account data and payment initiation, enabling custom integrations that bypass the browser-based interface entirely.

Cloud Accounting Integration

Connecting bank accounts to cloud accounting software eliminates manual transaction entry and reduces bookkeeping errors. Japan's three major cloud accounting platforms—freee, Money Forward Cloud, and Yayoi Online—all support automatic bank transaction import.

Integration works through two mechanisms: API connections (direct data feeds supported by digital banks like GMO Aozora and SBI Sumishin) and screen scraping (automated login and data extraction from internet banking portals, used for megabank connections). API connections are more reliable and faster, while screen scraping can break when banks update their portal interfaces.

For foreign companies, freee offers the most comprehensive English-language support among Japanese cloud accounting platforms and connects to virtually all Japanese banks. Money Forward Cloud provides stronger reporting features for companies that need consolidated multi-entity accounting. The accounting software comparison covers the detailed feature differences between these platforms.

Tax and Social Insurance Payment Automation

Corporate internet banking in Japan integrates with the national and local tax payment systems, enabling electronic tax filing and payment without visiting a tax office or bank branch.

- e-Tax (国税電子申告): National tax payments (corporate tax, consumption tax, withholding tax) can be initiated directly from internet banking using the Pay-easy system. The company's e-Tax identifier links bank payments to filed returns automatically.

- eLTAX (地方税電子申告): Local tax payments (enterprise tax, inhabitants tax) use a similar electronic payment system. eLTAX integration is available through most megabank and digital bank internet banking platforms.

- Social insurance premiums: Health insurance and pension premiums can be paid via automatic withdrawal (口座振替) from the designated bank account. SMBC and other megabanks support direct linkage with the Japan Pension Service's automatic collection system, while some digital banks require manual transfer.

- Labor insurance premiums: Annual labor insurance premium payments (employment insurance + workers' accident insurance) can be processed electronically through Pay-easy or bank transfer.

Setting up these automated payment channels during the first month of operations prevents missed deadlines and late payment penalties. The corporate bank account opening guide covers the prerequisite documentation and application process, while the tax filing schedule details payment deadlines throughout the year.

API Banking and Open Banking in Japan

Japan's amended Banking Act (2017) established a framework for open banking by requiring banks to publish API connection policies and work with registered third-party providers (電子決済等代行業者). However, corporate API access remains more limited than in markets with mandated open banking standards like the EU's PSD2.

GMO Aozora Net Bank leads in corporate API adoption, offering transaction data retrieval, balance inquiries, and payment initiation through REST APIs. This enables foreign companies to build custom treasury dashboards, automate vendor payments, and integrate banking data directly into ERP systems without manual downloads. Other banks offer more limited API access, primarily for account aggregation through third-party accounting platforms rather than direct corporate use.

For most foreign companies in the early stages of Japan operations, the practical API benefit comes through cloud accounting integration rather than custom-built banking interfaces. As the company scales, direct API access can automate payroll disbursement, vendor payment batches, and real-time cash position monitoring.

Digital banking infrastructure is the operational backbone of every foreign company in Japan. Choosing the right combination of bank accounts, security configurations, and software integrations during the first months of operation determines how efficiently the company can manage payroll, tax payments, and daily transactions going forward. AQ Partners sets up corporate banking, configures internet banking systems, and integrates bank feeds with cloud accounting platforms as part of our market entry back office services. Contact us at hello@aqpartners.jp.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.